Market Intelligence

Weekly Wool Market Commentary

Moses & Son is committed to providing our valued customers the most current information and data to empower your decision-making process. Discover our latest Australian wool market weekly update below, along with archived reports for your perusal and analysis.

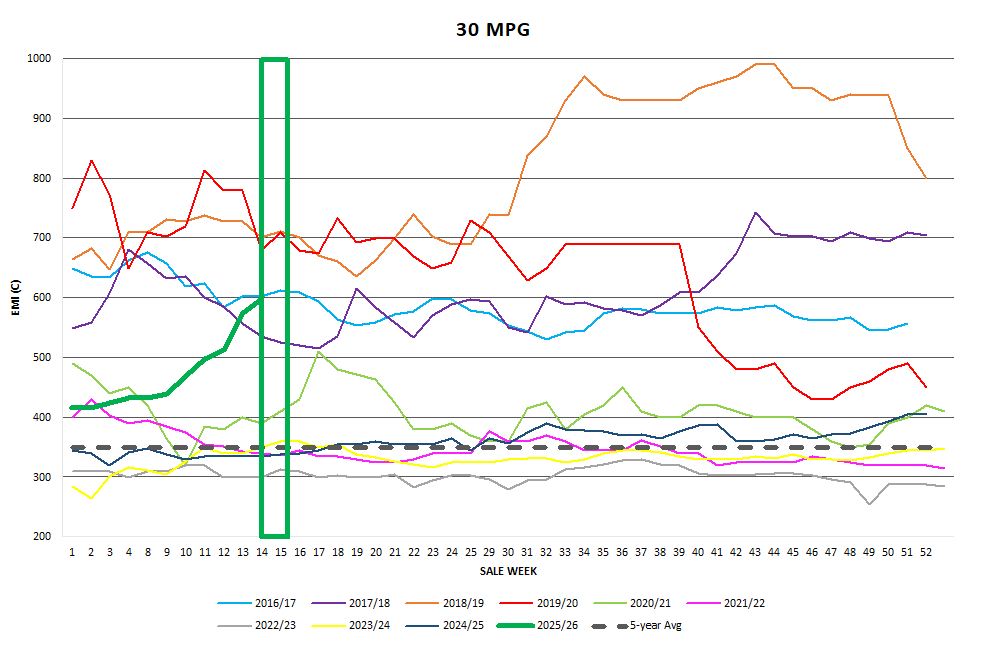

2025-S14

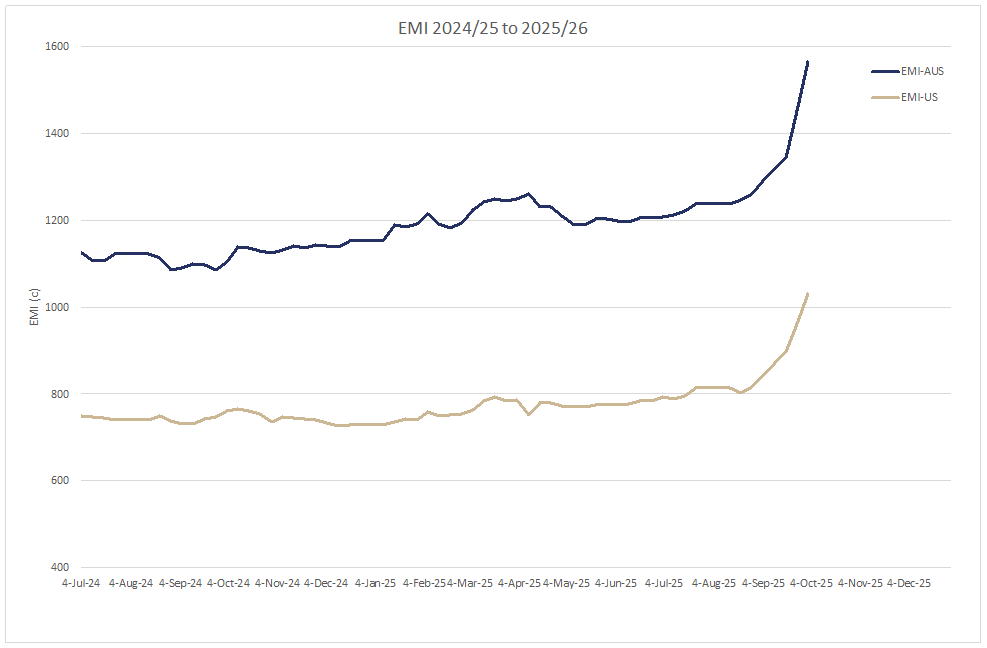

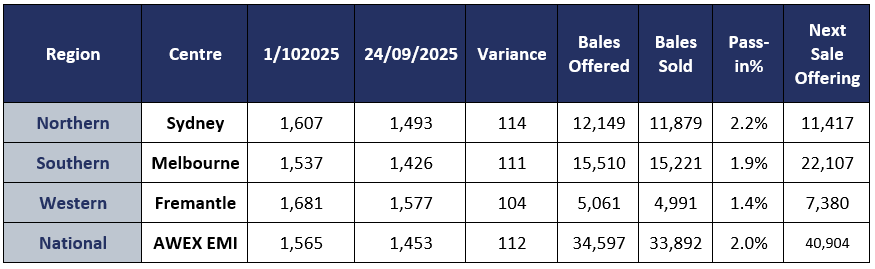

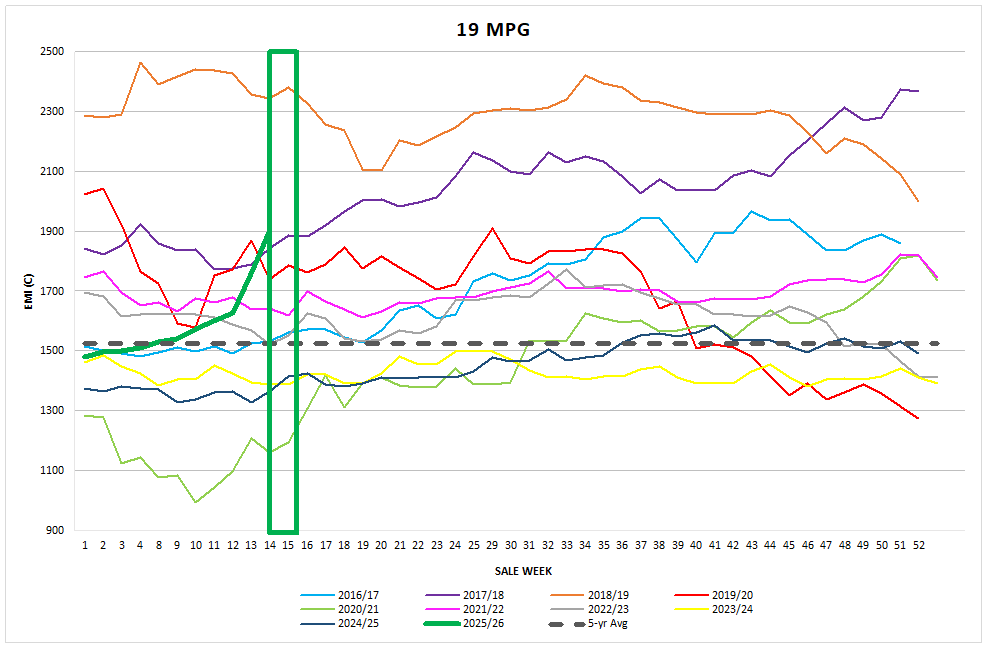

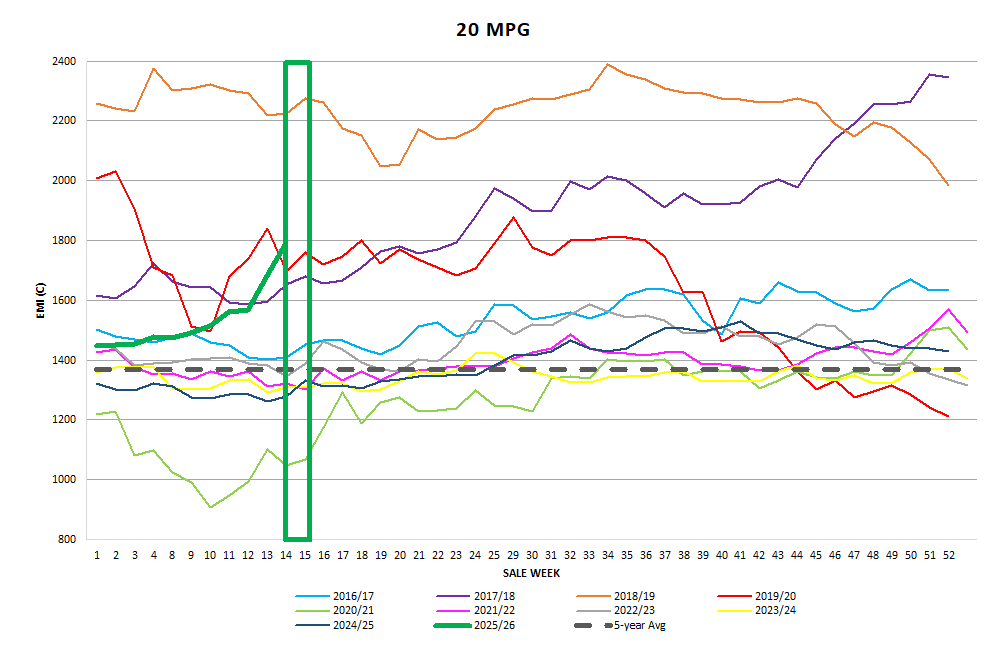

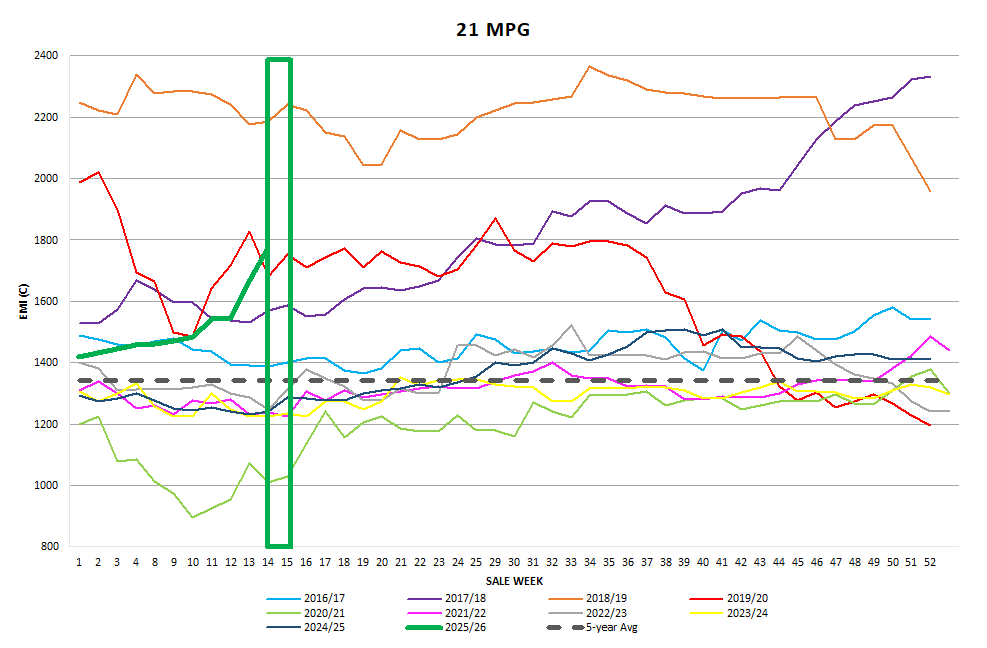

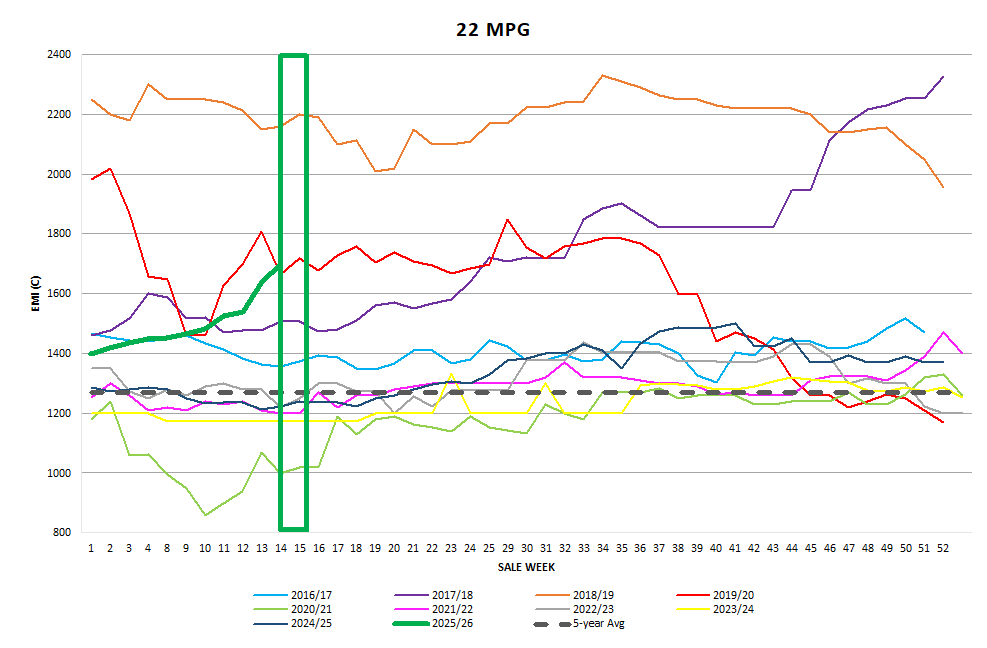

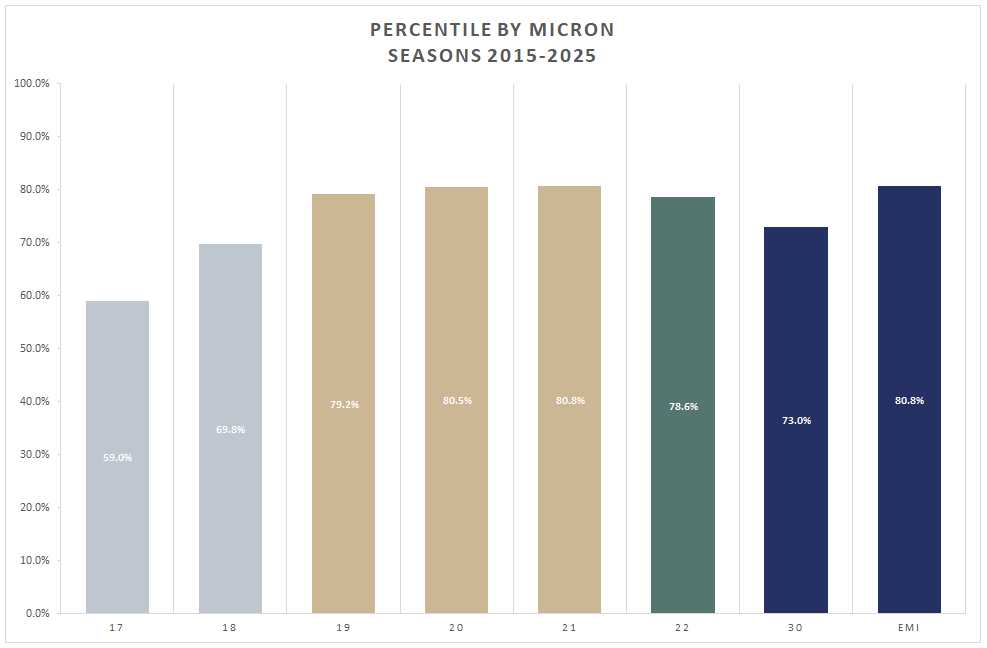

The AWEX EMI closed the week on 1565c, a 112c rise, and the 5th largest weekly rise since AWEX started recording. Last week’s EMI rise of 109c drew a few more bales onto the market with this week’s offering climbing to 34,597 bales. 98% of the offering cleared to a bullish cohort of Australian Trading Exporters and Chinese Indent and Topmakers seemed keen to pursue purchasing at any cost. The EMI currently sits 461c or 42% above the EMI at the same time last year, furthermore its 11 straight week rally is the longest positive market run since 1987, adding 358c to the EMI. This week’s culmination in EMI rises, markslargest unbroken cumulative increase in the AWEX EMI since 1979. Currency exchange rates had little or no influence on the market as the EMI rose 7.7% in AUD and 7.2% in USD.

Merino Fleece

16.5 MPG rose 221c whilst the 17 MPG was up another 180c. The remaining MPG’s rose between 110 and 179 and it seems the finer the micron the larger the rise. The 4 largest buyers in these sectors accounted for 65.8% of the purchases.

Merino Skirtings

Followed the fleece trends upwards with reports of strong demand driving the extreme demand. The 4 largest buyers in this sector accounted for 62.6% of the purchases.

Merino Cardings

remained in demand with the standard Carbo types posting 7-15c rises for the week, while the best colour and slightly longer cardings rose strongly. The Northern MC rose 15c whilst The Southern and Western MC’s went up 7c.

Crossbred Fleece

Crossbred Oddments

Crossbreds

Tuesdays XB market opened very strong with the Northern 26 and 28 MPG’s posting 44c and 42c respectively. The Southern MPGs ranged between 20c to 73c on Tuesday. Wednesdays XB market held the previous day’s price rises and some MPG’s rose another 2-5c. The top 4 buyers accounted for 55.7% of the Crossbred offering purchases. Well prepared XB fleece found favour amongst some buyers.

Next Week

offering increases to 40,904 bales, the largest offering since the return to sales after the 3-week recess in week 8. Whilst Exporters remain generally positive with the renewed vigour in the wool market, it is widely felt this week overshot the sustainable price level by a fair margin. I won’t be surprised if the market experiences some retracement in the past two-week record-breaking price rises. Processors will have made solid profit margins on their processed inventory over the past few weeks but will feel the pinch when they are buying at this level to replace that stock. It goes without saying “I will be happy to be wrong”. ~Marty Moses.

Graphs

Market Commentary

Whilst the market rise was the headline the underpinning news on supply took another hit. AWTA report further reduction in the bales sampled in September 2025 down-12.9% compared to September 2024, this takes the bales sampled in July 1-September 30 period down 16.2% compared with the same period in 2024. AWTA Ltd has tested 56.1 mkg (million kilograms) this season compared with 66.9 mkg for the equivalent period last season. Despite this wool sold figures in the same time frame are on a par with the July – September 24 figures. This can only be possible by the reduction in the pass in rates and the weekly content of wool tested before the 1st July 2025. Unfortunately, you can only sell it once.