Market Intelligence

Weekly Wool Market Commentary

Moses & Son is committed to providing our valued customers the most current information and data to empower your decision-making process. Discover our latest Australian wool market weekly update below, along with archived reports for your perusal and analysis.

2026-S04

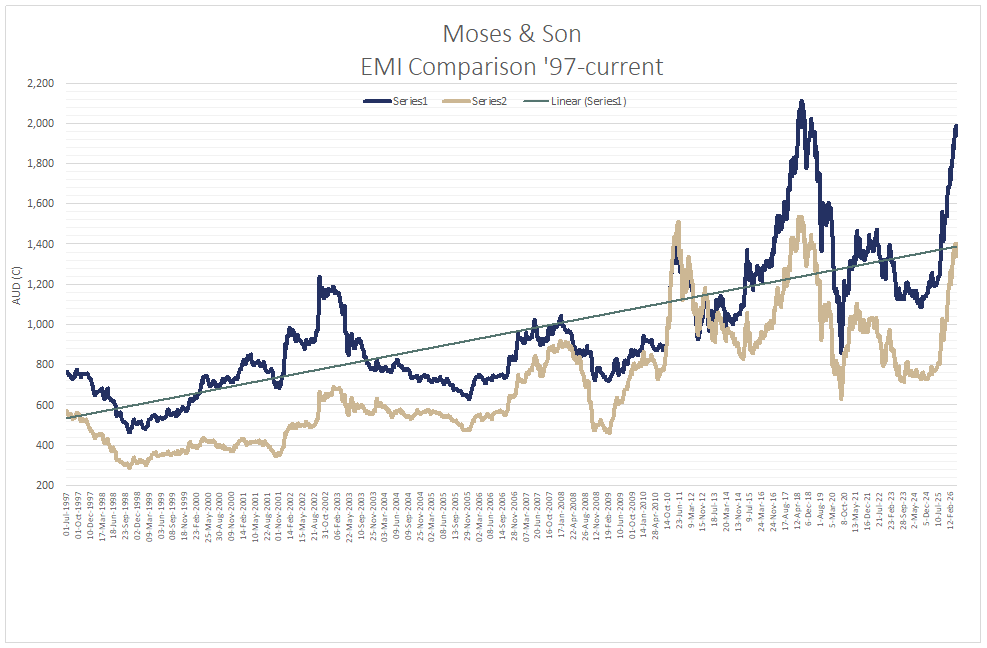

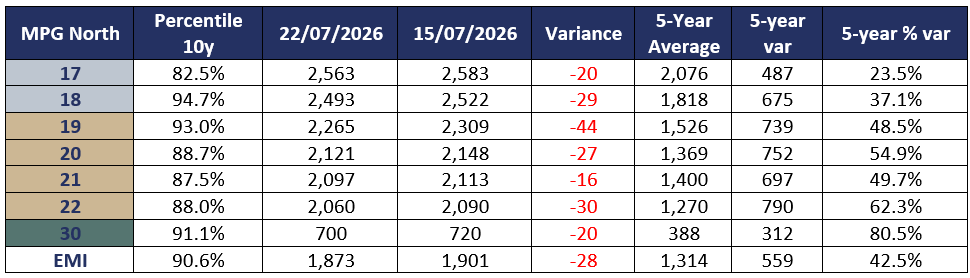

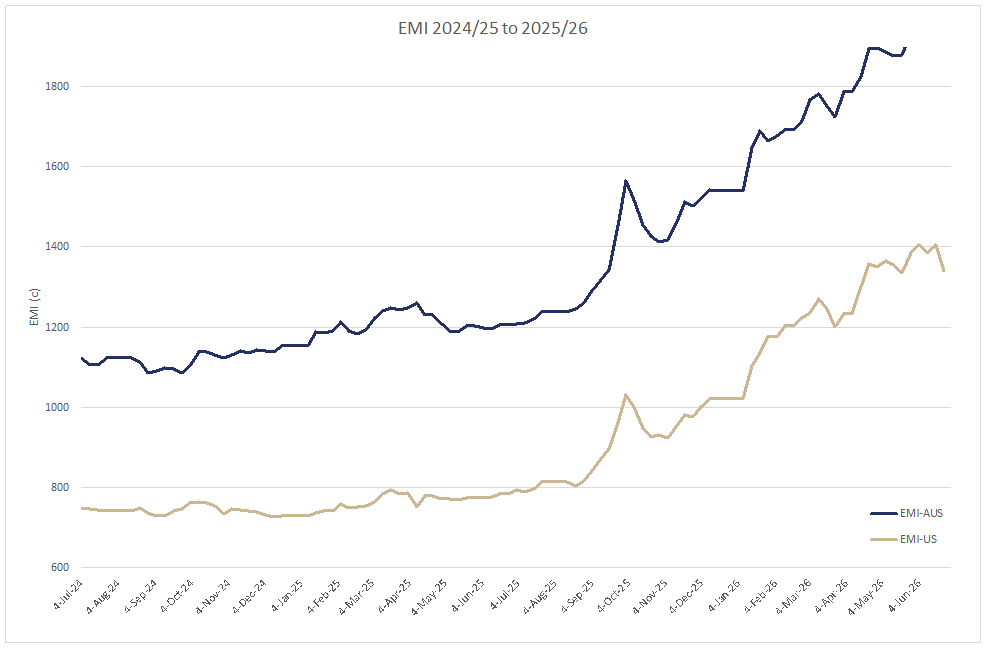

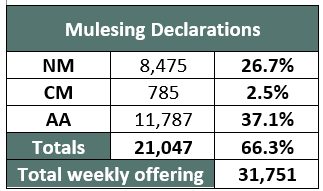

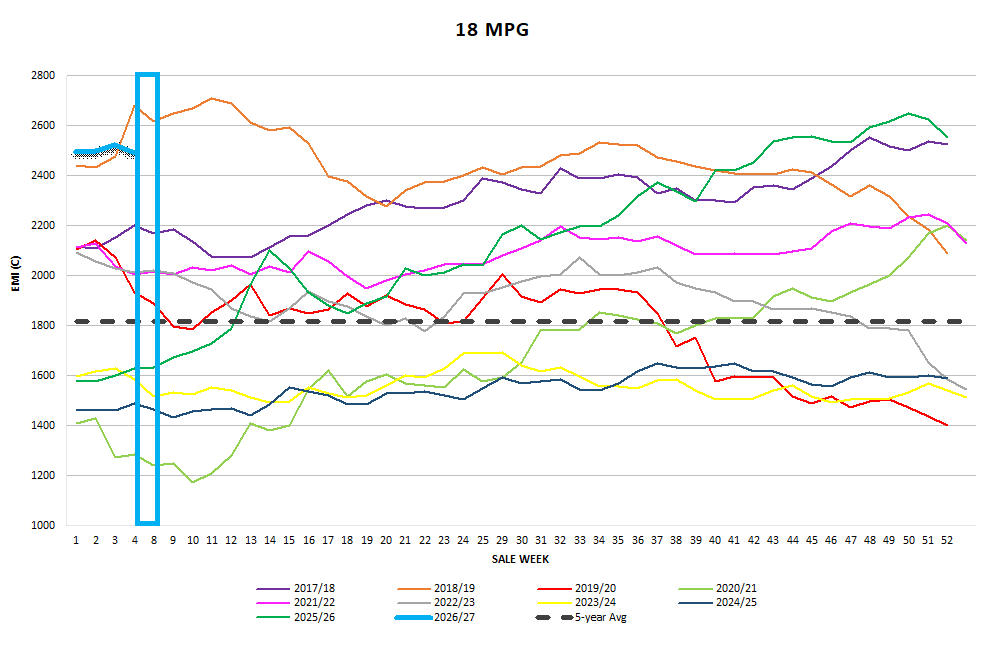

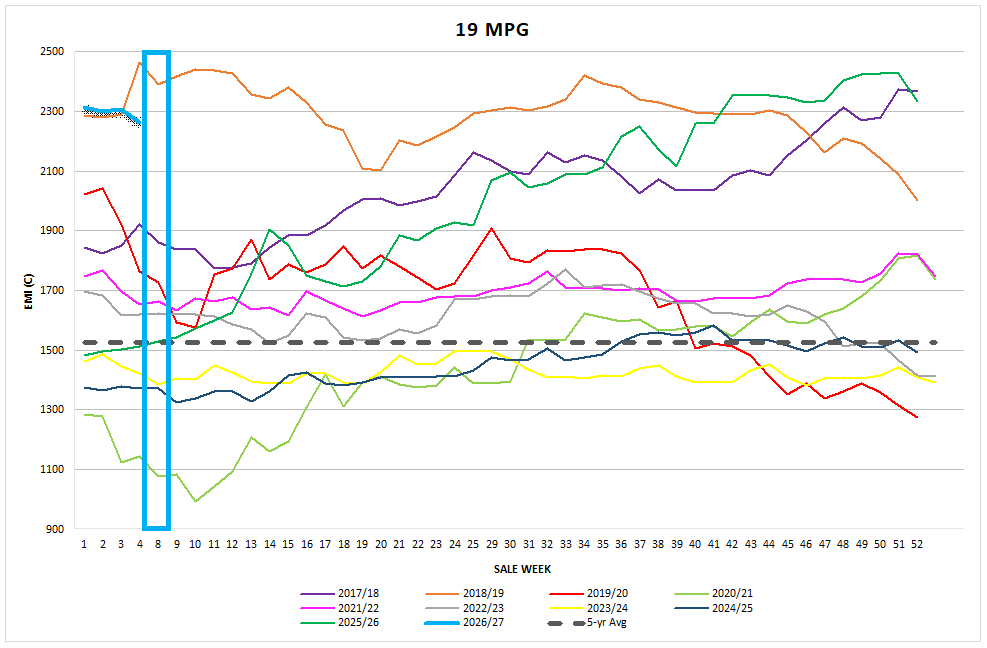

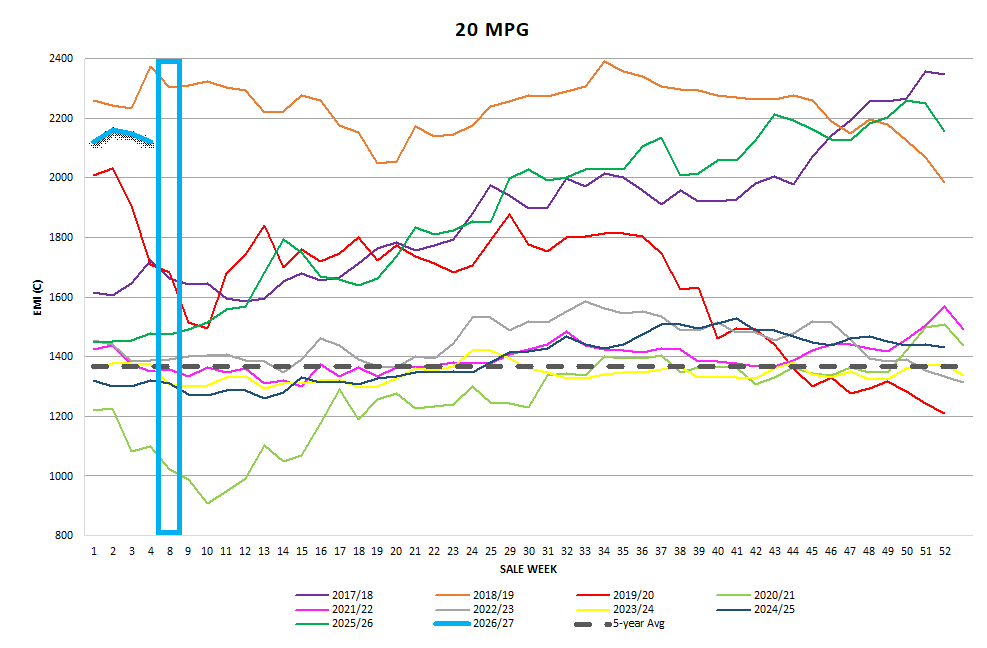

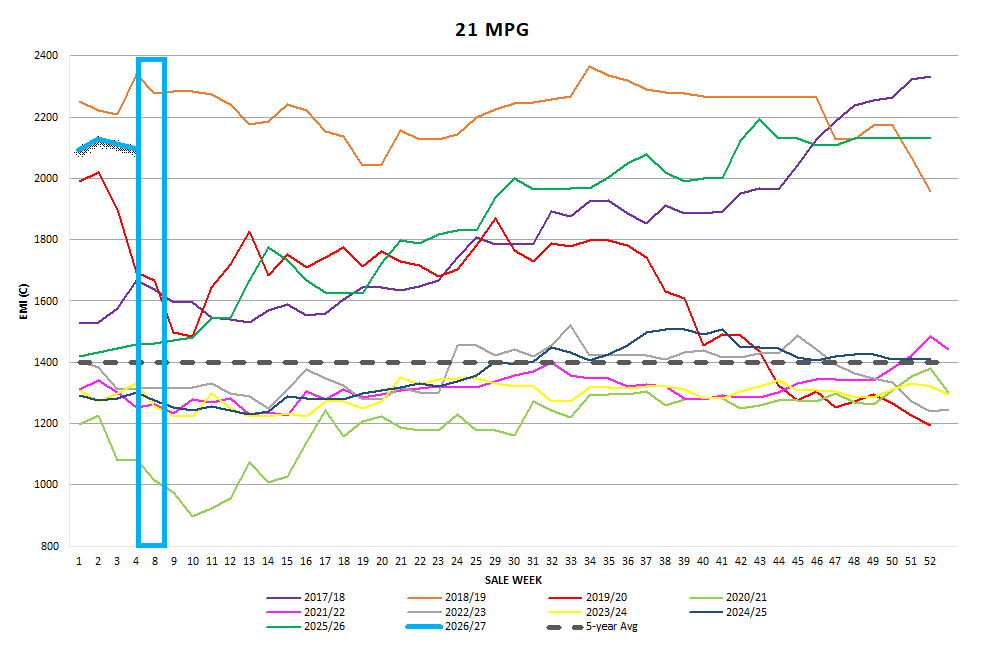

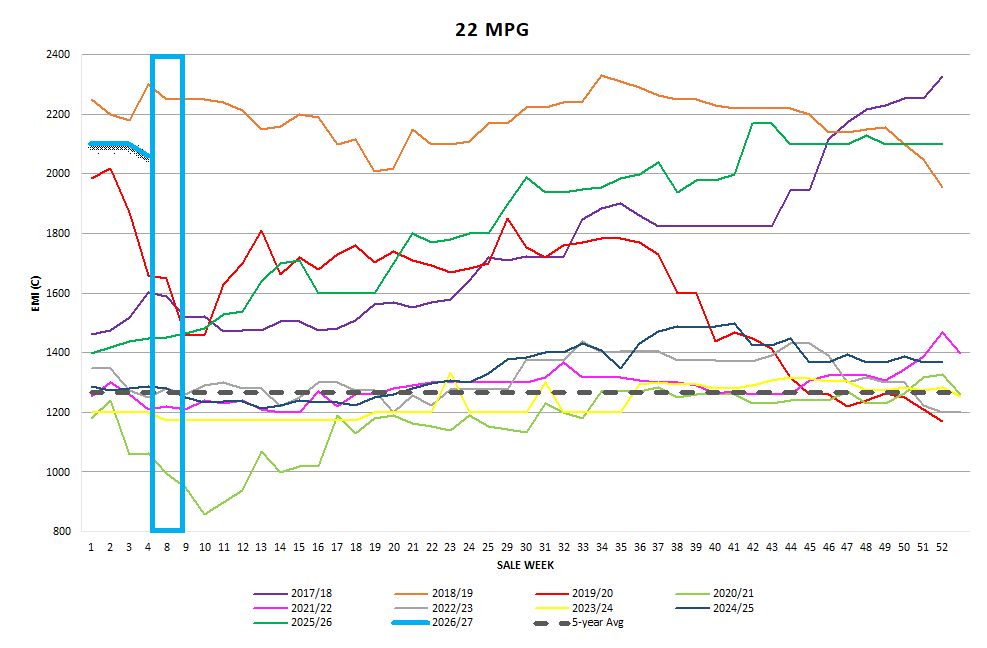

The AWEX EMI closed the week on 1873c, down 28c at auction sales in Australia. After spending 8 selling weeks over 1900c and peaking at 1989c, this week’s fall in the EMI supported the news of price resistance being felt by the top makers down the pipeline. In USD terms the EMI fell 18c to close on 1311 USc. It spent 15 weeks above 1300c in that time and spent just 2 weeks above 1400c. 31,751 bales went under the hammer as Fremantle returned to the last sale before the mid-year sale recess, with a severely reduce clearance rate of 84.7%. Whilst the increase in the pass in rate over the week may have been justified, the exporters I have spoken to reported reduced orders for the week as the prices that were being offered were somewhat unsatisfactory.

Merino Fleece

The Market opened slightly cheaper as prices continued to fall as the day progressed, with the EMI posting a 21c loss, and the Merino MPG’s posting 20-50c losses throughout the three centres. Whilst Wednesday saw the EMI fall just 7c there was some attempt recovery to secure stock which pushed the Northern 17µ and 18µ MPG’s up 12c and 15c respectively, whilst the remaining MPG’s struggled to maintain the previous day’s levels. Traditional “Italian Spinner” types attracted good competition however prices for average, good and best style lots were barely maintained.

Merino Skirtings

Merino Skirtings opened with falls of 10c to 30c on the opening day. Wednesday saw the market maintain this newly established price level for most skirting types with VM less than 8%. The best bulk and prepared pieces continued to attract price premiums which is consistent to the previous market sentiment.

Merino Cardings

Merino Cardings generally followed the market down with the exception of the Northern Region. Whilst all centres fell 20-34c on Tuesday, the Northern region MC posted a 26c rise on Wednesday to close the week up 5c. The more stylish selection offered in Sydney on Wednesday could be attributed to the Northern selling centres late price recovery.

Crossbred Fleece

Crossbred Oddments

Crossbreds

Crossbreds measured heavy losses between 40 and 50c clean for the week, to round out the negative market theme. Whilst Tuesday’s offering may have been swayed by poorer quality and cast lots, there was no doubt the price trend negative. By the market close it was noticeable that the 25µ-28µ MPG losses were more substantial and the 29µ and coarser crossbred types.

Next Week

Sales will resume in the week beginning Monday the 17th of August. ~Marty Moses

Market Commentary

Whilst it was inevitable that the wool market reached its “Everest Summit”, there is always a sense of loss as the price descends to base camp. I keep reminding myself as a wool grower and a wool broker that the EMI is 634c above this time last year, which is an price increase of 51% year on year. Reflecting on some highlights and lowlights over the past year is that we saw 17 Micron wool clips making over $3000/bale (up $1000/bale) whilst at the other end of the clip seeing wool having little or no value go from being used as erosion stabiliser in the creek to being worth $135 to $150 per bale.

This week the wool industry mourns the loss of Peter Ackroyd MBE, who passed away suddenly at the age of 76 in Bradford, England. Peter dedicated over 50 years to the industry, working across business development, research projects, textile innovation, and international promotion. He served as president of IWTO, was chairman of the Campaign for Wool (of which King Charles is patron), and for many years was a Global Strategic Advisor to AWI and Woolmark. I met Peter on several occasions; he was an imposing figure, and his contribution to the industry may never be surpassed. RIP Peter.

On a positive note for the Wool Industry, the boards of the Australian Wool Exchange (AWEX) and the Australian Wool Testing Authority (AWTA) announced formal discussions had commenced to explore a potential merger of the two industry-owned organisations. The decision reflects a shared commitment to exploring opportunities to streamline operations and strengthen industry services, with the goal of delivering greater value to industry participants. Both boards also recognise the potential to improve efficiency, integration, governance, clarity and responsiveness to meet the evolving needs of the industry.

Both boards have provided in principle support for the merger and will continue to undertake detailed work with the intention to provide a formal proposal to their respective members at upcoming AGMs.