2025/26 Season Review & 2026/27 Outlook

Australian sheep and wool prices strengthened sharply through 2025/26 as tight supply met improving market sentiment. Wool production fell as flock numbers remained historically low and seasonal conditions constrained rebuilding, while strong lamb and mutton values encouraged producers to retain or carefully manage breeding stock rather than rapidly expand numbers. At the same time, the wool market benefited from firmer buyer demand, particularly from China, renewed interest in sustainable natural fibres, and premiums for finer microns and whilst both the price premium and the volume certified has shrunk, the demand for certified wool continues to grow. This combination of constrained supply, stronger sheep meat pricing and improved confidence across the wool pipeline helped drive a marked lift in both sheep and wool values over the season.

Production Summary

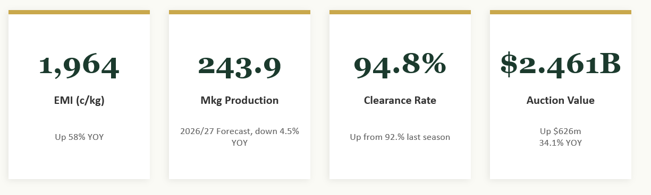

The 2025/26 Australian wool season was defined by significant supply tightness. The Australian Wool Production Forecasting Committee (AWPFC) fourth forecast for shorn wool production stood at approximately 255.4 Mkg greasy (down 8.8% year-on-year from 2024/25), with some earlier estimates around 244.7 Mkg reflecting even sharper declines. The first forecast for the 2026/27 season resulted in a fall of 4.5% to 243.9 Mkg indicating a likely 23% fall in wool production over the past 4 seasons.

Key drivers of the production decline include multi-year seasonal pressures on stock numbers, historically low flock levels—with the national flock near historic lows at around 70 million head—and subsequent destocking driven by strong mutton and lamb prices, high shearing costs, and broader industry shifts.

Declines occurred across all states, with New South Wales forecasted at 98.6 Mkg greasy (down ~10.4%). This structural tightness, combined with low auction volumes, supported strong price performance throughout much of the season.

Price Performance

The Eastern Market Indicator (EMI) showed remarkable resilience and gains, breaking through the 1,700c/kg clean mark early in 2026 and reaching highs of 1,964c/kg by early June 2026 levels not seen since 2019 and representing substantial year-on-year increases at 64.8%. Merino wool led the gains, with premiums for certified and finer microns. Clearance rates remained solid despite smaller rosters, reflecting buyer competition amid constrained supply.

Global Economy & Demand

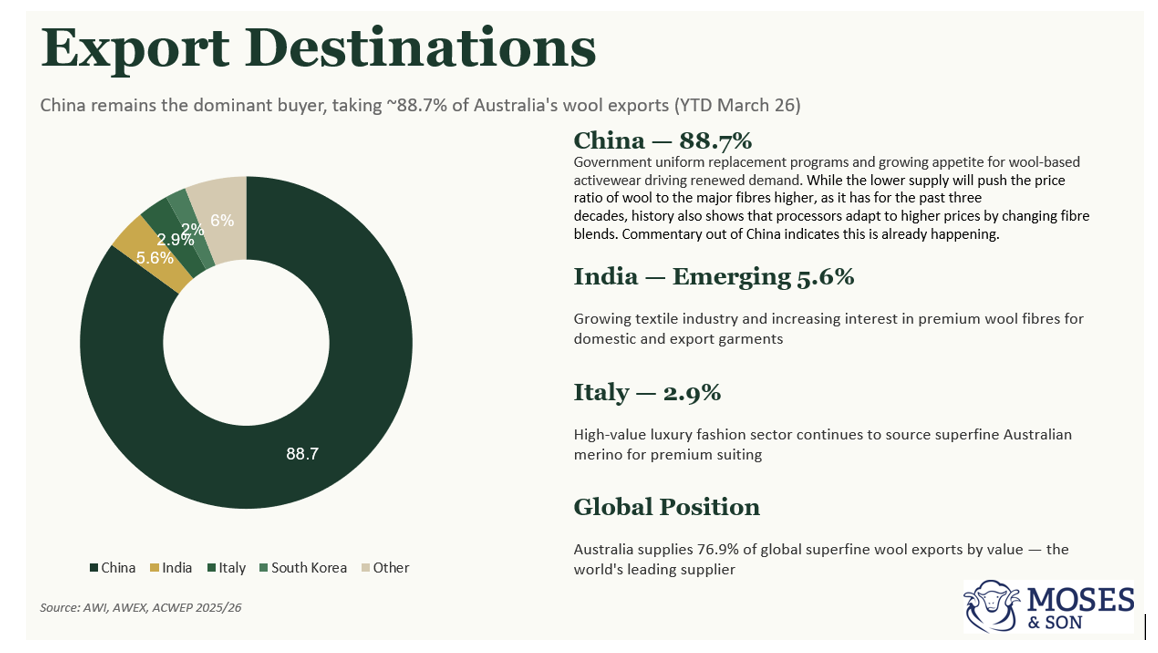

Global economic conditions in 2025/26 were steady but divergent, with overall GDP growth projected around 3.3%. China, the dominant processor and buyer of Australian wool (handling over 40% of global raw wool, and more importantly, 89% of the Australian Wool Exports), provided robust demand support despite its own challenges.

Key demand supports:

• Renewed interest in sustainable natural fibres.

• Strength in luxury and performance apparel sectors.

• Broader recovery in textile demand.

Demand from key markets remained firm, helping offset any softness elsewhere. Global wool market value continued to expand, driven by sustainability trends and wool's unique properties.

Geopolitical Impact

Geopolitical eventssignificantly shaped the operating environment:

· Middle East tensions, including 2026Iran-related conflict and risks to the Strait of Hormuz, lifted oil, fuel, and fertiliser prices, increasing on-farm and logistics costs.

· Shipping disruptions and elevated energy costsadded inflationary pressure across the agricultural supply chain, although theworst impacts were partially contained.

· The ongoing Russia-Ukraine conflict continued to contribute to global energy and commodity volatility, within direct flow-on effects for the wool sector.

Despite these headwinds, tight wool supply and strong buyer demand (particularly from China) enabled the market to absorb cost pressures and deliver firm-to-strong prices. Wool's resilience stood out amid broader ag sector challenges.

Outlook for 2026/27

The AWPFC's first forecast for 2026/27 shorn wool production is 243.9 Mkg greasy, another decline of ~4.5% from 2025/26, pointing to continued supply constraints.

Positive factors:

- Sustained demand from China and global textile sectors.

- Premiums for certified wool, including AWSS and ResponsiWOOL.

- Wool’s continued position in sustainable fashion.

Challenges:

- Persistent cost pressures linked to geopolitics and farm inputs.

- Slow flock rebuilding across key production regions.

- Potential economic softening in major export markets.

ABARES and industry views suggest wool prices should maintain recent strength into 2026/27, supporting values even as overall sheep meat/wool production value eases modestly. The season is expected to remain a “seller's market” for quality clips, with opportunities for producers leveraging their income from wool with certification schemes and efficient operations. An informed market is a healthy market.

In summary, the 2025/26 season highlighted the Australian wool industry's resilience: low supply drove strong prices despite geopolitical and cost challenges, underpinned by solid global demand. With further production declines forecast, the outlook for 2026/27 remains cautiously optimistic for well-positioned businesses.