Market Intelligence

Weekly Wool Market Commentary

Moses & Son is committed to providing our valued customers the most current information and data to empower your decision-making process. Discover our latest Australian wool market weekly update below, along with archived reports for your perusal and analysis.

2025-S04

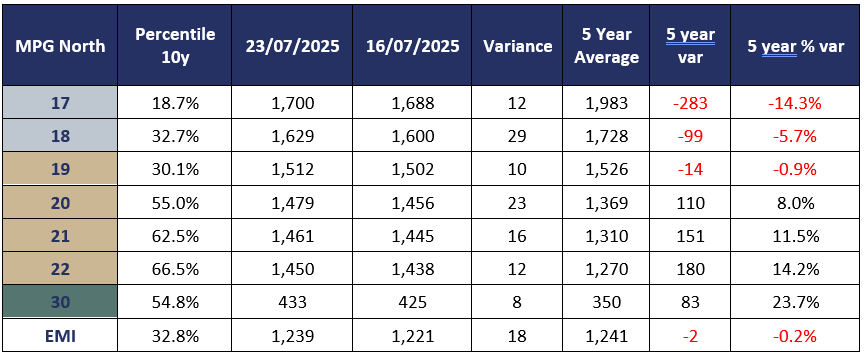

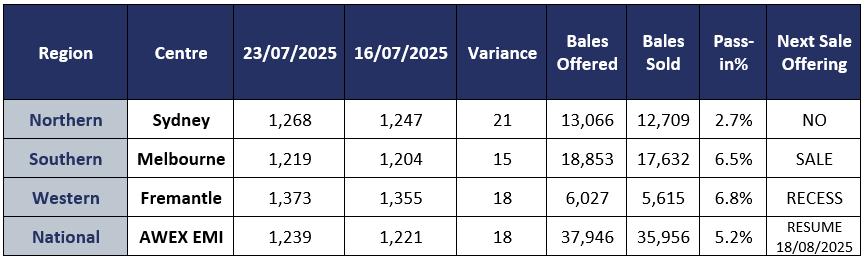

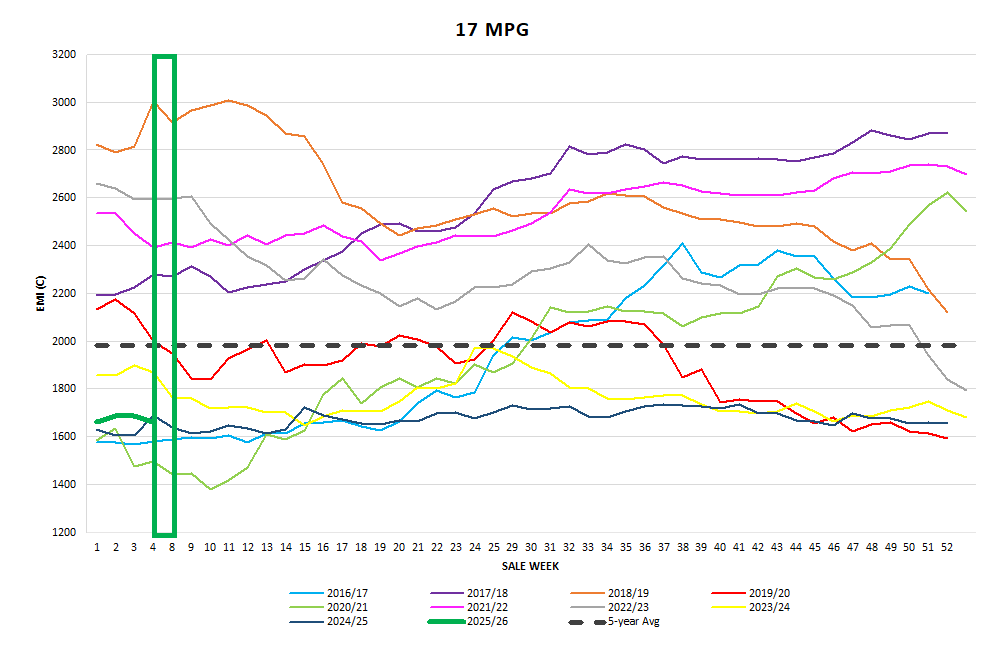

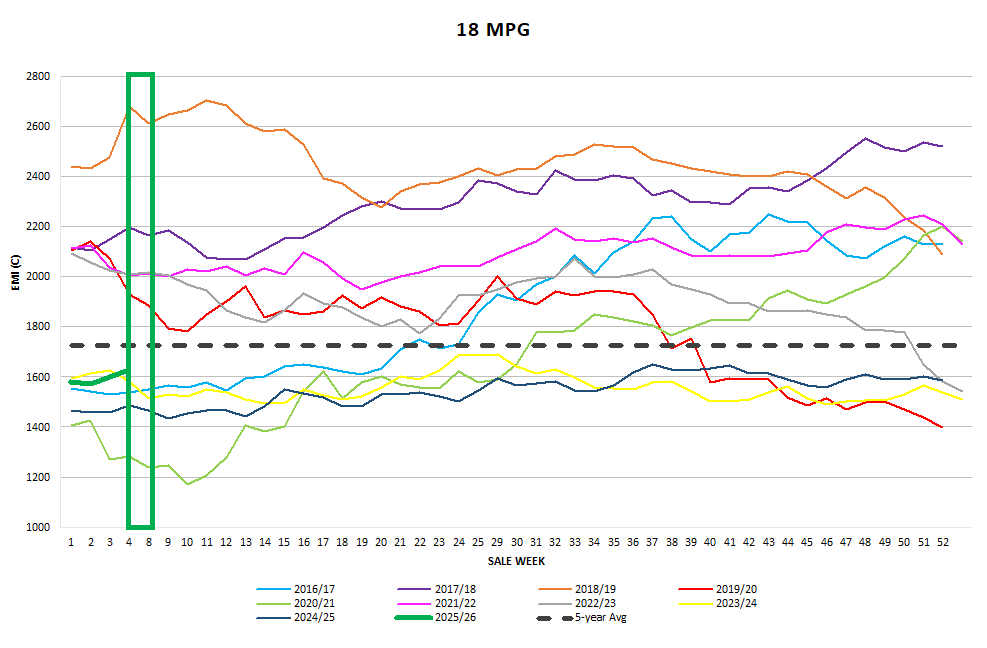

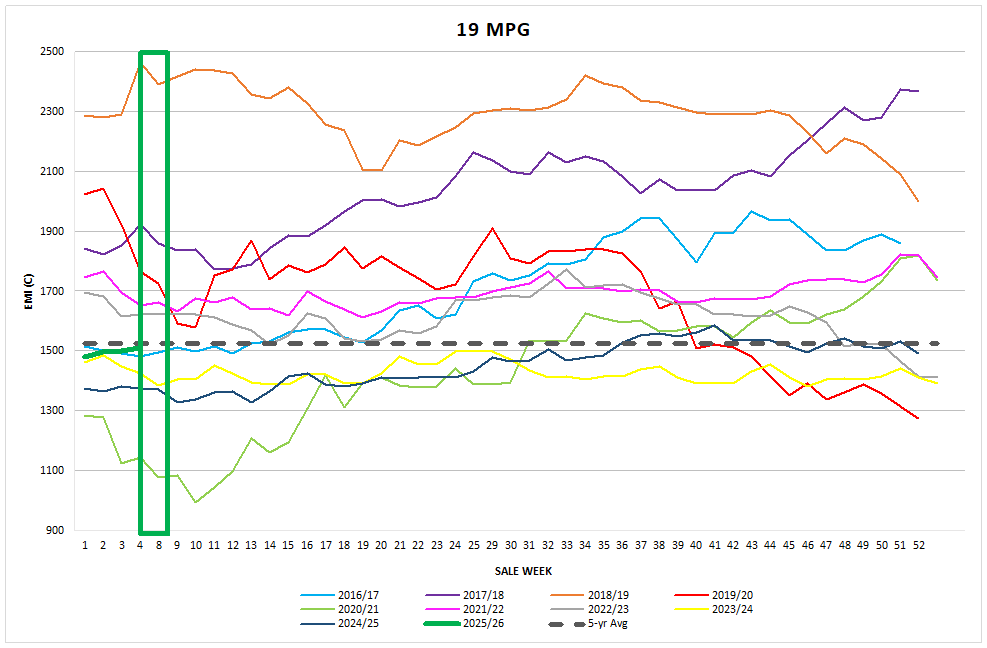

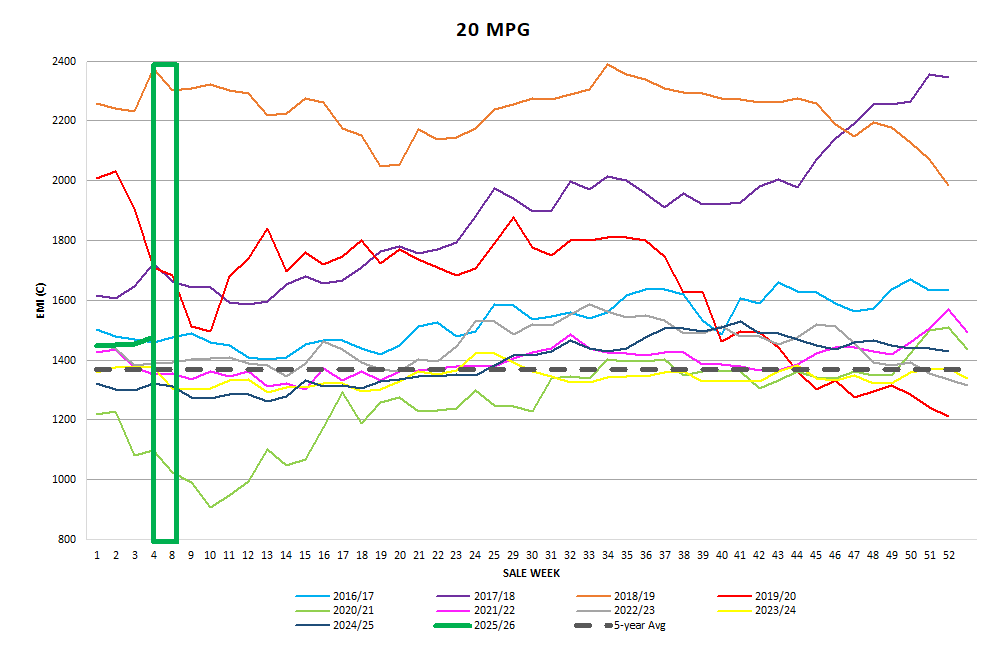

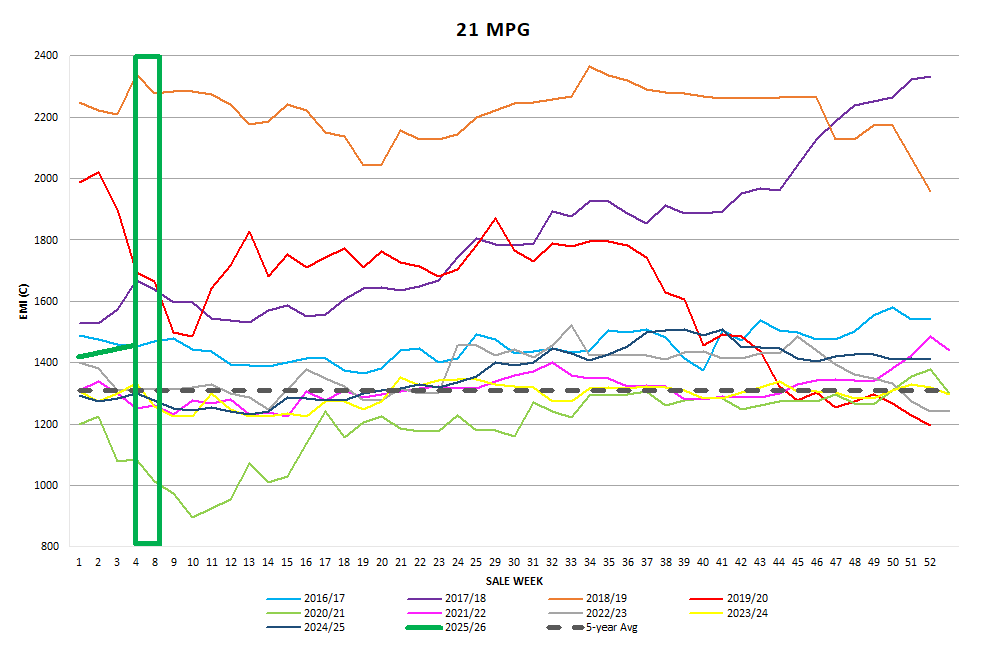

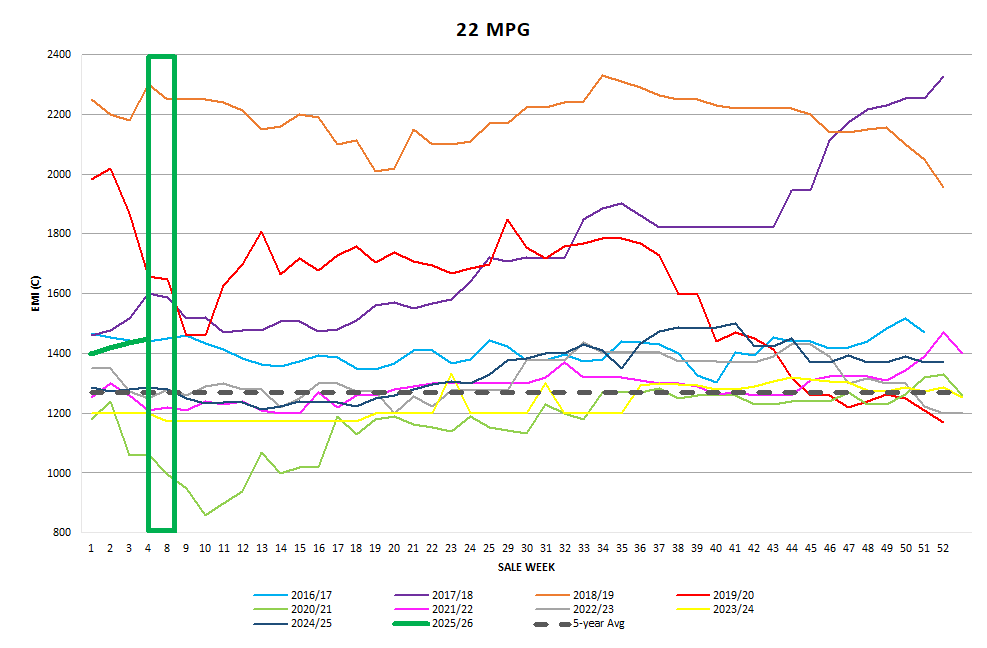

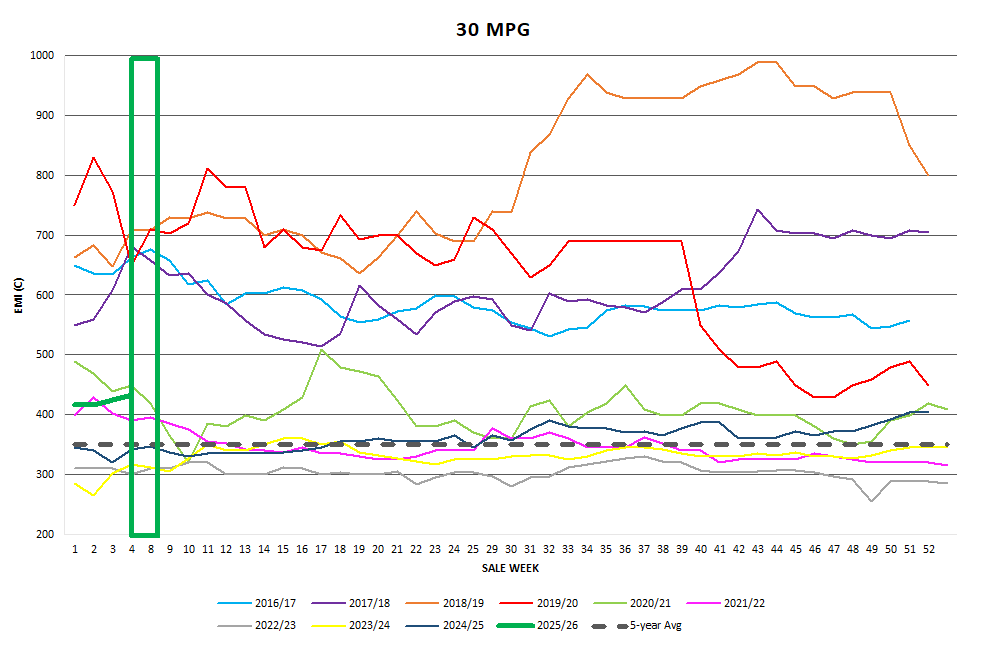

Week S04: 23/07/2025: The AWEX EMI closed on 1239c up 18c this week at last auction sale in Australia as we glide into the mid-year 3-week sale recess. The wool market continues to enjoy a strong start to the 2025/26 wool selling season with 4 consecutive rises in the EMI for the 2025-26 season. 94.8% of the 37,946-bale offering cleared to the trade. It was evident from the first lot that all categories of buyers were keen to compete on the offering and reports that the majority of the lots traded were for immediate shipment. Fremantle only offered on Tuesday where it posted a 18c increase to the WMI against the EMI which added +15c. Wednesday saw a consolidation of most MPGs across the Merino and Crossbred Indices. Within the selling days the AUD strengthened .44USc which saw the EMI in USD rise a significant 17c to close on 817 USc. This is the highest EMI in USD since January 2024.

Merino Fleece

posted some of the best weekly increases for some time with the upward range spanning 10c to 38c in the Northern MPG’s whilst the Southern MPG’s added 5c to 28c. All exporter categories competed aggressively on the Merino fleece offering With the Chinese Indent operators & Topmakers competing heavily with the 2 largest Australian Trading exporters, with the top 4 buyers taking 55% of the fleece offering. Whilst the participants can celebrate the small win it is still uncertain if the fundamentals that has been restricting the price levels of the wool market have changed but we can dream.

Merino Skirtings

free of heavy colour and cotts rose 10 -20c across the board on Tuesday and held their composure until the close on Wednesday. Purchasing competition was dominated by the Australia’s largest Trading Exporters who collectively purchased a “smidge” under 40% of the M Skirting offering.

Merino Cardings

reacted positively to the Northern region’s selection of well prepared and specified Merino Locks. The Merino cardings prices are noticeably defined by the micron with the coarser Locks Stains and Crutchings sold at substantial discounts. Whilst the Sydney MC were the shining star Melbourne added 6c and Fremantle adding 9c for the week.

Crossbred Fleece

Crossbred Oddments

Crossbreds

prices continued to creep upwards generally 6-8c rises measured across the XB MPG’s. Whilst the best specified lots attracted vigorous bidding, anything that fell outside of these for VM Length or CV Diameter is being substantially discounted.

Next Week

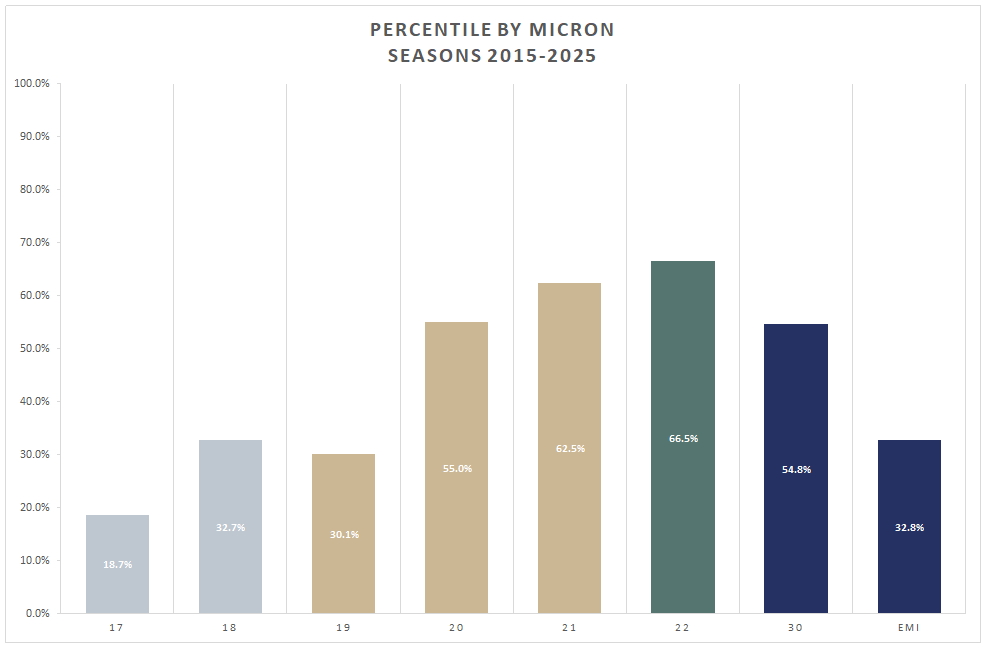

Graphs

Market Commentary

Exporters report whilst we had a great week and firm closing tone once the exporters filled their orders so far they have shown little interest in pushing further. The markets cumulative rise over the past 4 weeks painted a better picture for the resumption of sales on the week beginning the 18th August. Appreciating AUD Currency Exchange rates with the USD may have squashed that mood before it had a chance to gain momentum. On Thursday, this week, the AUD punched through the 66 USc barrier effectively turning off any chance of continued business over the break. US tariffs were in the news again with agreements being progresses with Japan and the EU. This set the markets alight and strengthened the AUD. The other fear I have is the volume of wool accruing for the first sale back S08/25 on the 19th August. So now we have to new things to pray for. The AUD to fall back towards .65USC and for Brokers to roster no more than 45,000 bales on offer in the first sale back. ~ Marty Moses.