Market Intelligence

Weekly Wool Market Commentary

Moses & Son is committed to providing our valued customers the most current information and data to empower your decision-making process. Discover our latest Australian wool market weekly update below, along with archived reports for your perusal and analysis.

2025-S13

What a difference a week makes!!

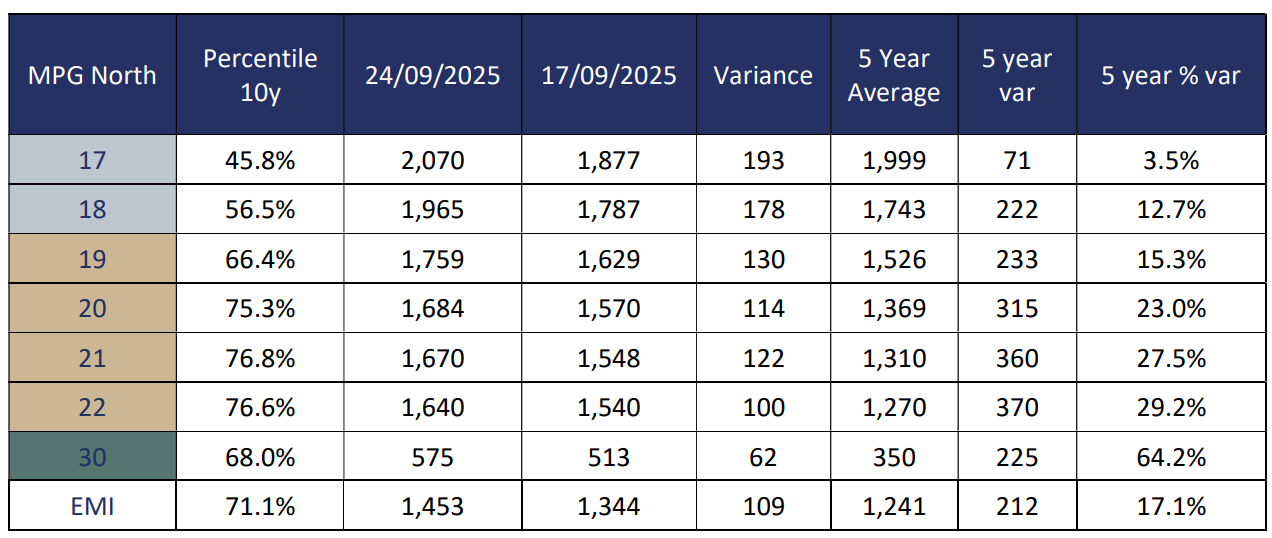

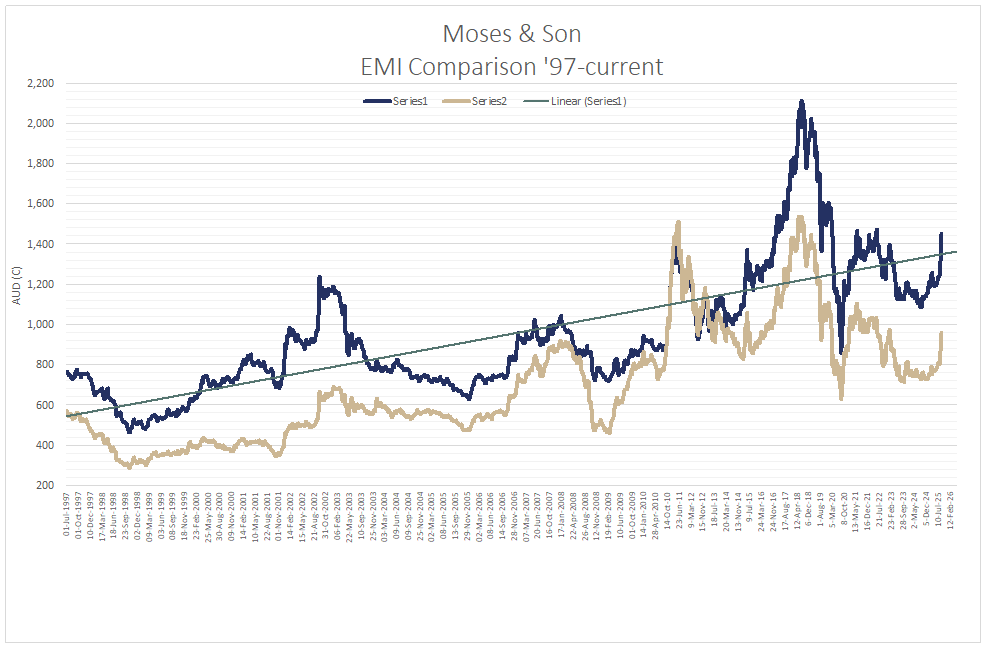

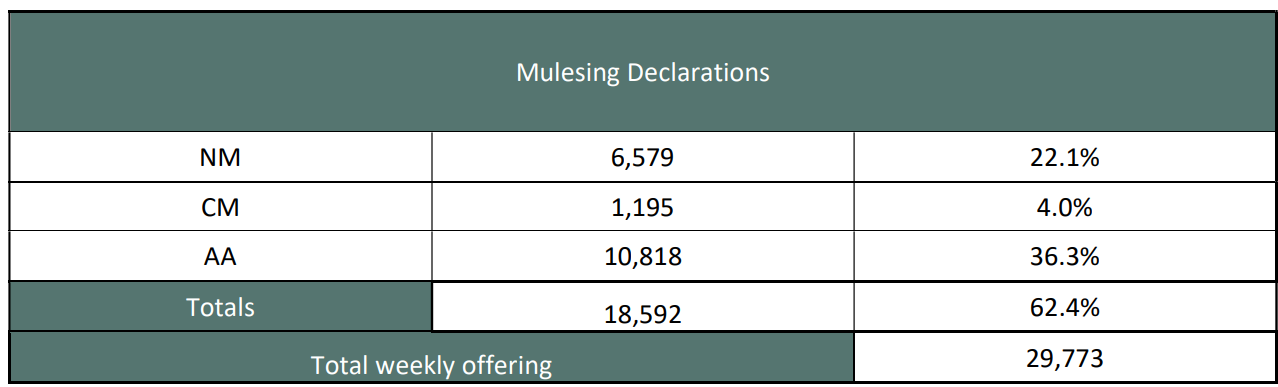

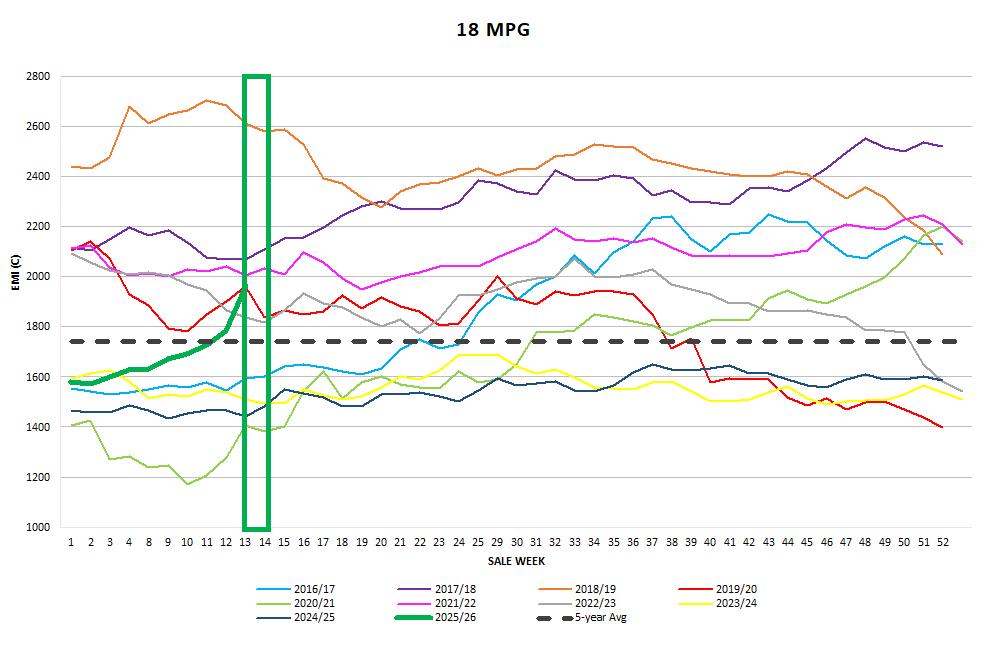

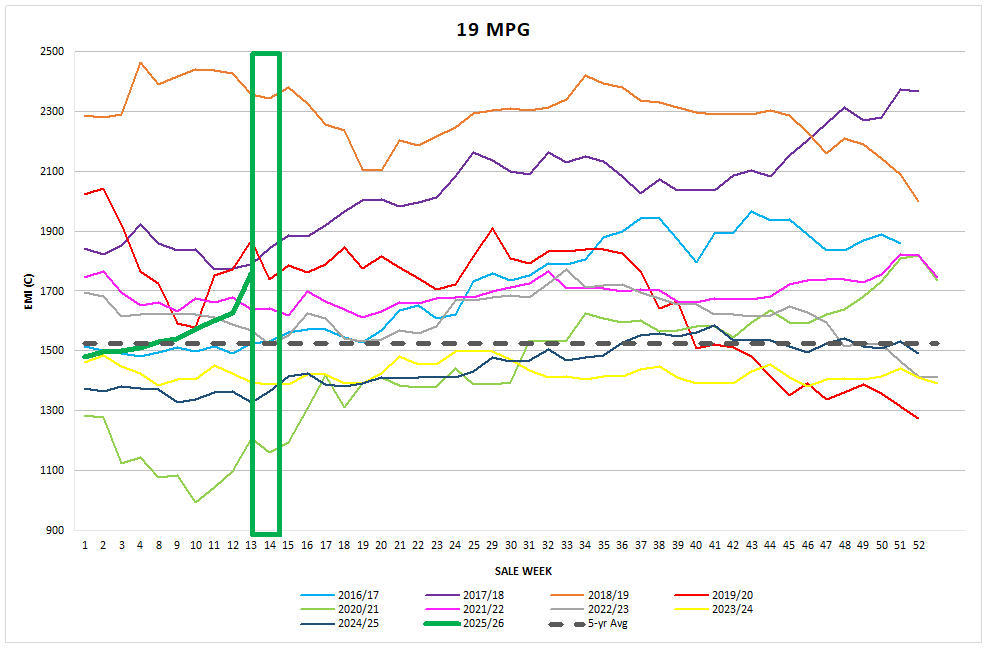

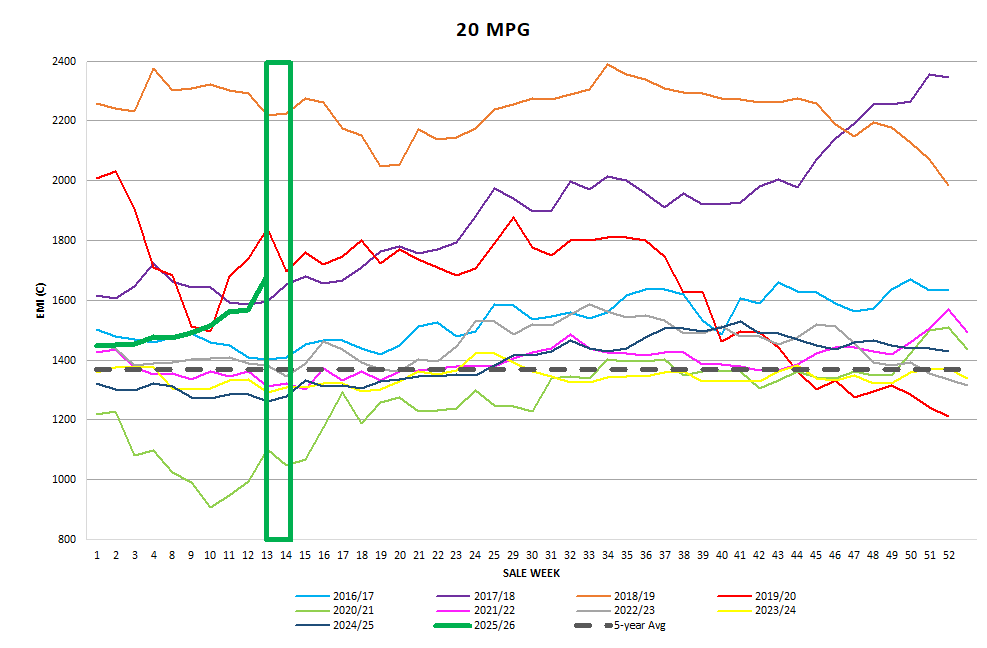

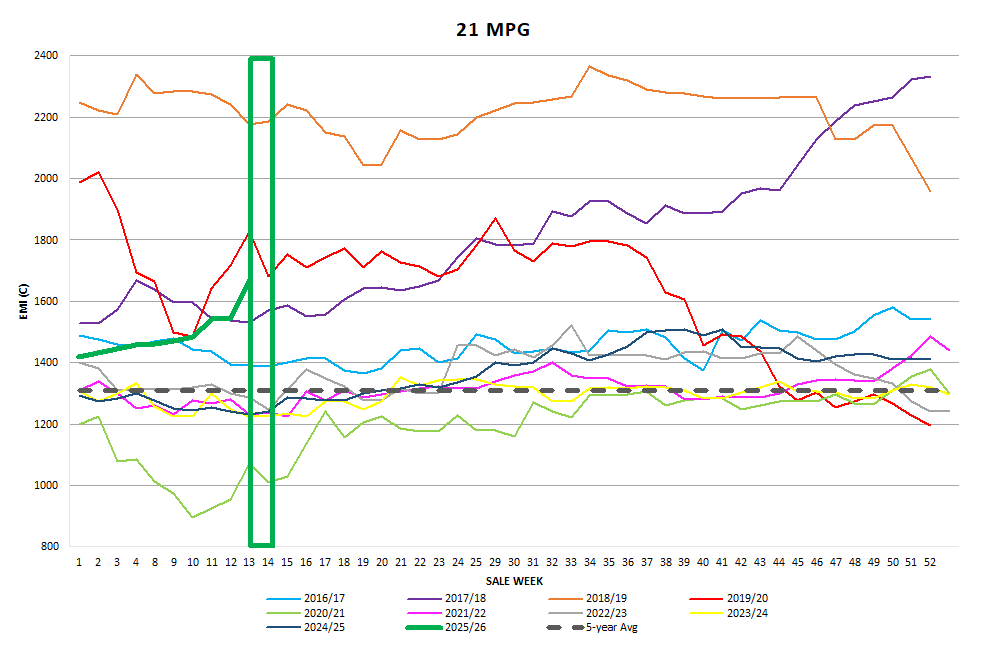

The AWEX EMI closed the week on 1453c, up 109c at auction sales in Australia this week. With just 29,773 bales offered, it was no surprise aclearance rate of 98.2% was achieved. This EMI rose 72c on Tuesday and 37c on Wednesday with the cumulative movement in the EMI being the largest weekly riseposted in six years (September 12, 2019). This week’s rise in the EMI extended the rally to 10 straight weeks, equaling the longest unbeaten weekly run since1987. Whilst Exporters came into the week buoyed by the outcome of the Nanjing Wool market conference. Reports from attendees felt that unlike the IWTO Congress in May 2025 Nanjing created more confidence than we have seen emerging from China since the US Tariffs on Chinese Goods entering the US were announced. It seems they are conquering the tariff dragon slowly but surely andhave a keen eye on the reduction in Wool production in Australia and other countries with similar production trends. The Australian representationannounced that after many years of resisting requests for a sale recess in the Chinese New Year week a conditional exception had been reached at the NationalAuction Committee meeting last week. This added to the positivity of the conference.

Merino Fleece

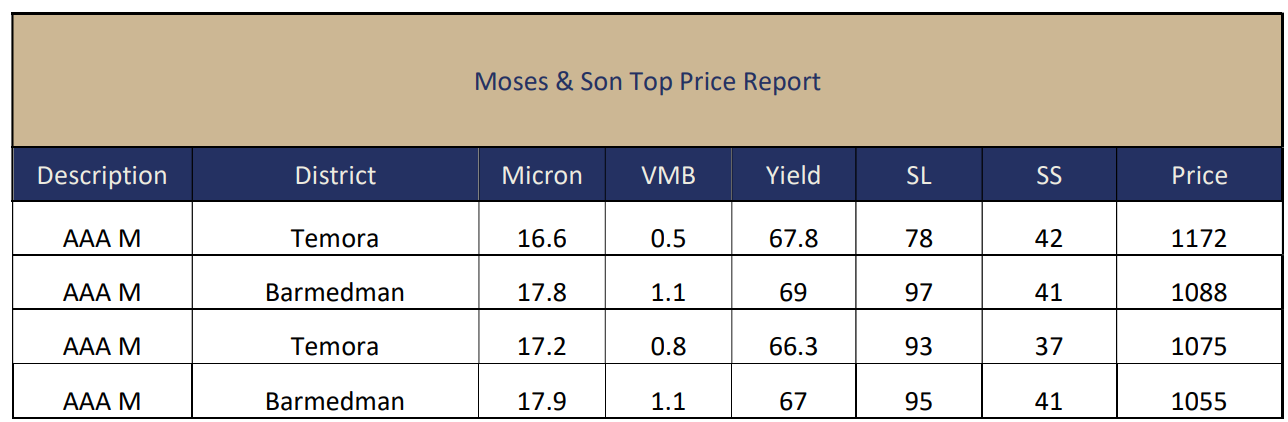

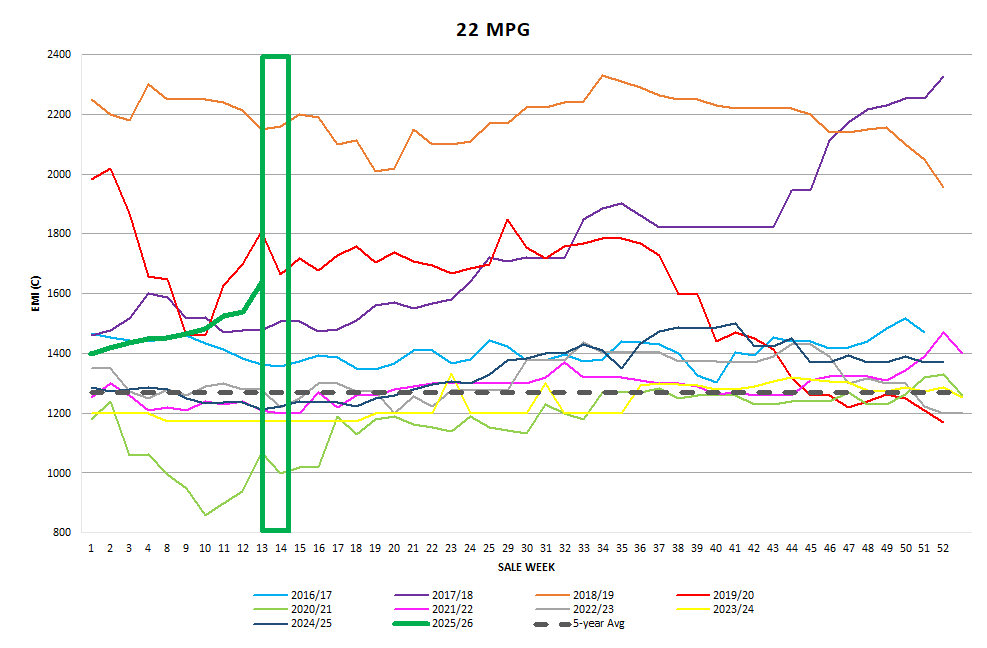

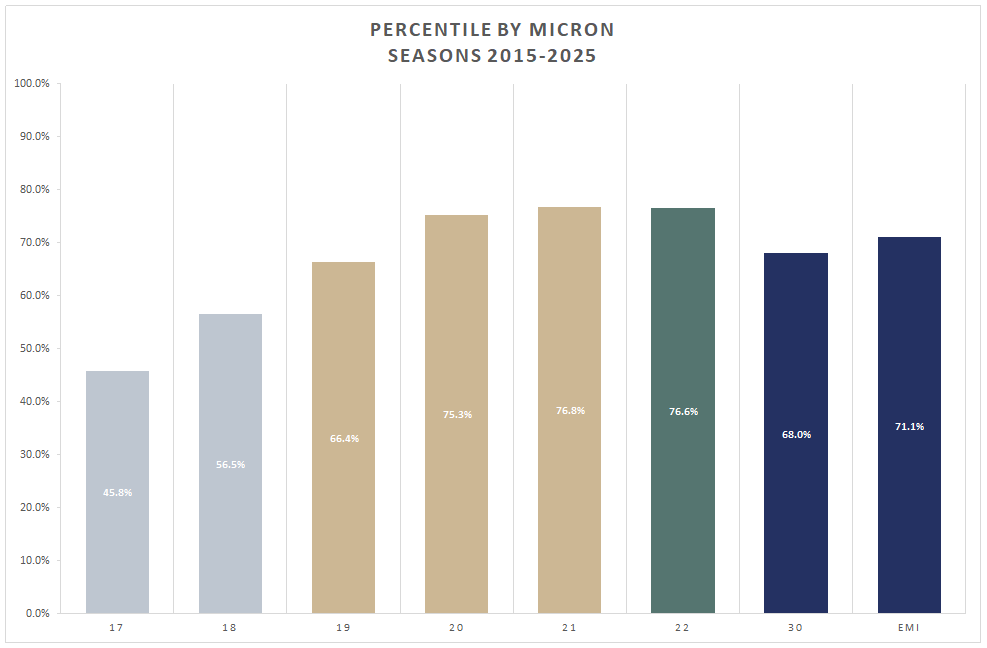

Started the week with buyer activity not seen for years. The weeklyrises in the merino MPG’s were generally divided into 18.5µand finer rising 169c-193c and 19µ and coarser roseby 114c-130c. The superfine sector made up valuable ground this week with 17MPG went up 193c to close on 2070c, its highest level since May 2023. Whilstthe fleece sector was dominated by Australia’s largest Export Trading entity,Chinese indent operators were driving the market on every lot. Whilst the 17MPG hit the 56th5-year percentile the 21 MPG topped the 5-yearpercentile.

Merino Skirtings

Saw similar rises to the fleece with average rises of 100c measured onthe low VM skirtings Tuesday and another 50c added on Wednesday. Heavier VM Skirtings added 50-60 on Tuesday and another 20c on Wednesday. Whilst the top two Australian Trading Exports dominated the purchases in this sector, competition from Indents and the largest Chinese Topmaker was quieter than normal in the fleece sector, purchasing 11% of the skirtings.

Merino Cardings

Were the exception to the market rise this week.

Crossbred Fleece

Crossbred Oddments

Crossbreds

Followed the Merino fleece and skirtings lead adding 47-78c across the MPG range. Competition came from a mixture of all exporter and processor sectors scrambling to secure quantities pushing the 28and 30 MPG’s to the 100th Percentiles.

Next Week

Next week’s offering increases to 35,260 bales and the early sentiment is that there has been enough business done, to carry into next week at similar levels to this week. ~ Marty Moses.

Graphs

Market Commentary

What drove the market to rise 8% in a week seems to be the 64M$ question, and to date it seems the only explanation is the persistent message of lower wool production projected for Australia coupled with lower-than-normal inventory levels with the early-stage processors and further up the manufacturing pipeline. The string of historically low weekly volumes on offer, coupled with the draw down from wool being held in brokers inventory in Australia. Compared to our competing fibre prices (cotton, viscose, polyester staple and acrylic) have not experienced the comparative price rise seen in wool (Source ICS).

The recently concluded Nanjing Wool Market conference was widely believed to be the most positive and best opportunities for business since 2018.

Key factors driving the positivemomentum this week include:

· Lower than normal inventory (stock) isbeing held by a majority of first stage and a portion of the second stage andbeyond makers and processors. Greasy wool stocks from all origins are athistorical low levels and most mills were looking to renewal.

· Demand has lifted, more volume of woolproducts are moving through the supply chain and more swiftly allowing forturnovers to improve. Much of this new business is made up of blends mostly tomeet price points as retail recovers and uniform business starts to buildagain.

· Some of the medium-size Chinese millshad relied upon a local single entity for supply that has now changed andappear to have adjusted their business model. Those mills are now using forwardcontracts written directly from the overseas traders, creating morecompetition.

· Demand from Europe now relies partly onChina produced tops or yarns. Many mills in China now compete for that higherquality, potentially more lucrative business. The dominant supply for thatconsumer and manufacturing market relies upon certification of RWS/NM to becarried through to the exported product from China to Europe. Demand ispredicted to keep rising for that product supply chain and calls to increasesupply of RWS/NM was placed in front of all wool producing nations.

· Australian traders had/have very littlestock left to sell so they must be aggressive in auction to meet the higherdemand and predicted business opportunities going forward into what was beingwidely tipped as a sustainable bull run in the short term. Source (AWI Weekly Market report)