Market Intelligence

Weekly Wool Market Commentary

Moses & Son is committed to providing our valued customers the most current information and data to empower your decision-making process. Discover our latest Australian wool market weekly update below, along with archived reports for your perusal and analysis.

2025-S18

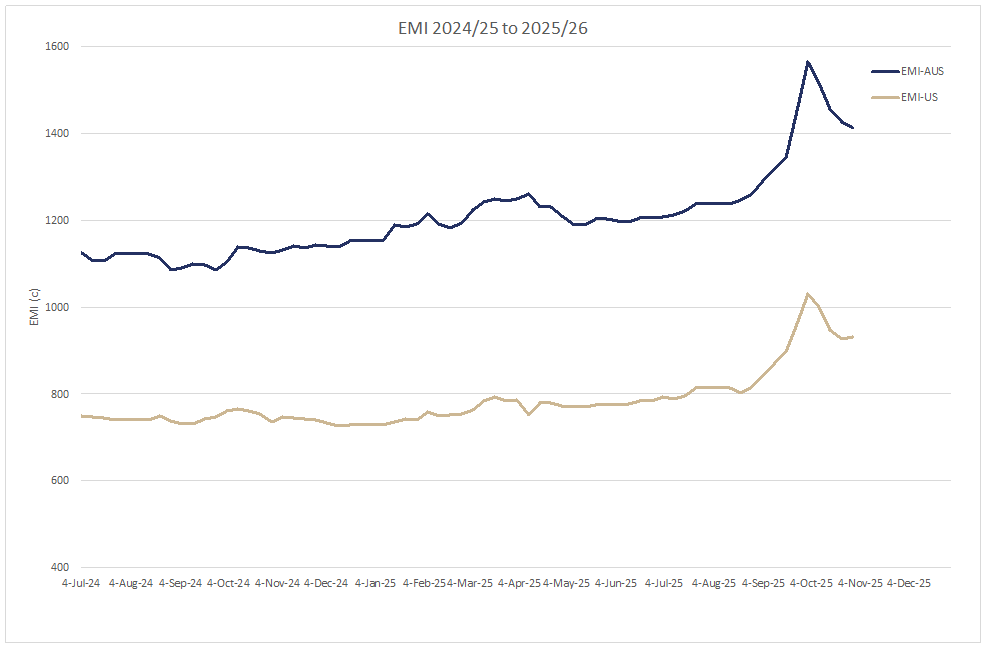

The AWEX EMI closed on 1413c, down 14c at auction sales in Australia this week. 33,535 bales went under the hammer in all selling centres in Australia this week, with a clearance rate of 87.9%. The AUD increased from .65c to .66c which resulted in the EMI in US terms adding 5c for the week and possibly indicating a steadying price basis for now. With a 12.1% pass in rate and 8.6% withdrawn before sale sellers exercised their right to refuse the prices on offer, and In this period of diminishing wool supply, this sent a clear signal of price resistance to the market.

Merino Fleece

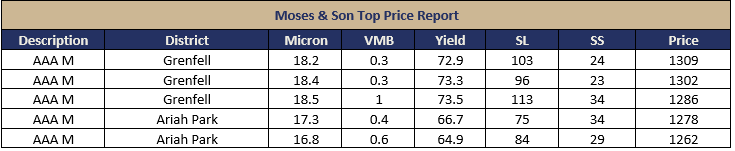

The merino fleece continued to progressively give back the price gains achieved over the July to September period. While there were some signs of positive price support in the well-measured and specified super fine categories throughout the week, cumulative price falls were measured across all Northern MPG’s, ranging from 6c to 42c. The Southern region MPG’s ranged from +6con the coarser Merino MPG’s to -27c at the finer end. Competition from traders, indents, and processors remained cautious, and notably, the largest Australian trader was unusually out of the top four fleece buyers in this category this week. Whilst there has been some commentary about the market finding a new trading level, it was difficult to find a positive signal in AUD terms. Perhaps next week, if the AUD/USD relationship moderates, we may see the market stabilise.

Merino Skirtings

While Tuesday opened in buyers’ favour, Wednesday’s skirting prices fell another 10–20c. Buyer competition came from trading exporters, China’s largest top maker, and Chinese indents.

Merino Cardings

All centres posted price falls in the MC category. Sydney was off -5c, Melbourne -11c, and Fremantle -20c. There are frequent reports emerging that these wools continue to be hard to sell down the pipeline.

Crossbred Fleece

With the largest falls (-43c) measured in the 26 MPG, crossbreds were generally cheaper across the 25–30µ MPG’s. Despite this weaker price trend, Melbourne posted a 3c rise in the 28 MPG.

Crossbred Oddments

Crossbreds

Next Week

Next week, the national offering is estimated at 34,598 bales. Due to “the race that stops the nation” on Tuesday, sale days will shift to a Wednesday–Thursday series in all centres ~Marty Moses

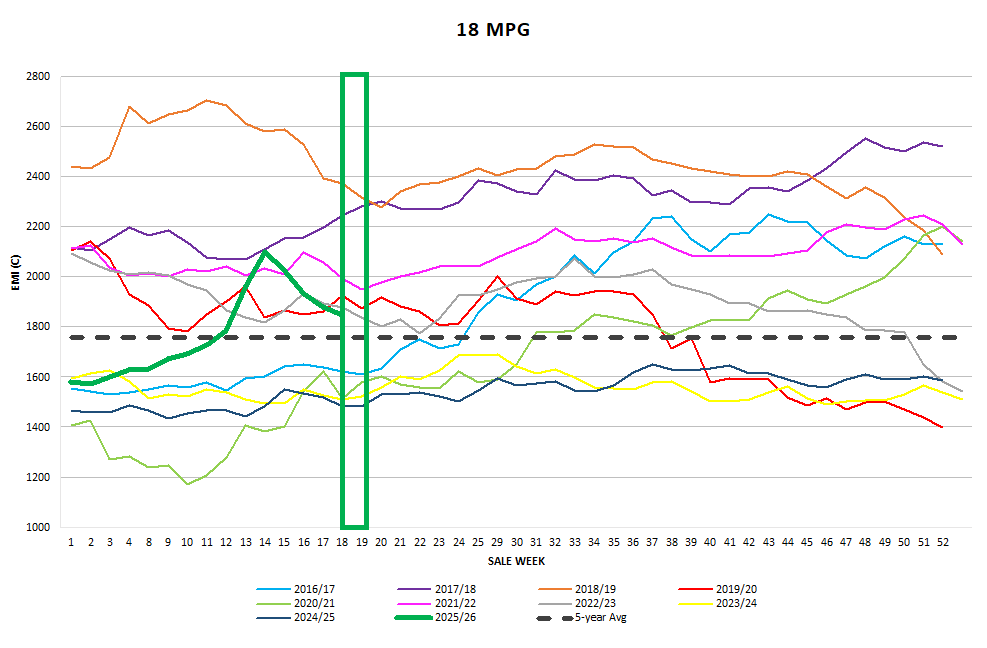

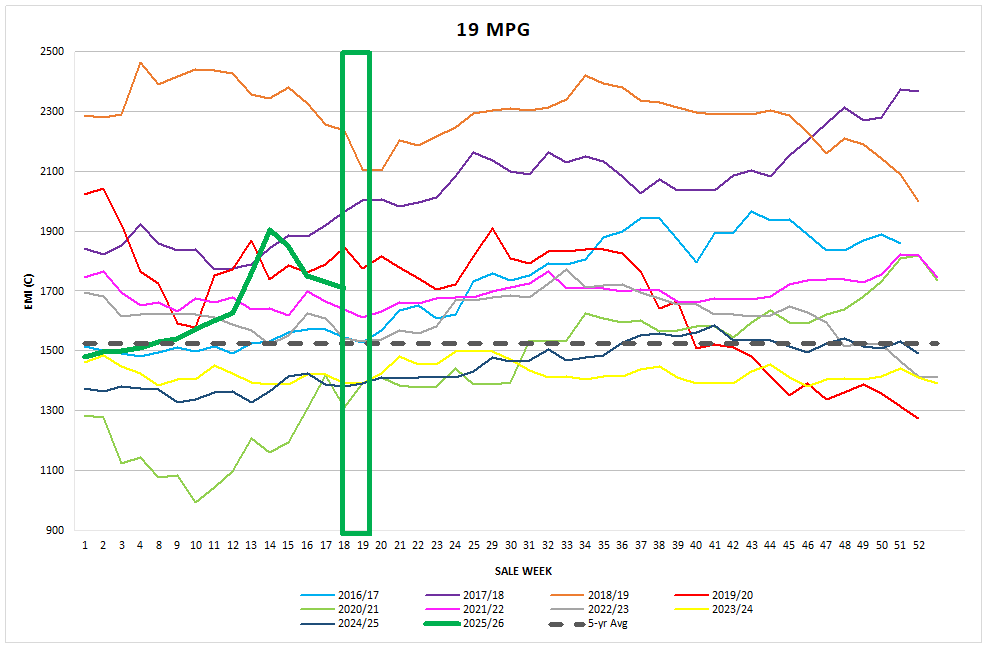

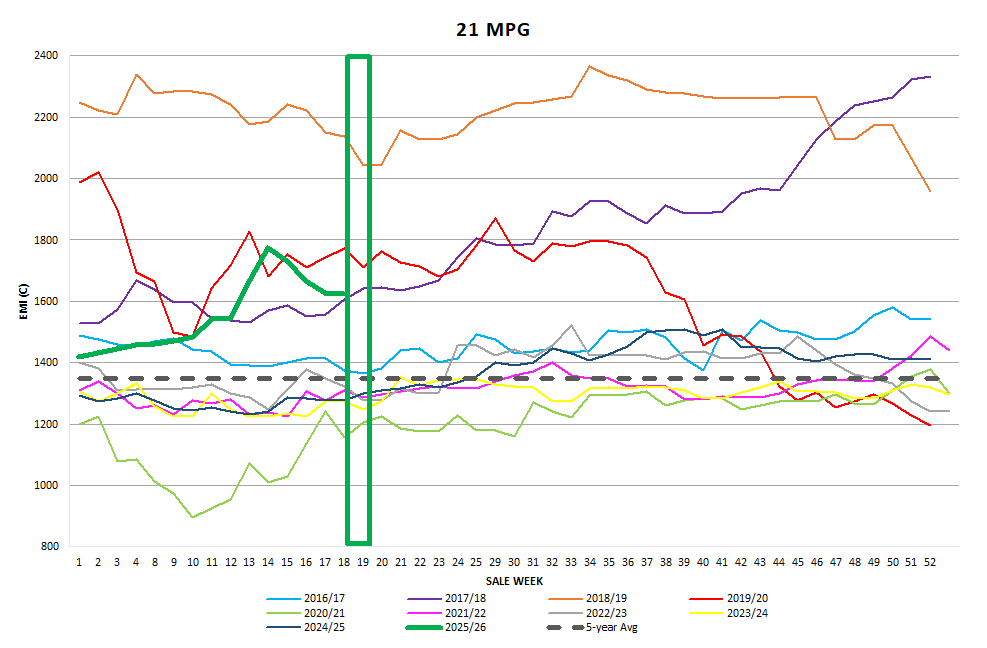

Graphs

Market Commentary

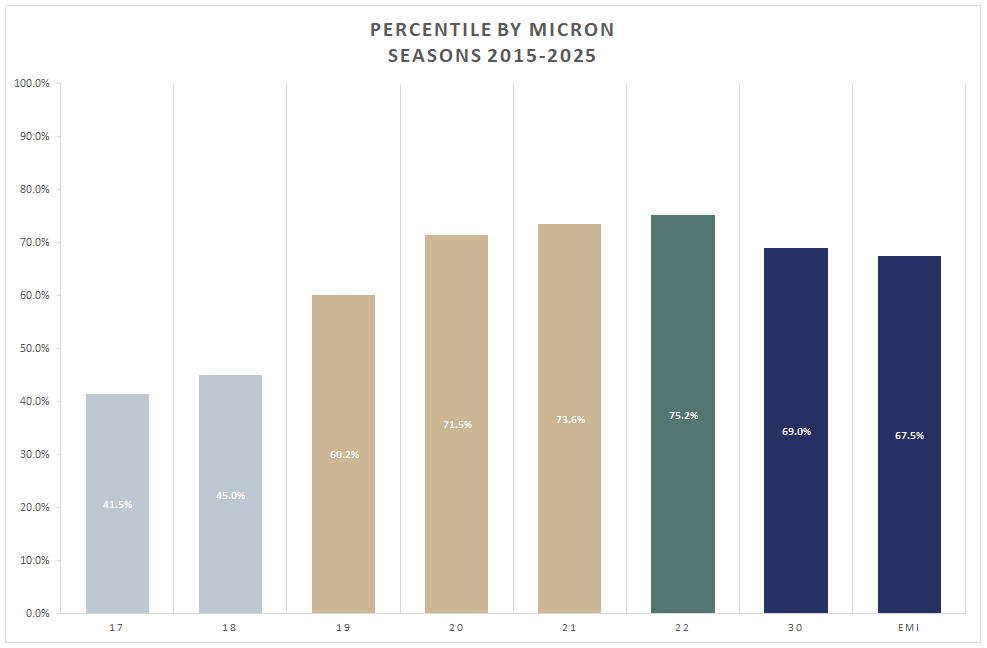

There is a reduction in the quantity of medium and coarse Merinos, reflected in the price levels sitting at the 90–98percentile price bands for the 19 and 21 MPG’s. In the superfine and ultra fine sector, unless wools meet best spinner specifications, there is little or no interest in paying a price premium due to the abundance of bales available in this category. Whilst seasonal conditions have varied widely, we are now seeing the impact in the wool being catalogued. There is no shortage of over length, tender, high midpoint break, low style, and poor-yielding combing wool on offer, with this proportion of the selection fast becoming the “norm” for now.

Market intel reveals that competing fibre prices remain static due to slow sales persisting in Northern Hemisphere retail outlets. Until retail demand improves for all fine fibres, prices are expected to remain under pressure.

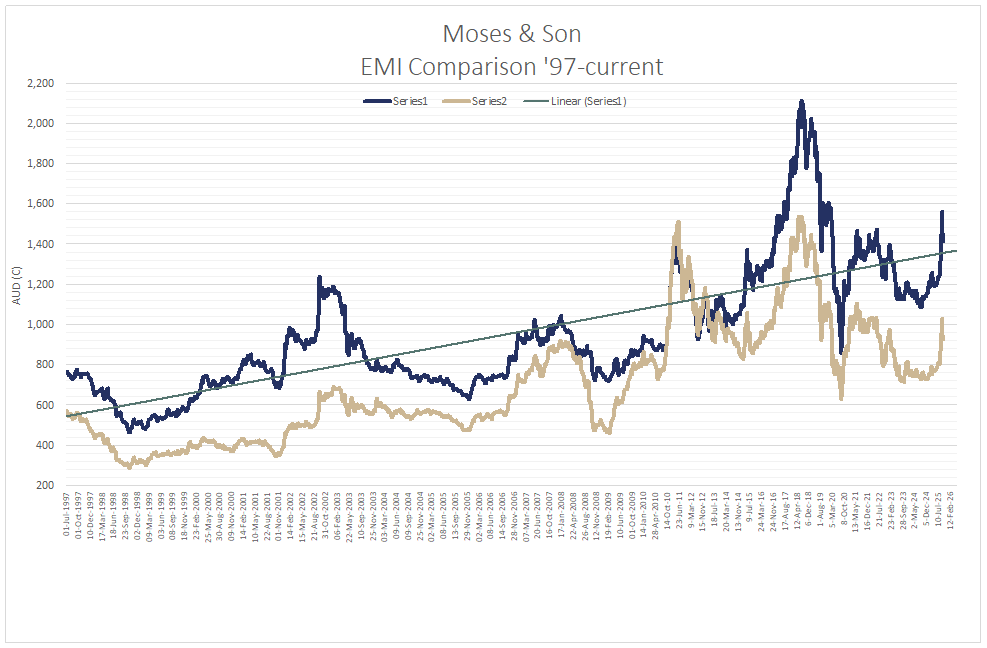

Despite October’s inability to post a rise in the EMI, the statistics for this fiscal year remain quite impressive for wool overall. Since 1st July 2025, the EMI posted rises for 11 consecutive weeks, reaching 1565c (up 358c) before falling over the past four weeks, giving back 152c of those previous gains. Compared to the same time last year, the EMI remains 288c higher (+25.6% YOY).