Market Intelligence

Weekly Wool Market Commentary

Moses & Son is committed to providing our valued customers the most current information and data to empower your decision-making process. Discover our latest Australian wool market weekly update below, along with archived reports for your perusal and analysis.

2025-S23

The EMI closed at 1521c, up 17c at auction sales in Australia this week, posting a 6c rise on Tuesday and a further 11c on Wednesday as we fast approach the final wool sales of 2025. From the offering of 35,335 bales, which managed to reach 95% of the early estimates published last Wednesday—the total clearance rate was 94.9%. The best-performing sector was Merino Skirtings, averaging a 98% clearance across all centres. With the AUD showing signs of strengthening over the selling week, the EMI in USD terms closed at 1001c, up 21 USC for the week and edging toward the September USD EMI bar set at 1032c. Crossbreds appeared irregular as we enter their main receival period.

Merino Fleece

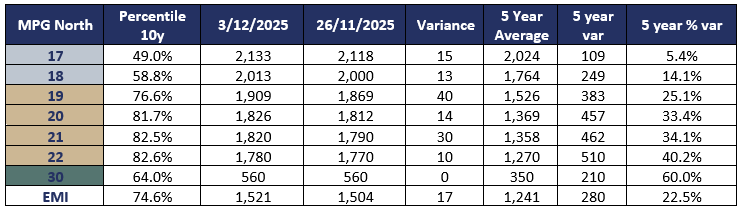

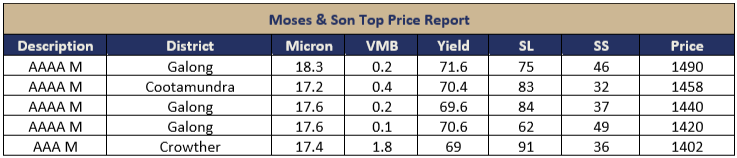

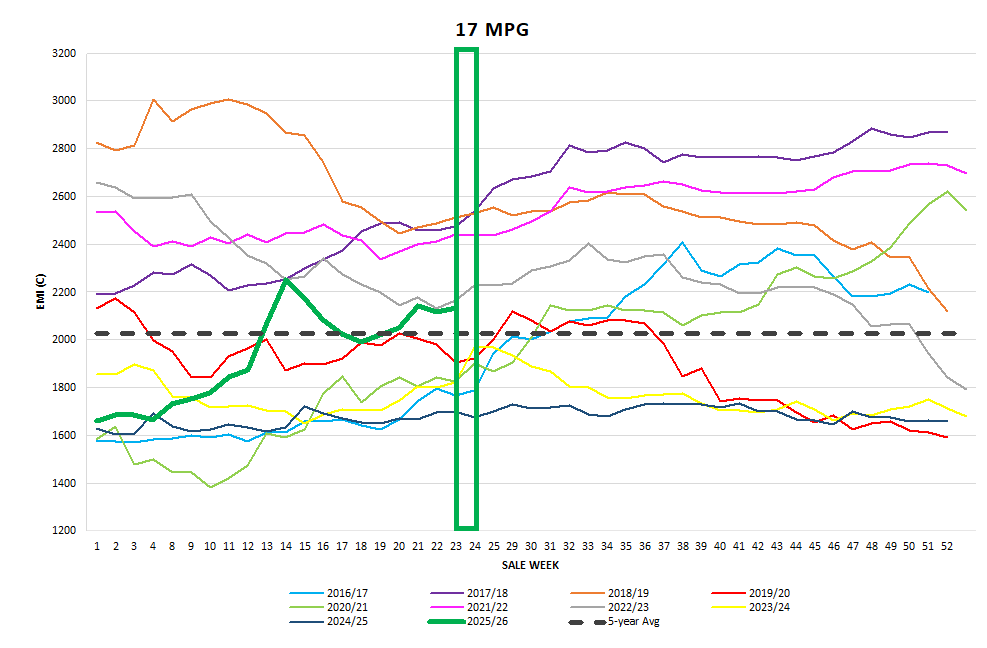

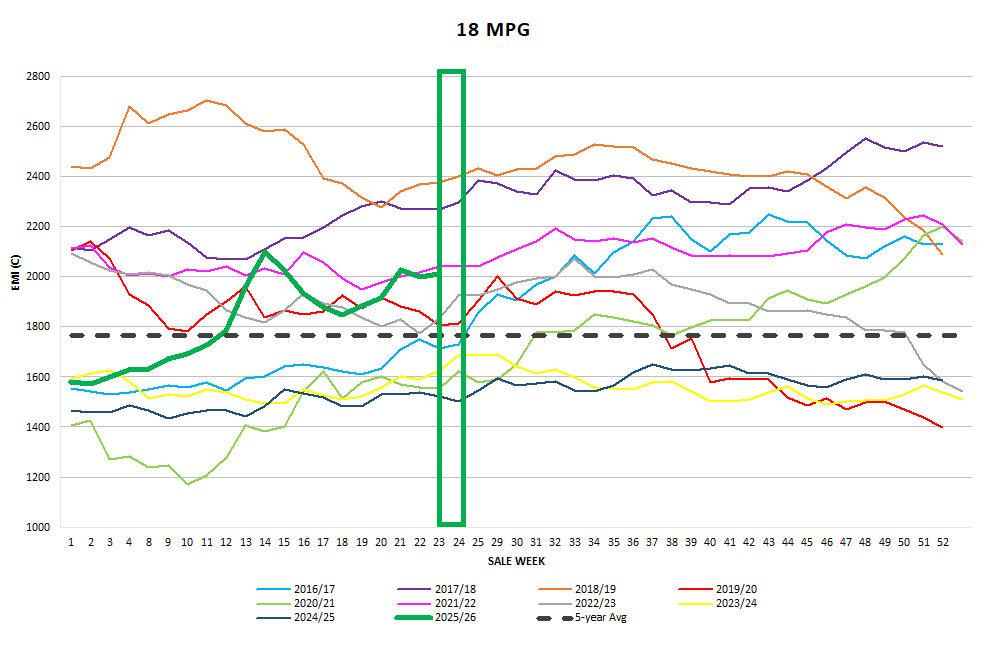

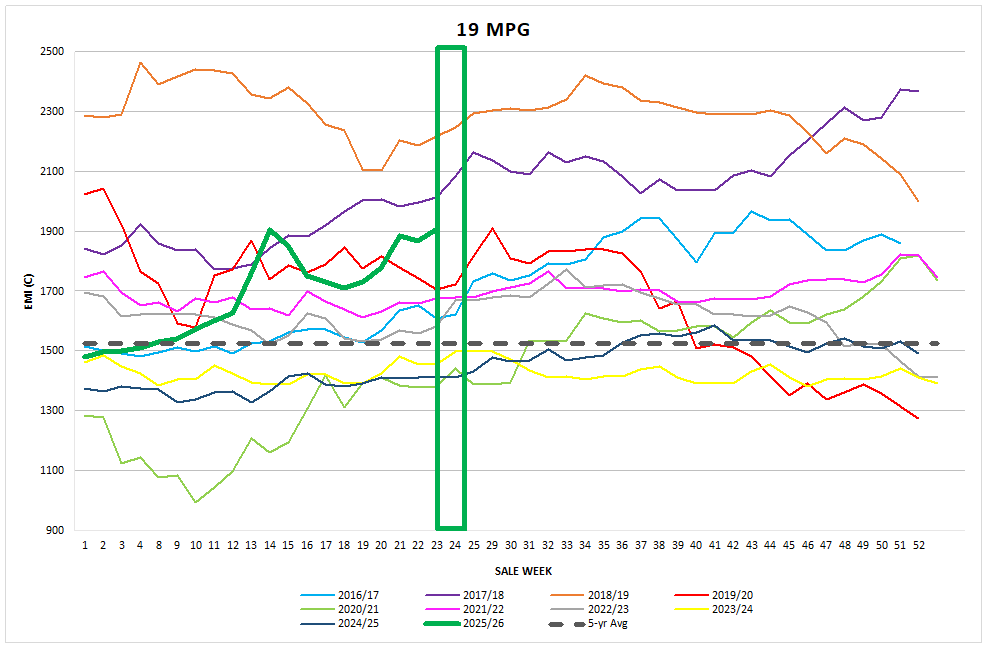

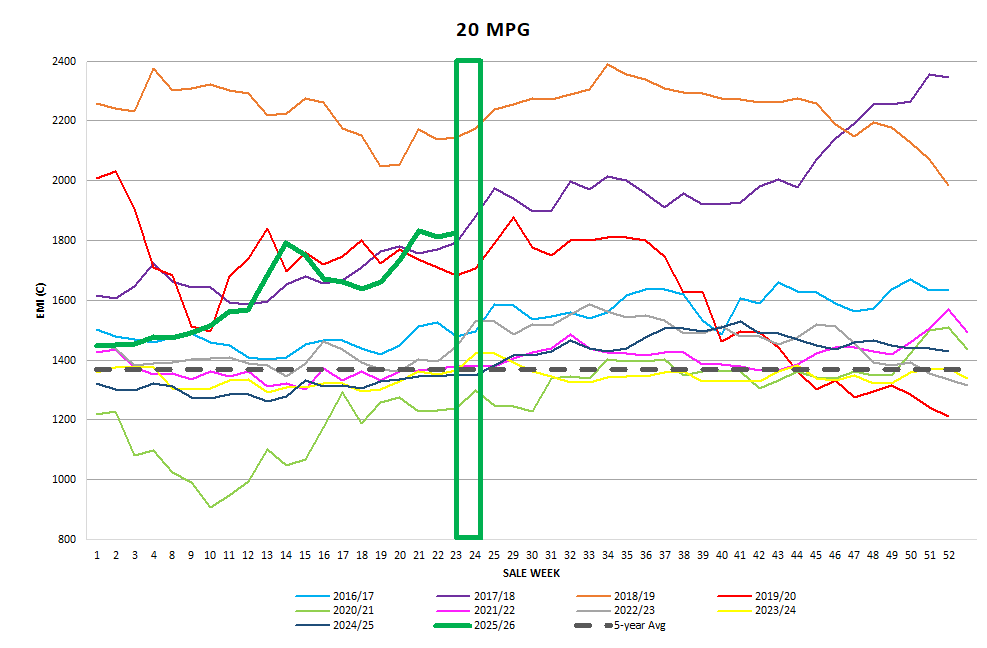

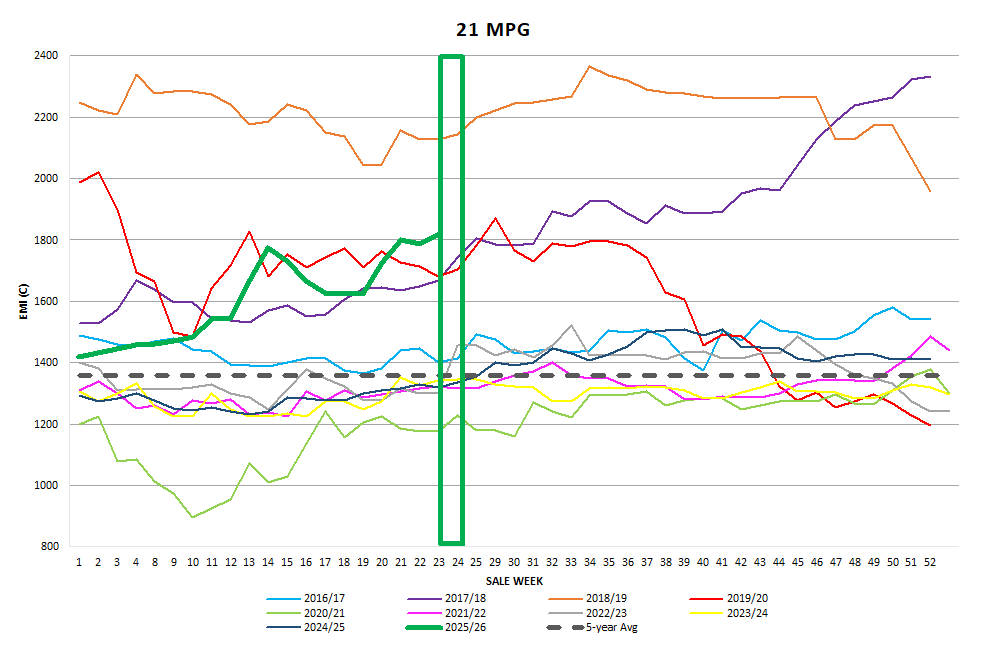

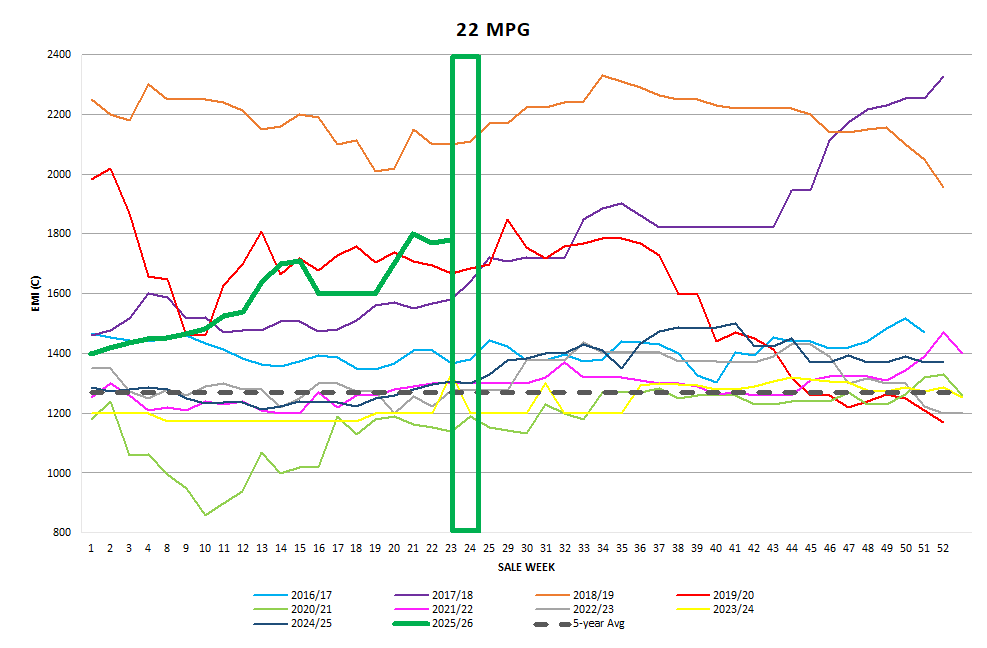

Sydney markets opened facing last week’s bullish results from the gazetted Superfine Sale selection. The momentum was well supported not only in the best-style and best-specified lots, but also across a wide range of styles and specifications, all of which saw solid price increases. Competition from the European (Italian) sector was more noticeable, and the scope of their buying targets was somewhat wider than we have seen in the past. The really exciting news is that the 19µ, 20µ, and 21µ MPGs have surpassed the September rises. Competition was clearly dominated by the largest Australian-based trading export companies, leaving the indent operators chasing the upward price trend in both Merino fleece and skirtings.

Merino Skirtings

Skirtings opened strongly, with last week’s levels immediately surpassed and most types finishing dearer for the day. Wednesday’s sale continued the positive performance, accelerating right through to the final lot offered.

Merino Cardings

Merino Cardings have been a warm topic over the past week, with some of the strongest inquiry seen in a year or two beginning to emerge. While the MC indicator has not yet shown significant price movement, it appears some exporter carding inventory is currently being drawn down, suggesting there maybe a pleasant surprise either side of Christmas.

Crossbred Fleece

Crossbred Oddments

Crossbreds

Crossbreds opened the week strongly, with prices remaining fully firm. We have been reporting the importance of the Coefficient of Fibre Diameter (CVD) in XB fleece selection variance, and Wednesday was a classic example: lots with high CVD were substantially discounted, resulting in negative movements in several Crossbred MPGs.

Next Week

Next week will be the penultimate sale for 2025, and sellers in every centre have mustered 41,383 bales nationally. Three weeks ago, I would have said that any week offering above 40,000 bales would crush market momentum. However, pressure will now be on early-stage processors, traders, and indent operators to manage purchase shipping and deliveries to keep mills operating over the Christmas break and into early 2026.

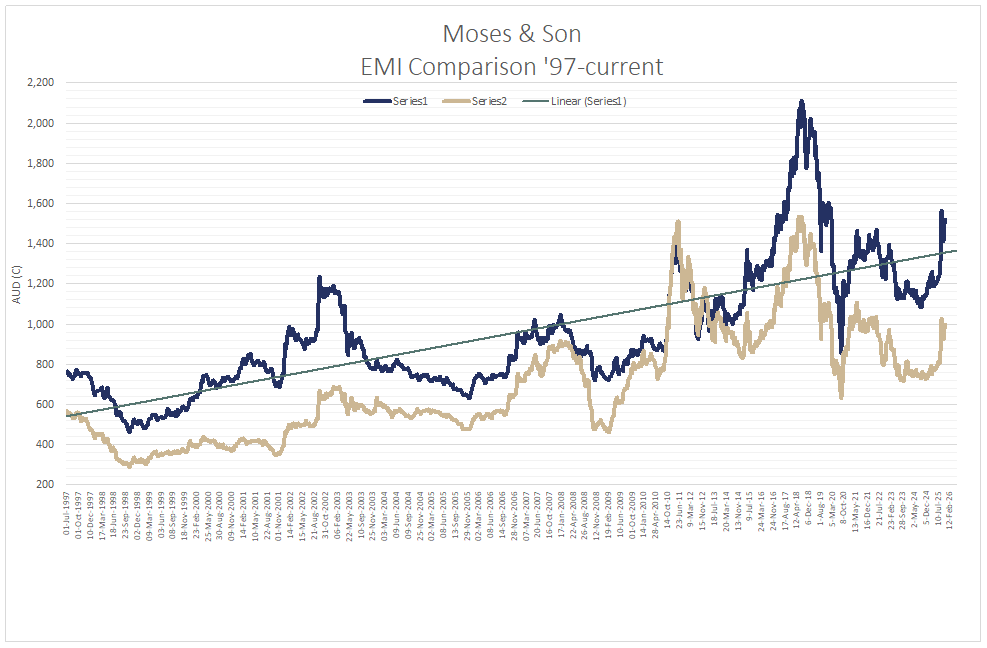

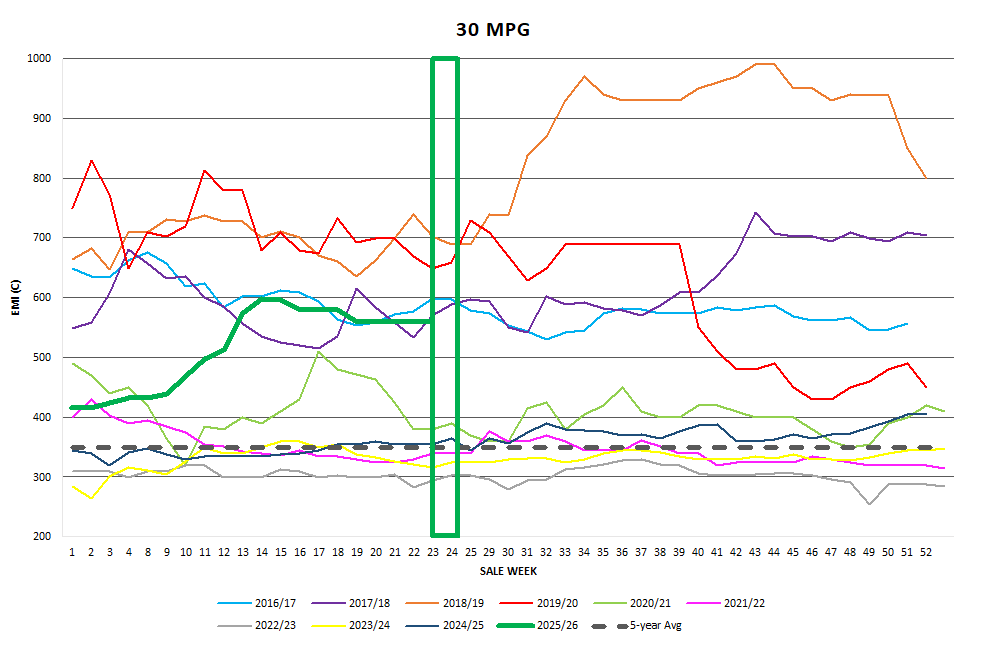

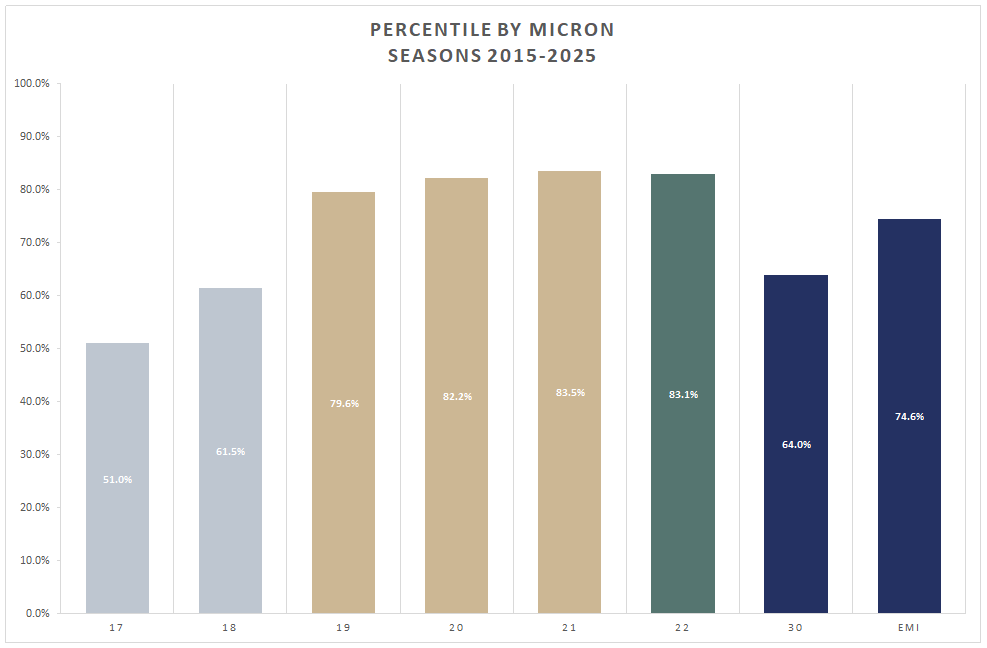

Graphs

Market Commentary

AWTA released its November key test data, showing November bales sampled were down 14.5%, with year-to-date bales sampled down 10.4%. With the Production Forecasting Committee meeting in the next few weeks, the auction results show that while bales offered are only down 4% YTD, bales delivered from previous seasons are up 20%. This places the true YTD offered at auction figure at approximately -9%.

A sincere acknowledgement to the amazing RFS units for their incredible efforts in the Temora Shire last Friday, where a fire broke out south west of Temora. More than 30 district Rural Fire Service units and the local town brigade responded, working alongside three aerial fire fighting units to bring the blaze under control. It was a super-human coordination of resources. We are aware of a number of locals directly impacted by the fire, but thankfully there appears to have been no significant personal harm to those involved.