Market Intelligence

Weekly Wool Market Commentary

Moses & Son is committed to providing our valued customers the most current information and data to empower your decision-making process. Discover our latest Australian wool market weekly update below, along with archived reports for your perusal and analysis.

2025-S09

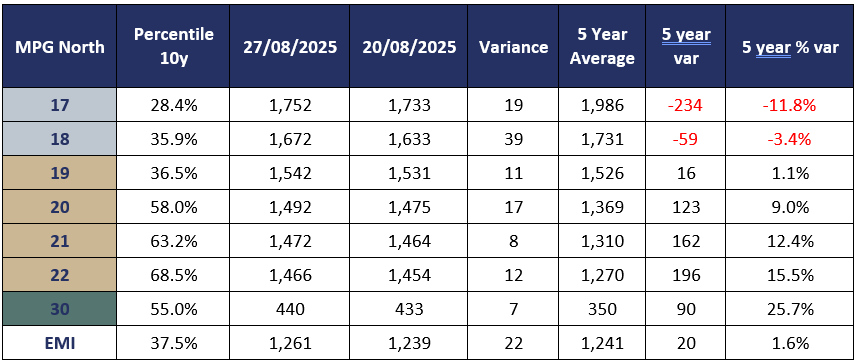

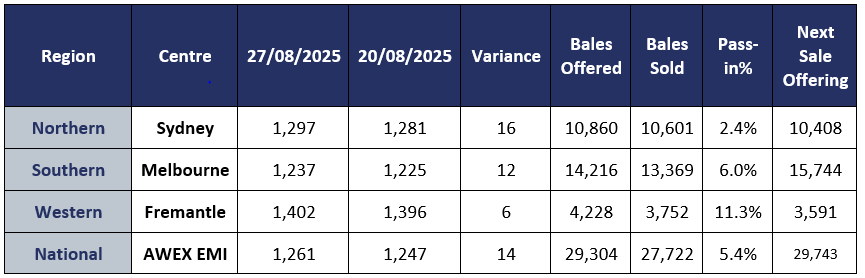

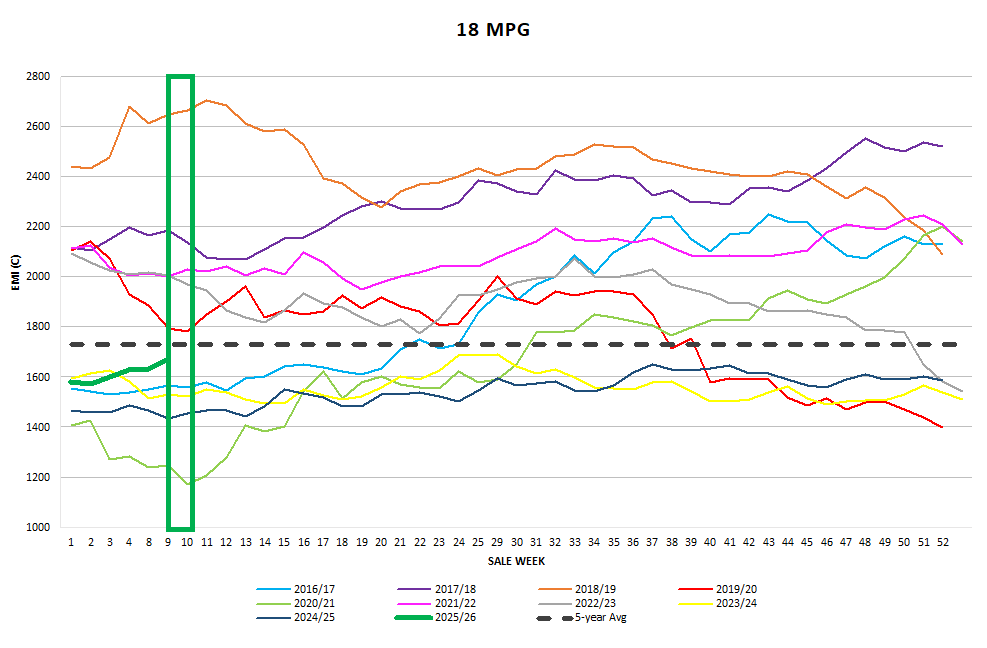

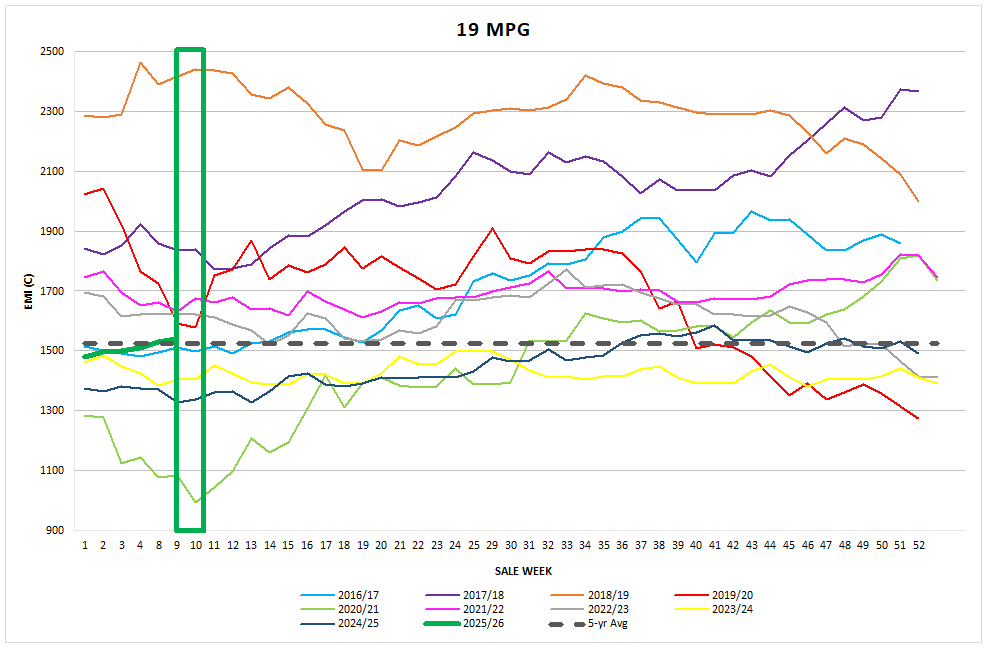

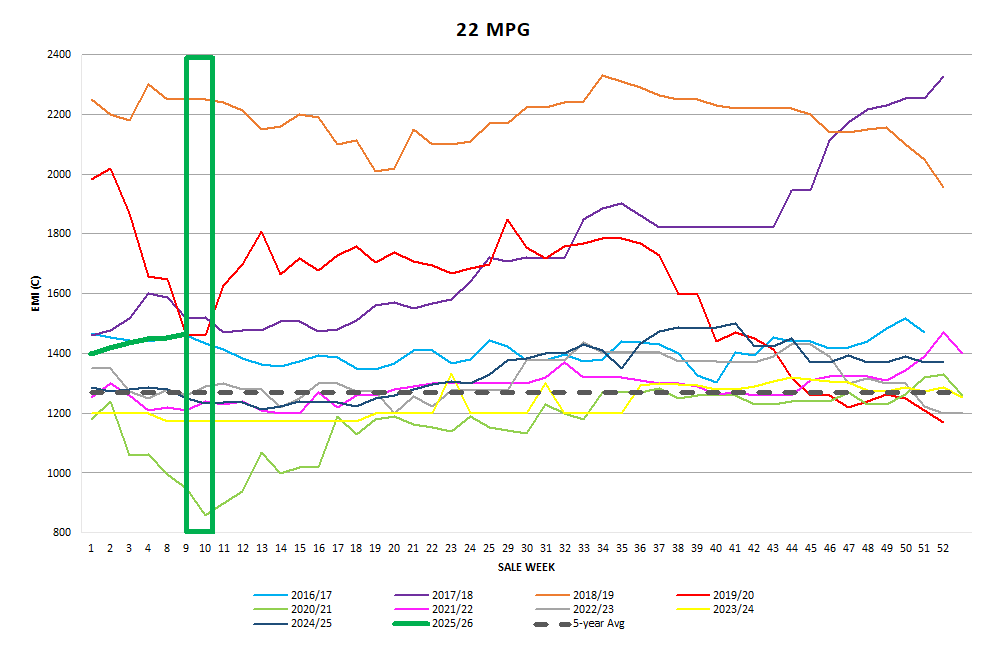

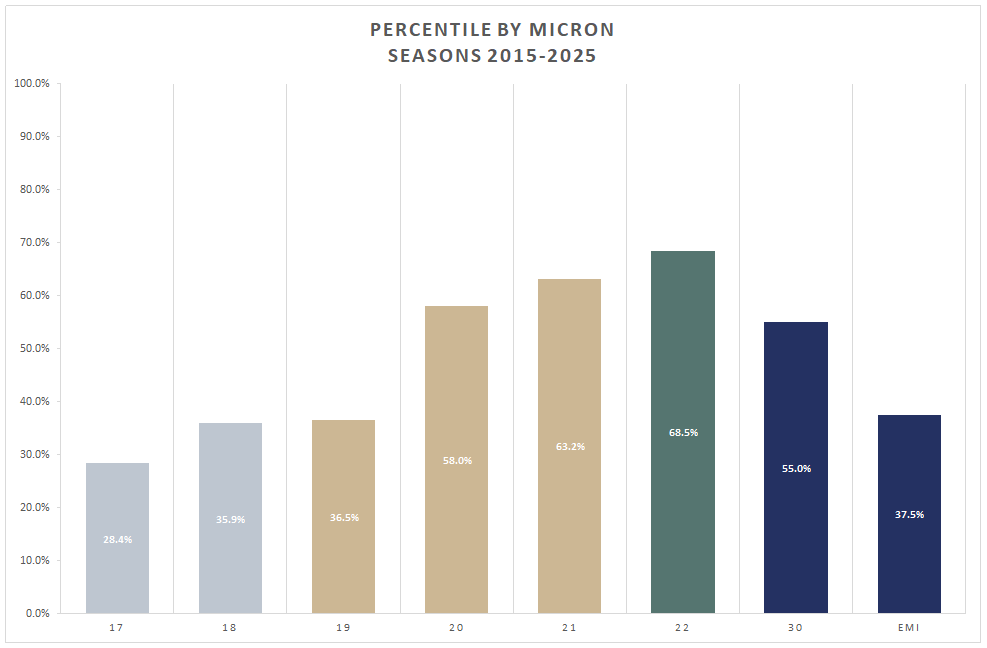

Week S09: 27/08/2025: The AWEX EMI closed on 1261c up 14c at auction sales in Australia this week. The EMI posted 7c rises over both selling days with the EMI in USD terms also rising 14c for the week. The national offering fell back to 29,304 bales for the week with Fremantle offering on Tuesday only. 94.6% of the offering was cleared to the trade with the northern region passing in 2.4% whilst southern region pass in was 6% and the West 11.3%. Exporters and (Indents) mill buyers were intent to continue their positive approach to buying, and most grower sale lots achieved returns of 10 to 20c over the previous week’s levels. The EMI has added 53c over July and August posting the 6th consecutive weekly rise and the 10th in a run of daily rises this week. Brokers are reporting large reductions in receivals over the past month due to “wet weather” however the AWPFC have released their August Forecast with the predicted wool production set to fall 10.2% in the 2025/26 season (from 280 Mkg to 251.5 Mkg). The question is being asked “is the quantity of wool really there?”.

Merino Fleece

saw the northern markets open up to 30c clean dearer and continue that trend on Wednesday with the 18.5µ and coarser adding another 10-15c. It is still impossible to determine if this week’s rise in the US value of wool purchases is driven by confidence emerging throughout the pipeline or fear of the lower production forecast.

Merino Skirtings

Whilst the FNF Best broken types added 10-20c for the week the prices for the main types did not follow dearer prices for the fleece types however the market was fully firm across the range of types and VM content.

Merino Cardings

saw another uneventful week with price levels remaining firm. Buyers favoured the best bulk and colour for their combing orders however the Carbonising types remained unchanged.

Crossbred Fleece

Crossbred Oddments

Crossbreds

saw steady rises across the micron range in all centres. The highlight for this sector emerged on Wednesday where vigorous competition for 25.5-micron fleece types forced prices up to 40c dearer for the day. Given the XB sector has seen YOY rises between 25% and up to 40% in some MPG’s, the projection for this sector is for a slight retracement in price over the next month but nothing to be alarmed about.

Next Week

offering remains under 30,000 with 29,743 bales on offer across all centres Tuesday and only Sydney and Melbourne offering on Wednesday. The market intelligence emerging from this week is that despite the Chinese processors continually challenging the current cost of wool and the absence of Indian and European competition the market should maintain these levels in the short term. ~ Marty Moses.

Graphs

Market Commentary