Market Intelligence

Weekly Wool Market Commentary

Moses & Son is committed to providing our valued customers the most current information and data to empower your decision-making process. Discover our latest Australian wool market weekly update below, along with archived reports for your perusal and analysis.

2025-S10

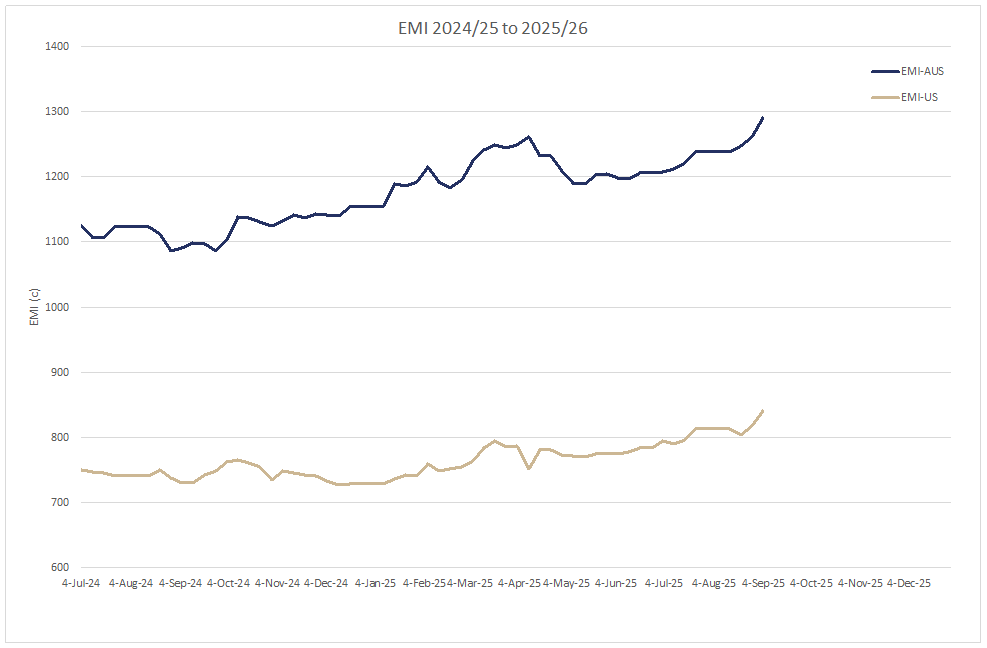

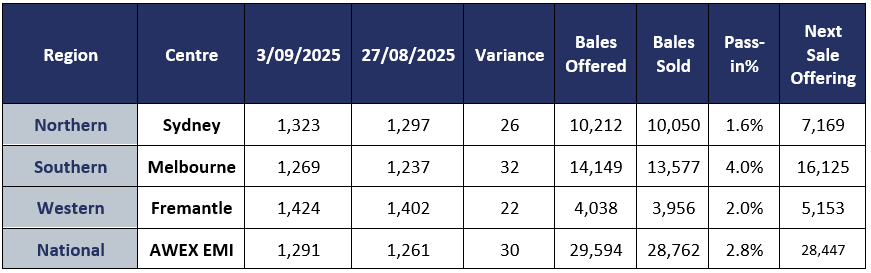

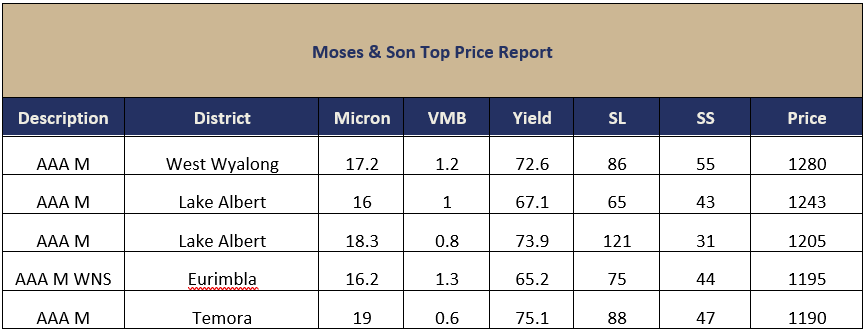

The AWEX EMI closed the week on 1291c, up 30c at auction sales in Australia. 29,594 bales were offered this week with a 97.2% clearance rate indicative of the increase in buyer urgency to complete orders. In USD terms the EMI rose 24c, closing the week at 842 USc with the AUD increasing .36c week on week. The low volume of bales offered this week has kept upward price pressure on the market, with the EMI achieving its 7th successive weekly rise, which we have not seen since 2019. Adding to that it is the first time in 46 years the market has risen continually for 7 successive weeks at the start of the new selling season. The EMI rose 17c on Tuesday with Wednesday adding another 13c to the EMI. The Individual MPG’s and the MC Indicators all closed in positive territory in all centres.

Merino Fleece

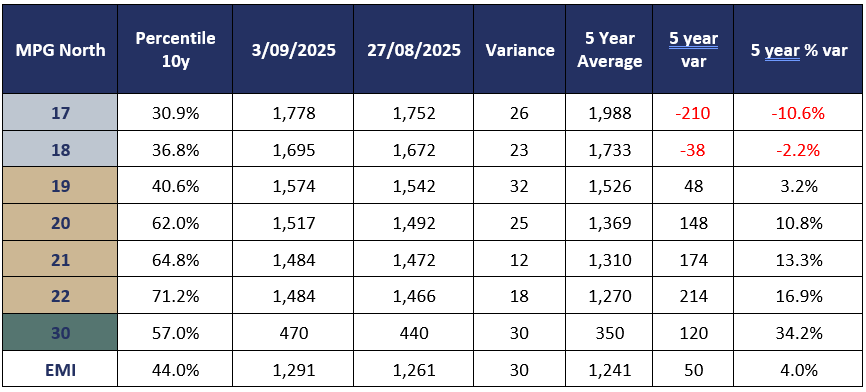

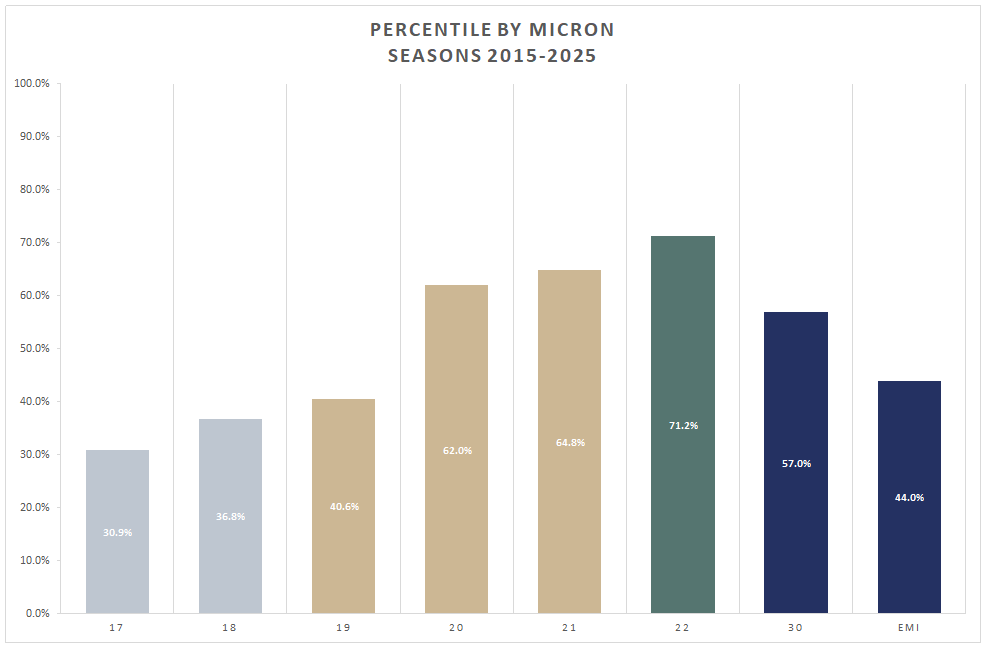

saw the lower weekly quantities on offer drive the price rises across all MPG’s ranging from 23c-42c in the northern region, 18c-45c in the southern region and 20-39c in Fremantle (Offering on Tuesday only). A significant milestone was achieved for the 21 MPG which reached its 99th Percentile price ranking (southern MPG). Australia’s largest trading Exporters pushed the Chinese Topmakers and indent buyers for the majority of the lots. Best style and specified, Certified Non Mulesed lots continued to attract elevated premiums in the market.

Merino Skirtings

followed their fleece counterparts upward with premiums for the best style and prepared FNF “Brokens”. As in the fleece category buying domination came from Australia’s 2 largest trading Exporters who collectively purchased 42% of the national skirting offering.

Merino Cardings

and oddments experienced good rises on Tuesday whilst maintaining theses gains on Wednesday. Whilst price gains were varied across the selling centres, everything is heading in the right direction.

Crossbred Fleece

Crossbred Oddments

Crossbreds

were continued on their steady upward price trajectory. Despite the absence of a few traditional competitors in this sector competition remained widespread. The southern 28 MPG reached the 97th percentile price ranking (5-year) whilst the 30 MPG hit a 100th percentile price ranking (5-year).

Next Week

national offering slips back to 28,447 bales with Fremantle offering on Tuesday only. The market should continue to support the current price levels simply based on the low supply issue. Happy Father’s Day to all the Dads, Grand Dads and Great Gran Dads. ~ Marty Moses.

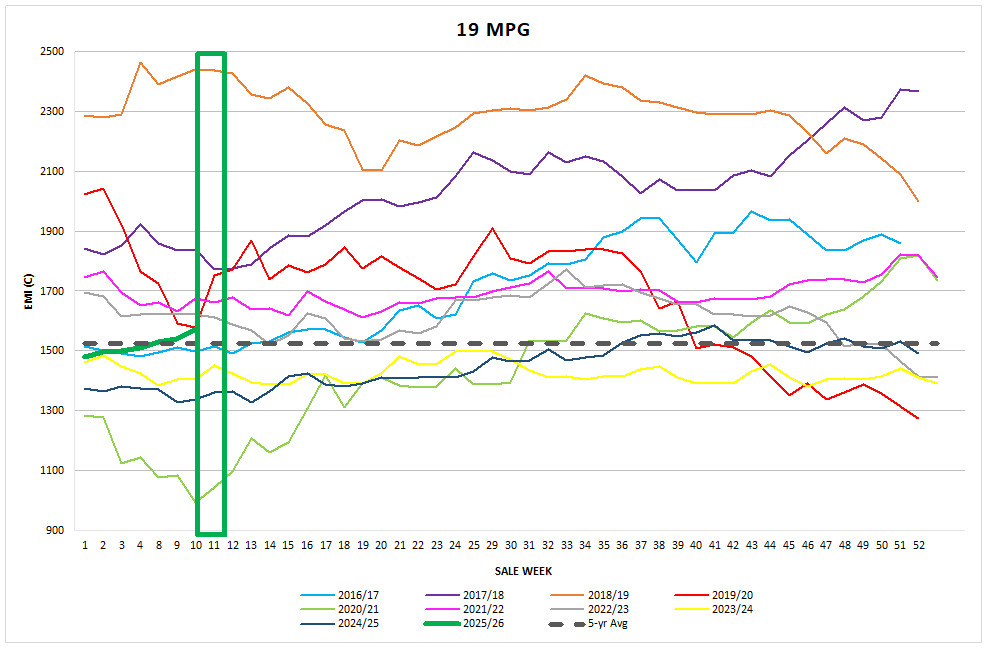

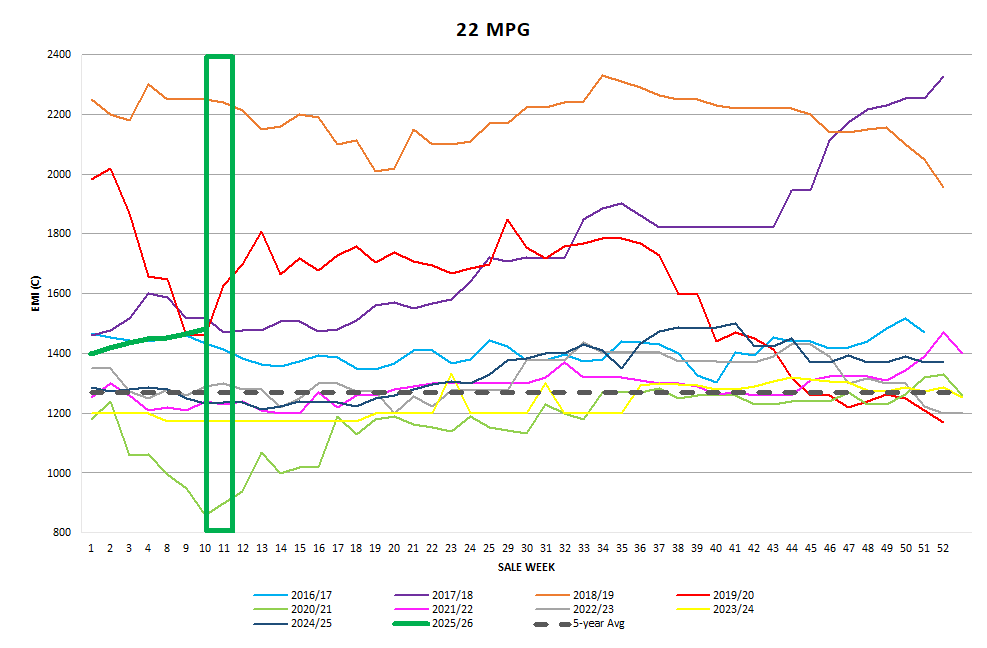

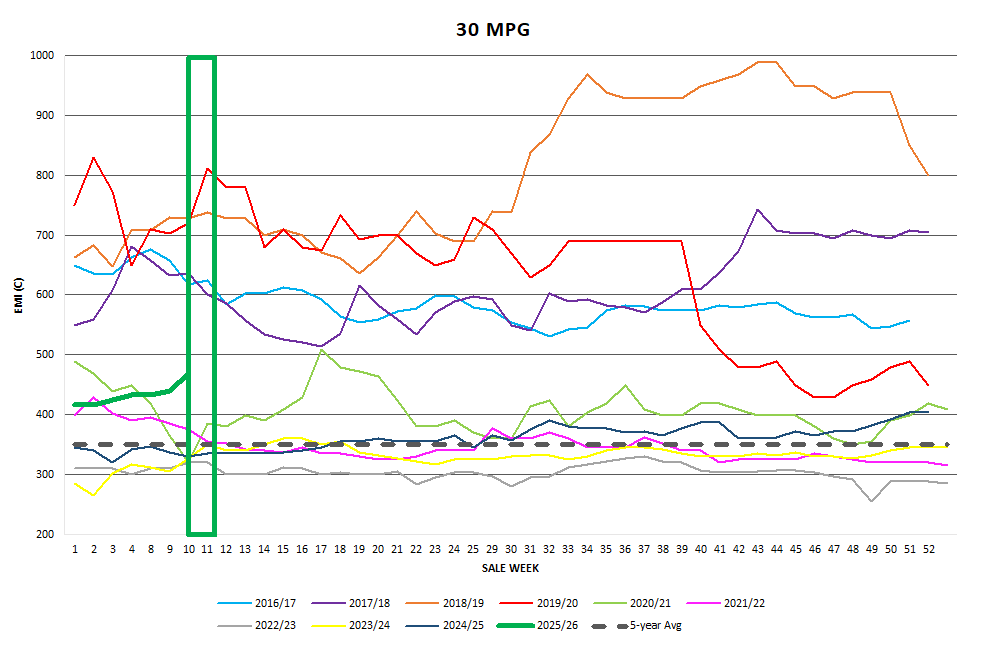

Graphs

Market Commentary

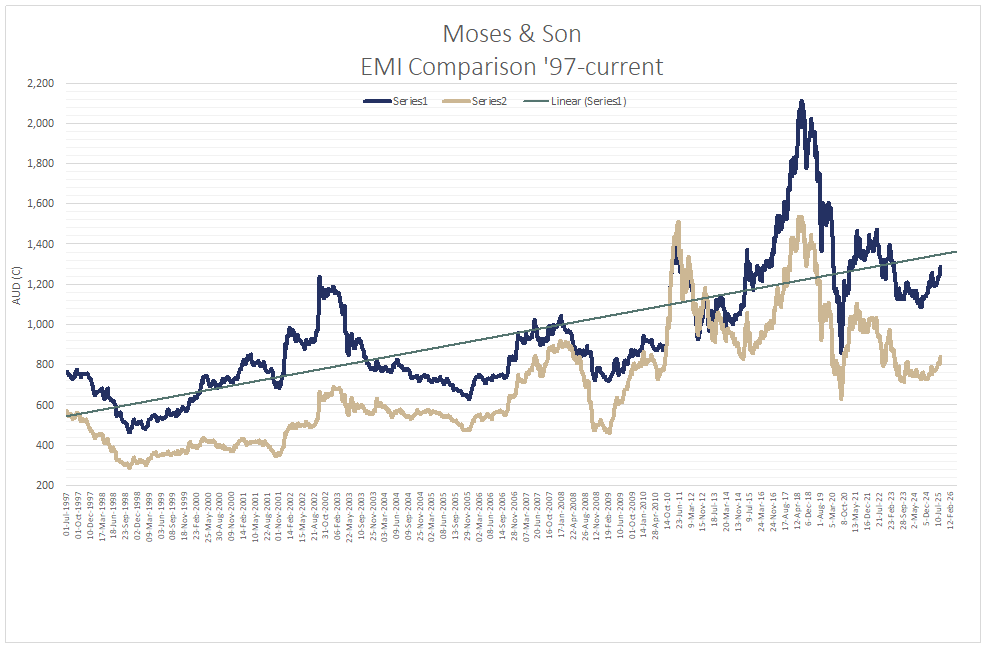

As the wool pipeline digests the latest release of its Wool Production Forecast which predicts the upcoming season to produce 251.5 Mkg, the lowest production since 1921. The most alarming fact is that Wool 251.5 Mkg represents just 24% of the Australian production in 1990. There is no doubt in my mind that the current price increases are supply driven rather than consumer demand driven, however, the time will come when the world economic drivers reconcile. The 64 Mkg is “When”? The total weight tested for the month August 2025 is 24.8% lower than August 2024. The progressive comparison of total weight tested for July to August 2025 compared with the same period last season is 18.2% down. AWTA Ltd has tested 33.0 mkg this season compared with 40.4 mkg for the equivalent period last season. In industry news AWI CEO John Roberts has announce he will stand down from his role after AWI AGM in November. John commenced in the CEO role in March 2022 and has worked with AWI since 2016. More information on the Board Nominations and how to ensure your vote is counted at the AWI election is coming soon. In same week as this announcement of NCWSBA has issued a joint press release with ACWEP & WPA emphasizing the need for informed market information be provided to our wool grower clients around the issue of demand for non-mulesed wool. This is in response to the latest report of the Chairman of AWI (Jock Laurie) suggesting there was no evidence of a premium for CM/NM wool. This week a major exporter revealed an increasing number of claims emerging from their processor customers on a number of quality issues especially from Unclassed (D Cert) wool Clips. As you would be aware, the combination of low prices and increasing cost of shearing has progressively seen contractors and producers adopt the practice of dropping a classer from their team. The take home message is that in a 2 and 3 stand shed the cost differential of adding a classer is somewhere between 7 and 10c clean but the discount could be as much as 50-100c clean. Now that Crossbred prices are more viable the discount for unclassed XB clips will continue to grow.