Market Intelligence

Weekly Wool Market Commentary

Moses & Son is committed to providing our valued customers the most current information and data to empower your decision-making process. Discover our latest Australian wool market weekly update below, along with archived reports for your perusal and analysis.

2025-S24

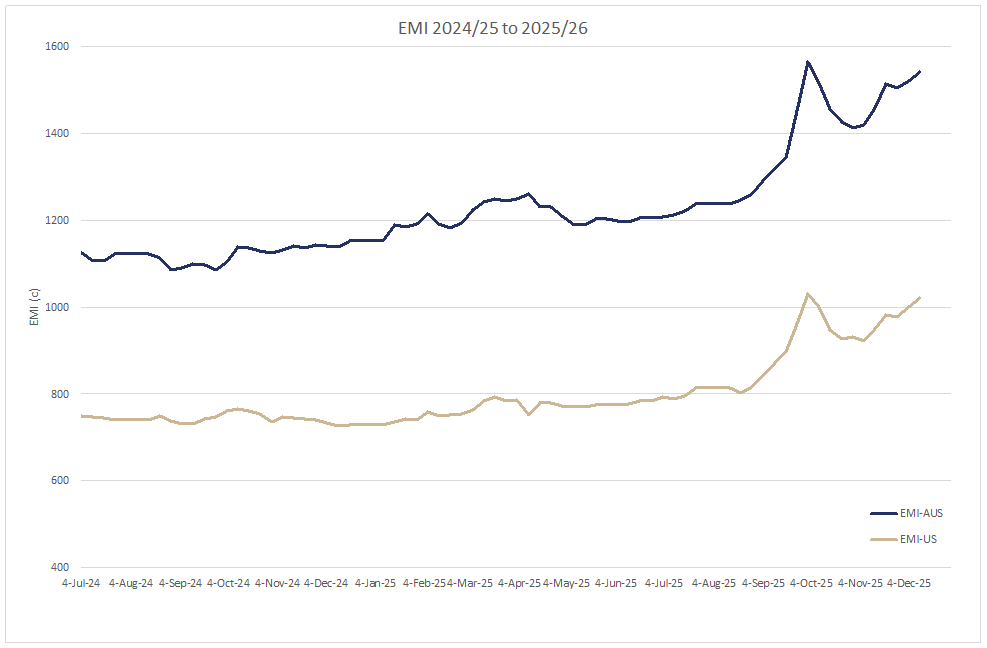

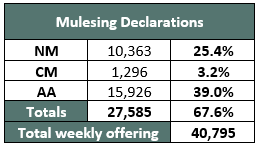

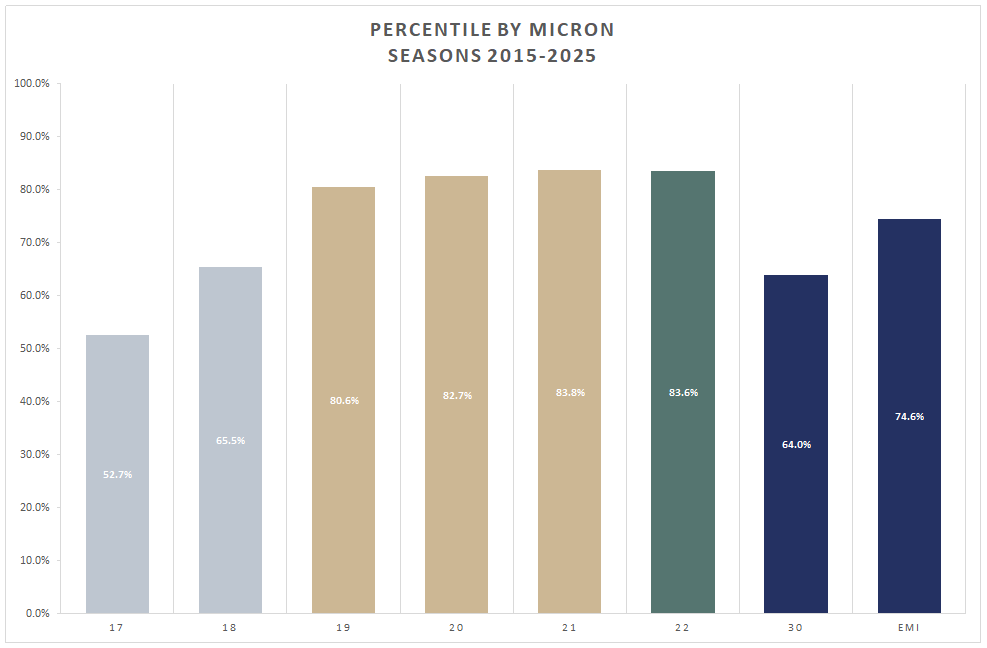

The AWEX EMI closed at 1542c, up 21c at auction sales in Australia this week. The market defied the challenge of 40,795 bales on offer and an appreciating AUD/USD exchange rate, delivering a 94.2% clearance. In USD terms the EMI rose 23c to close at 1023 usc. The significance of this week’s EMI levels in both AUD and USD is notable given the muddy demand signals filtering through from brands at retail.

The EMI in both currencies has clawed its way back to within 1% of the September peak. This week signalled the penultimate sale before the Christmas recess, and the best Christmas present for woolgrowers would be the EMI finishing 2025 on a high.

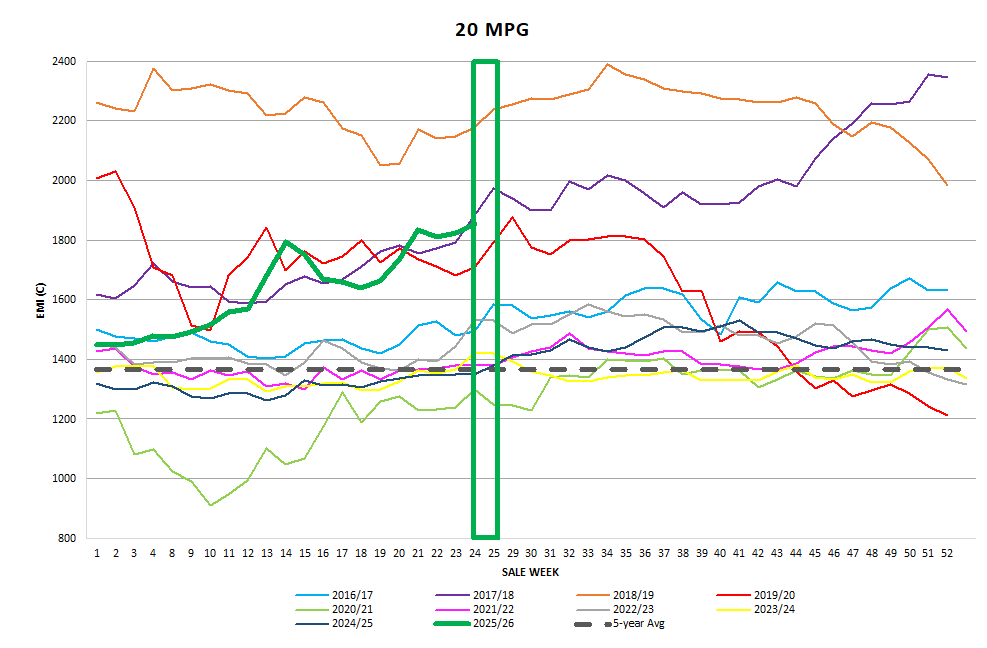

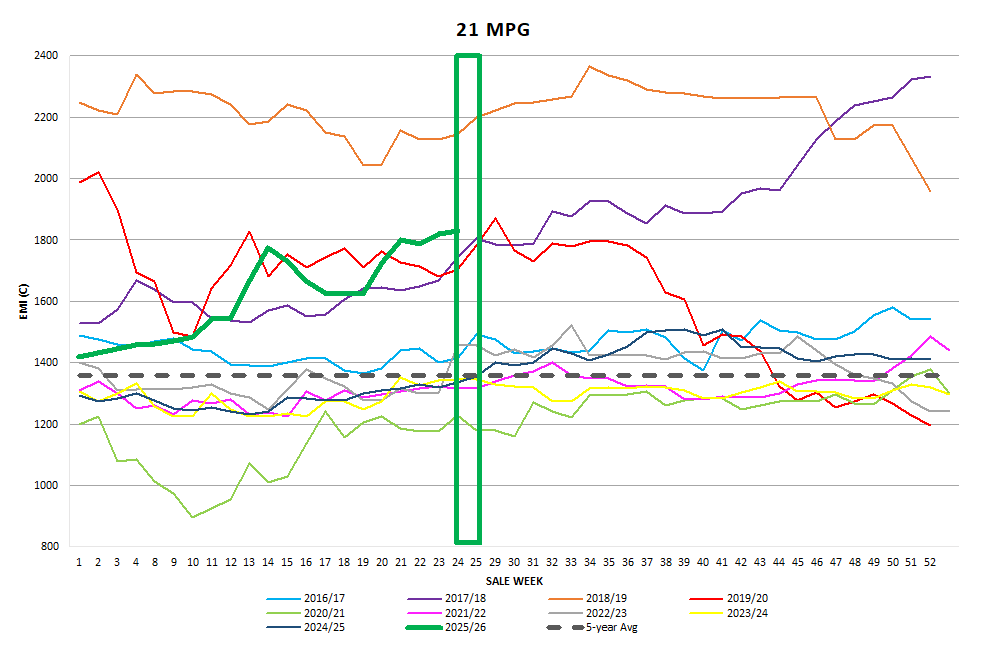

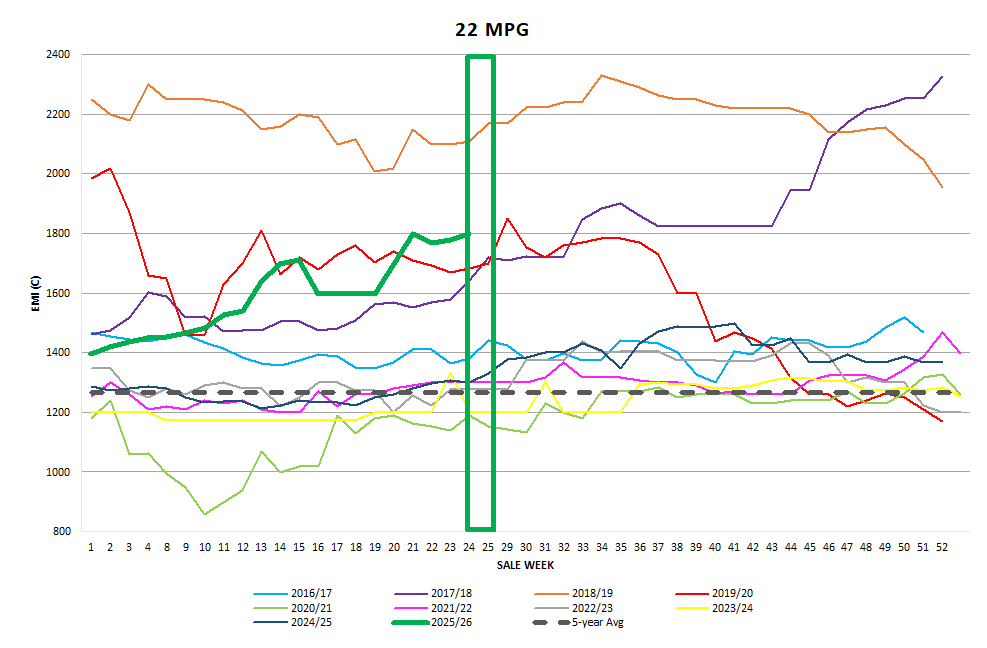

Merino Fleece

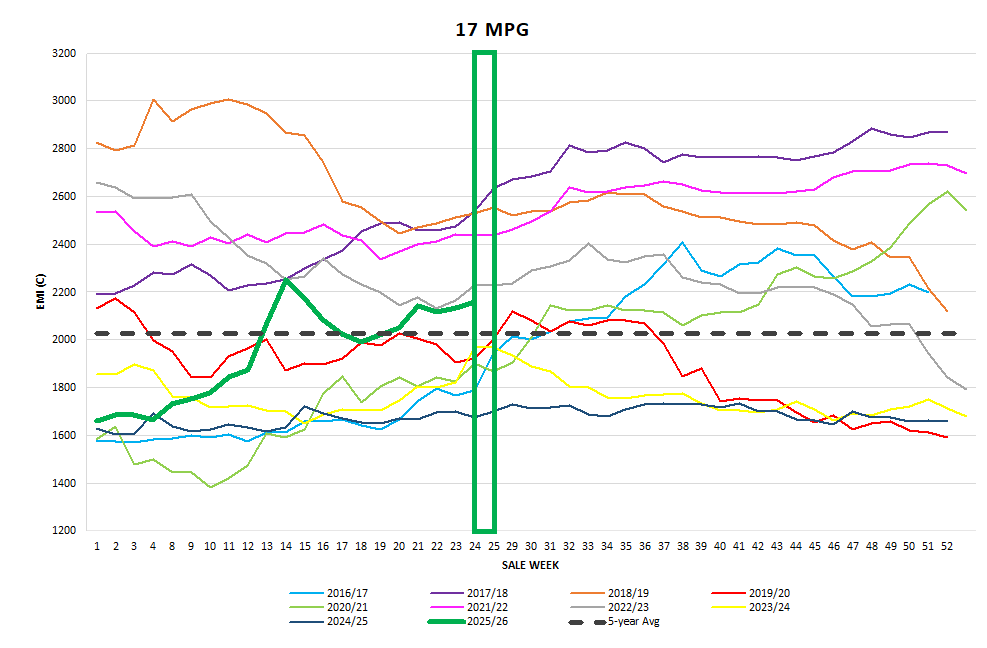

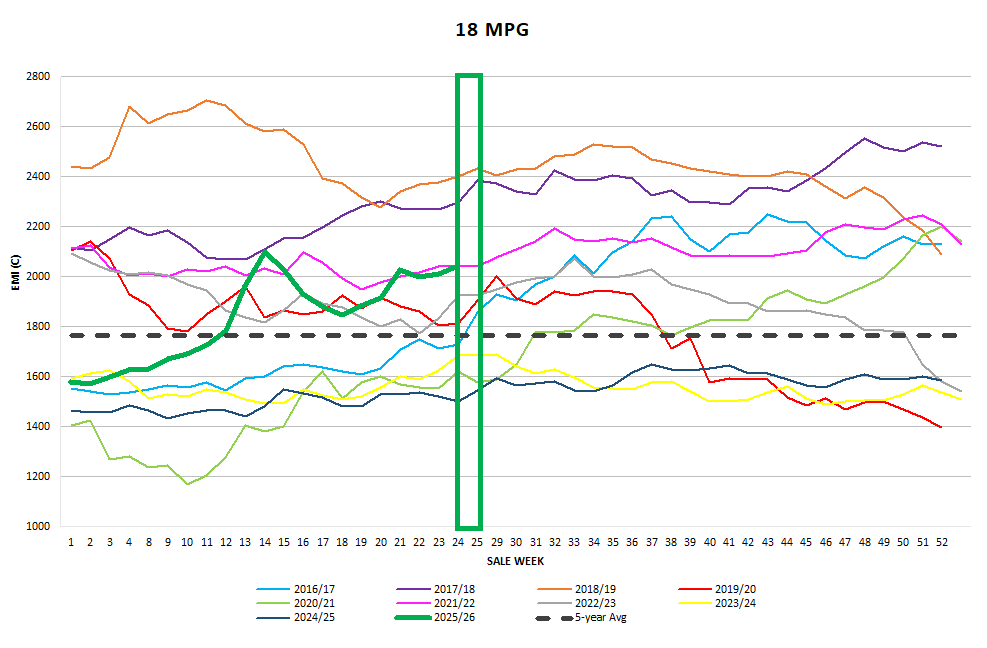

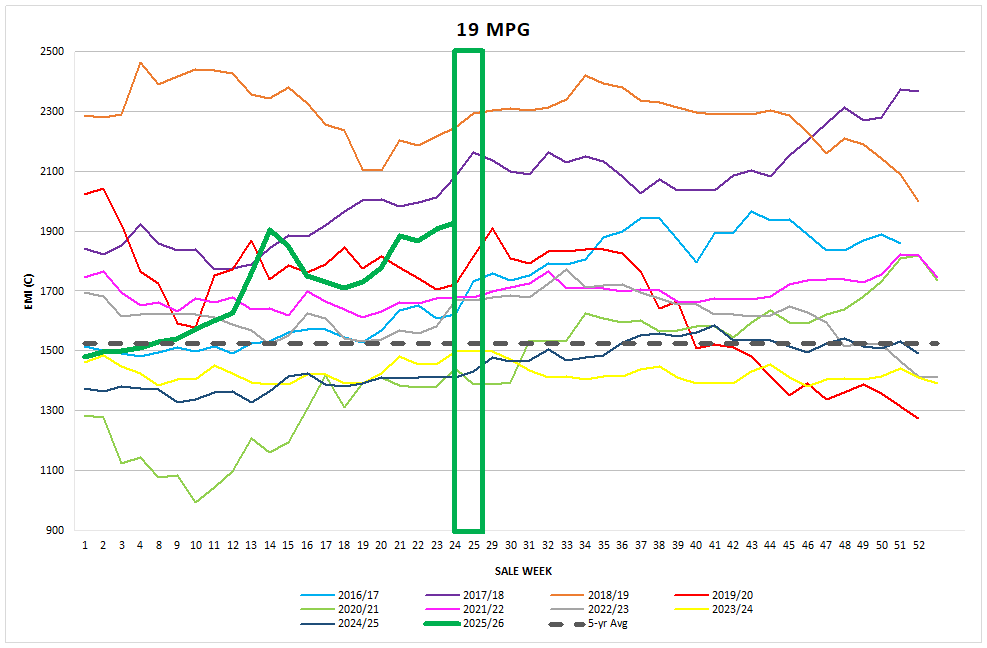

In the northern markets, the indices rose 9–39c across the Merino MPGs on Tuesday. Despite Wednesday’s slight pullback in the 16.5–17.0µ Superfine indices, the fine and medium MPGs added a further 5–25c to Tuesday’s gains. Support remained strong from the largest Australian trading export companies, Chinese indent operators and large Chinese top makers, with the top four buyers securing over 61% of the fleece offering.

Merino Skirtings

Merino skirtings with less than 3% VM strengthened immediately on opening, with all other types holding firm. Wednesday saw all skirtings, regardless of VM%, increase by 10–20c, again driven by strong competition from the largest Australian trading export companies. The top four buyers accounted for 57% of the offering.

Merino Cardings

Merino cardings continued to maintain or slightly increase their levels across the week. Fremantle was the standout, adding 35c, supported by solid rises in lambs and crutchings over both days.

Moses & Son’s top price for Merino Crutchings this week was 1131c greasy (1737c clean), just shy of the top eastern-seaboard price for bulky, clean, well-picked crutchings from a mulesed with pain relief ewe flock.

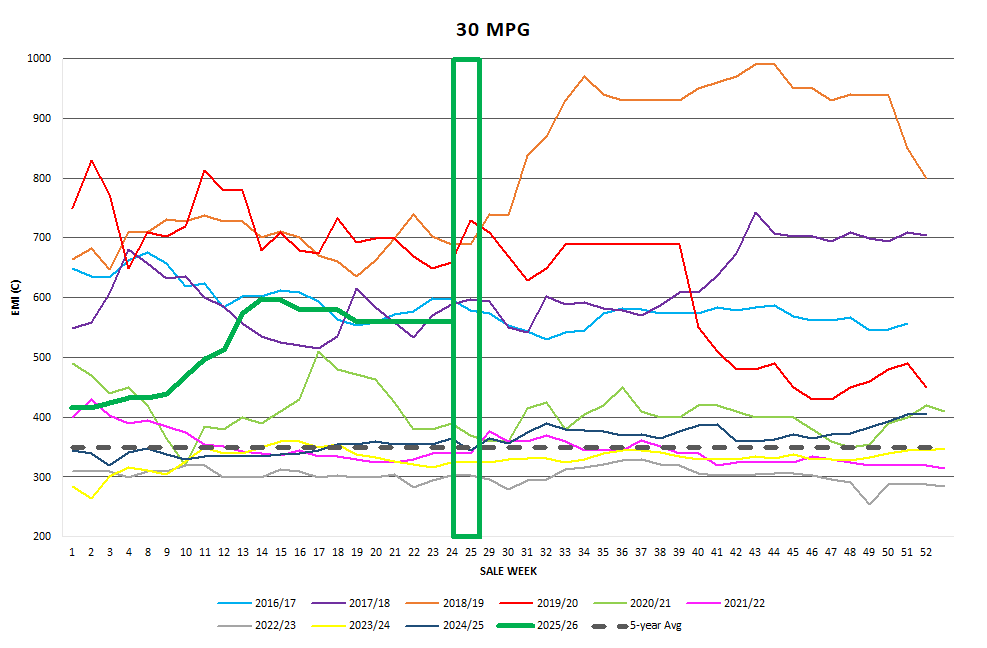

Crossbred Fleece

Crossbred Oddments

Crossbreds

Tuesday’s opening in the northern region featured a stylish and well-prepared crossbred combing catalogue, attracting increased competition and driving prices in the 26–30µ MPGs up 10–25c. Although the 26µ MPG failed to maintain its previous day’s premium, the 27µ and broader MPGs held firm. The largest Australian trading export companies dominated this sector, with additional support from a European processor.

Next Week

Next week the market will offer 40,509 bales nationally, almost identical to this week. The early market intel indicates that significant market movement appears unlikely. Under performing global economic fundamentals have thwarted any significant improvement in demand for woollen garments at retail, however supply continues its downward trajectory. Historically low sheep numbers and the impact on wool production and will place more pressure on the early-stage processing inventory security, meaning exporters should feel some elevated demand over the next few months.

The December round of State Wool Production Forecasting Committees commenced this week, with the National Production Forecast Committee preparing to release its third estimate for the 2025/26 season before Christmas (though it will not be published until after next week’s market closes). While most people will be focused on the Christmas tree over the next 13 days, my attention will be on the downstream market reaction to the WPFC’s third forecast for Australian wool production. ~Marty Moses

Graphs

Market Commentary

The EMI is now 402c (35.3%) higher than the same week last season. In USD terms the EMI sits at 1023 usc, 296c (40.6%) above the same time last year. In AUD terms, the stronger market has pushed total wool sales above $1 billion ($1,033 million),up a cool $152 million on the same point last season. Season to date offerings are 4.3% lower (with an elevated number of older-season bales included), while AWTA testing volumes are down 14.4% in November and running 10.4% lower in season-to-date. South Australia remains the worst-affected state, down 15.4% after enduring some of the harshest drought conditions of the past 12 months.