Market Intelligence

Weekly Wool Market Commentary

Moses & Son is committed to providing our valued customers the most current information and data to empower your decision-making process. Discover our latest Australian wool market weekly update below, along with archived reports for your perusal and analysis.

2025-S11

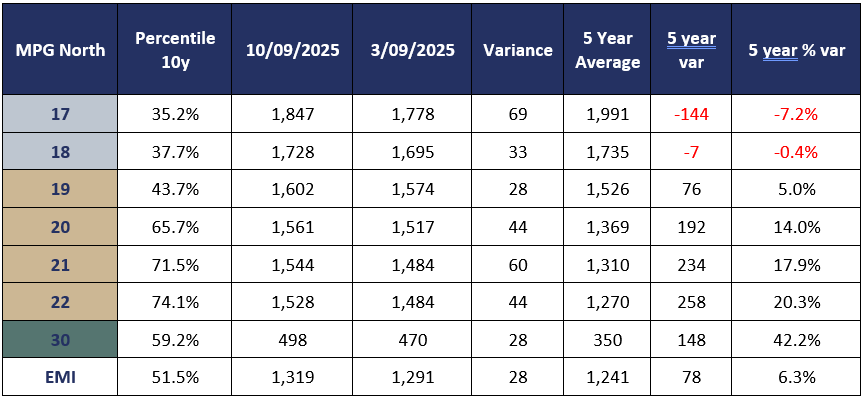

The AWEX EMI closed on 1319c up 28c at action sales in Australia this week. As I mentioned last week, the current 8 weekly rise in the EMI is the longest weekly rally in 6 ½ years and on a daily basis the rally has now run for 14 straight sessions, not seen since 2011. A rare feature was the 97.3% of the 27, 544 bale offering transacted this week, with the other feature being the 30 USc rise in the EMI to close on 872c. December ‘23 was the last time arise in the EMI in USD of this magnitude was achieved. Australia’s lower wool production forecast coupled with a string of historic smaller weekly offerings, are now really creating some competitive tension amongst the Chinese Topmakers.

Merino Fleece

Merino Fleece saw the market open immediately in positive territory with the 17.0 and 17.5µ MPGs fleece lots adding 40+c to their previous week’s levels. The other MPGs were 18c-35c dearer. Competitioncame from Australia’s largest Trading Exporters whilst the Chinese Topmaker sand Indent operators were in hot pursuit. Wednesday saw the continuation of this trend with most MPG’s adding another 5c-10c the 17 MPG continued to be the outstanding performer, added 27c to finish the week 69c dearer.

Merino Skirtings

Merino Skirtings followed their fleece counterparts upwards adding 20-30c on Tuesday and another 2-5c. Competition came from a similar mix of exporters as to the fleece.

Merino Cardings

Merino Cardings closedin positive territory with Sydney + 14c, Melbourne + 8c and Fremantle +23c

Crossbred Fleece

Crossbred Oddments

Crossbreds

Crossbreds on Tuesday saw the 26 MPG rise 30con nominal quotes with other MPG’s up 10c whilst Wednesday saw these prices consolidate. As the XB MPG’s are approaching or exceeding their 5-yearpercentile pinnacles and short term looks a little more promising for this market sector.

Next Week

Next week’s offering sneaks back up to30,992 bales. Is this the market resurgence we have been waiting for? Or just a reaction to the reduction in wool production in Australia and the subsequent lower weekly volumes on offer. My sources are indicating that demand has not shown any improvement at the retail end and the current price increases are most likely processors keeping their machinery ticking over. China’s domestic retail activity remains supressed with online shopping in the cheaper productsectors prominent. Europe is also lagging in the retail activities in thetextile sector. So, I expect the sharp rise in the EMI in USD terms might slowor reverse the trend next week and in the short term. ~Marty Moses

Graphs

Market Commentary

Some positive news emerging from AWEX was the announcement of the celebration of the 1 millionth bale being processed through WoolClip.

The Australian Council of Wool Exporters and Processors (ACWEP), the National Council of Wool Selling Brokers of Australia (NCWSBA), and WoolProducers Australia (WPA) today issued a joint statement re-emphasising the urgent need for a unified industry strategy on mulesing. This follows comments made by Australian Wool Innovation (AWI) Chairman Jock Laurie, which the organisations believe understate the significant and growing risks facing Australian wool in key international markets. It seems the battle lines are now drawn!!

Wool Industries Australia (WIA) has announced its support for the Australian Wool Sustainability Scheme (AWSS), recognising it as the preferred certification framework for Australian greasy wool – covering farm through to scouring. WIA Chairman David Michell said sustainability certification is becoming essential to maintaining access to premium global markets and building demand for Australian wool.