Market Intelligence

Weekly Wool Market Commentary

Moses & Son is committed to providing our valued customers the most current information and data to empower your decision-making process. Discover our latest Australian wool market weekly update below, along with archived reports for your perusal and analysis.

2025-S31

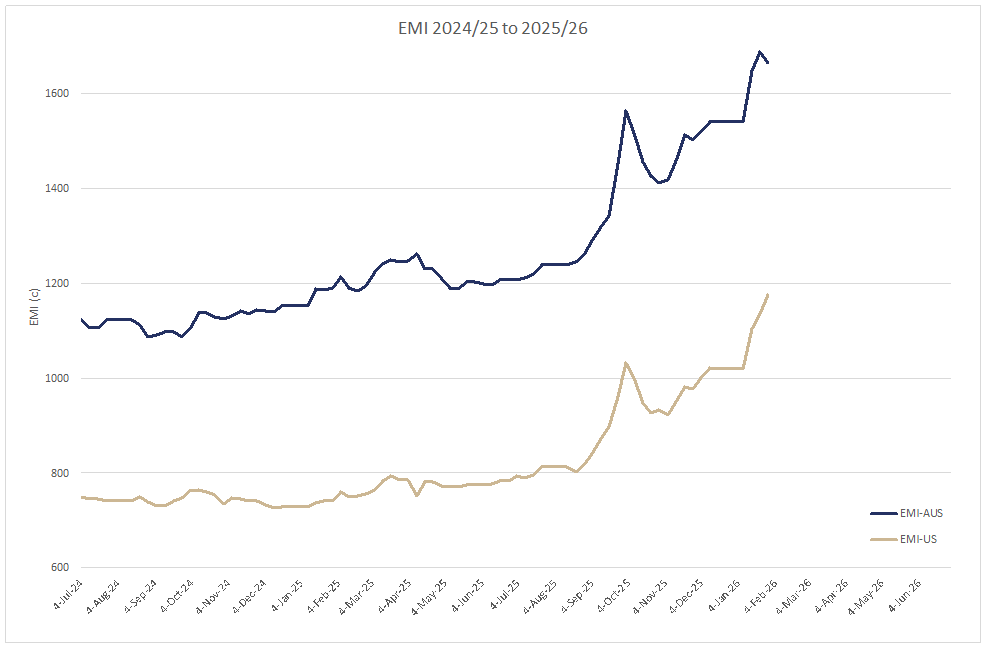

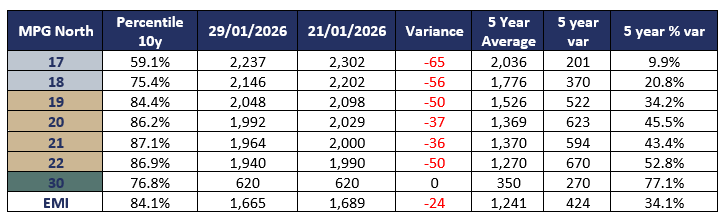

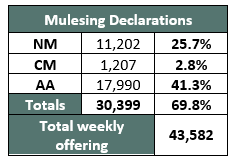

The AWEX EMI closed the week on 1,665down 24c at auction sales in Australia this week. 43,582 bales were offered in all Australian selling centres, with a creditable 94% clearance in an interesting market environment.

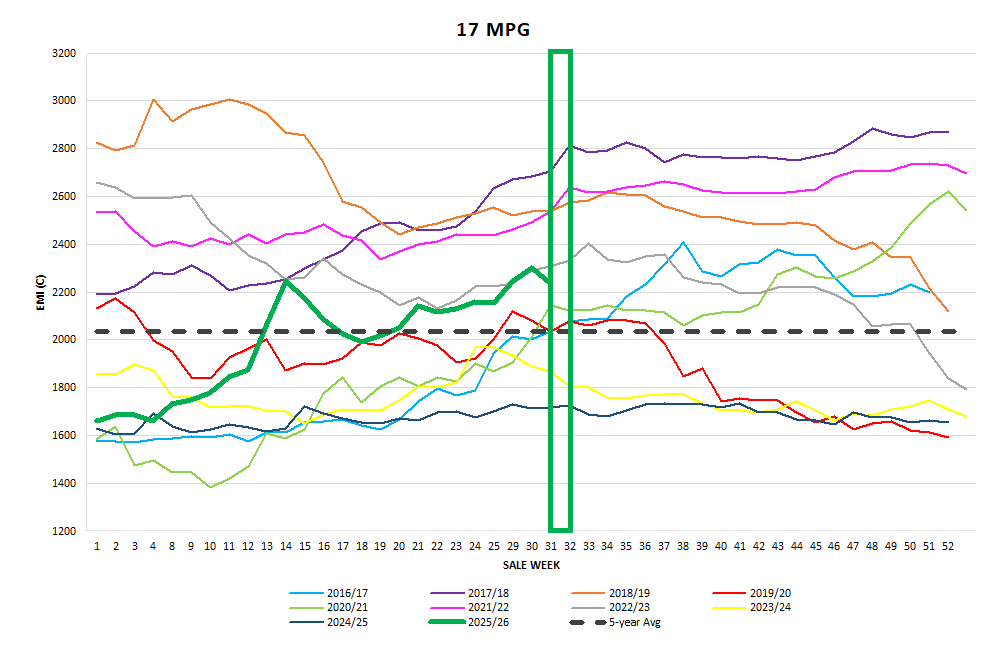

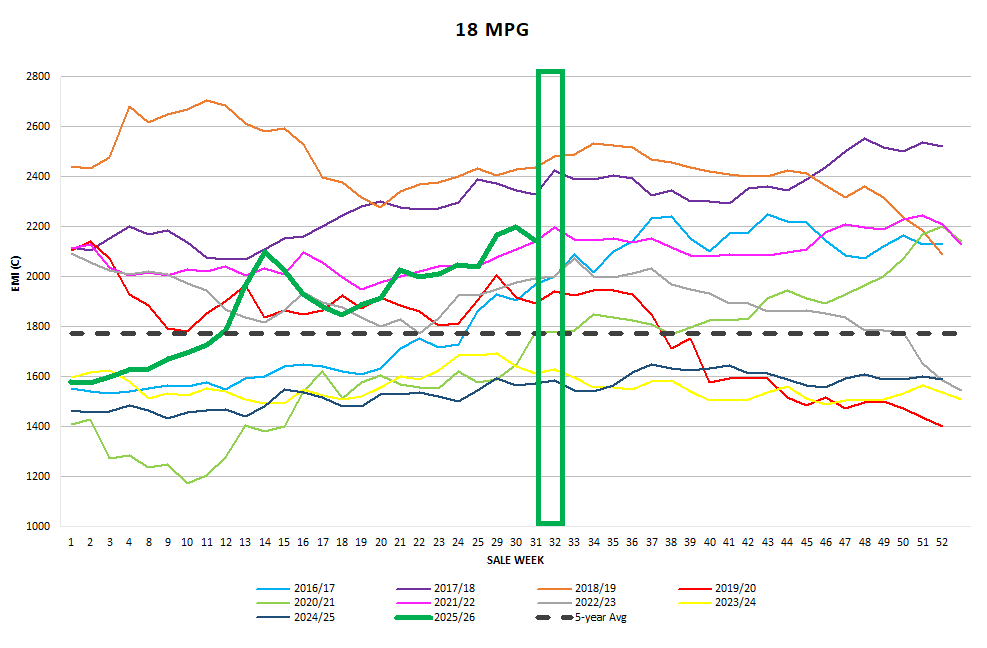

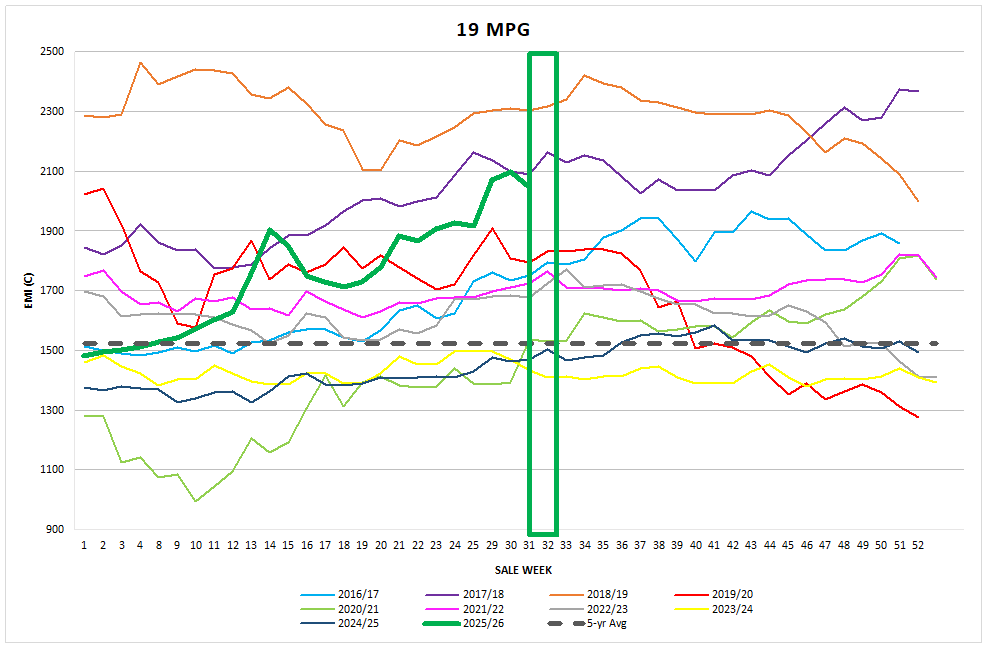

Whilst the EMI broke its almost perfect record for January, the primary reason for the check in the EMI was the AUD punching through the 70c barrier (up 4%) in US$ terms. This was the highest level for the AUD USD exchange in 3 years so despite the headline indices falling 24c the EMI in USD continued to rise, adding 40c this week and accruing156c (+15.3%) for the three sales conducted in 2026.

Competition was dominated by the large Australian Trading Exporters who were challenged by the Chinese Indents and Chinese early-stage processors. Most of the MPG losses were recorded on Wednesday with the EMI falling by 27c. Many exporters reported a distinct change on the price direction late on Wednesday, and this manifested into a solid price consolidation, and in some instances, a slight price rise measured on Thursday.

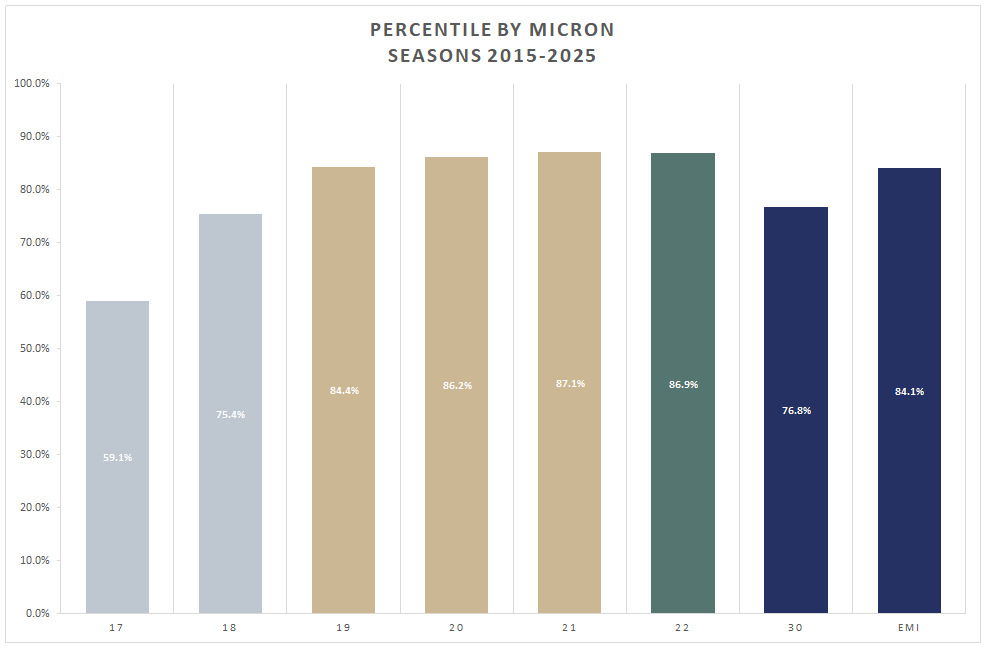

Merino Fleece

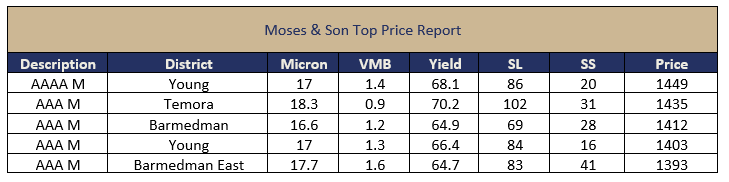

The Merino MPG’s were heavily affected by the Foreign Exchange adjustment and when expressed in USD terms merino fleece wool was dearer across the board. With a slightly higher weekly offering buyers remined selective pushing the best specified lots a lot harder than the out of spec lots, which continue to attract discounts. Thursday’s market saw a reversal of the price drop with some solid prices achieved. Over 55% of the Merino Fleece were purchased by 4 exporters.

Merino Skirtings

Merino Skirtings saw prices follow the trends of the fleece upwards, with the opening day experiencing elevated competition on the bulky (fleece like) well prepared skirtings of most VM content. These bulky well-prepared lots containing under 5% VM continued to rise into Wednesday whilst average style heavier VM lots lost most of the gains made on Tuesday.

Merino Cardings

Merino Cardings ignored the currency exchange anomalies posting solid rises across all centres. Sydney topped the list at +23c whilst Melbourne and Fremantle added 7c and 10c respectively. Crutchings, Lambs and Stains held up well whilst the jewel in the MC crown was the noticeable premium for bulky Merino Locks. 57% of the Cardings were purchased by 4 exporters.

Crossbred Fleece

Crossbred Oddments

Crossbreds

Crossbreds were least affected by the unfavourable currency movements measuring falls of 3 to 15c across the MPG range. 23-28 MPG wool has found a new destination that allows more blending of micron specifications. 4 exporters purchased 57% of the Crossbred offering.

Next Week

Next week the offering is estimated to reduce slightly to 40,480 bales offering in Sydney, Melbourne and Fremantle. The early market intelligence is for a consolidation of the new US prices established this week. With the newly released inflation figures this week the stronger AUD will almost certainly be preceded by an increase in the officialcash interest rates. ~Marty Moses

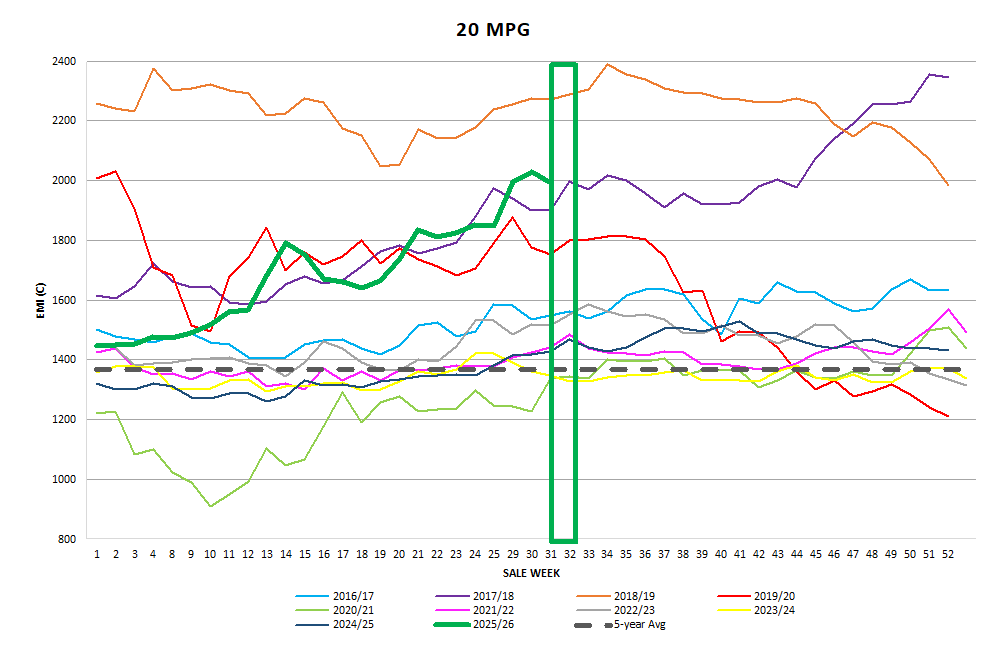

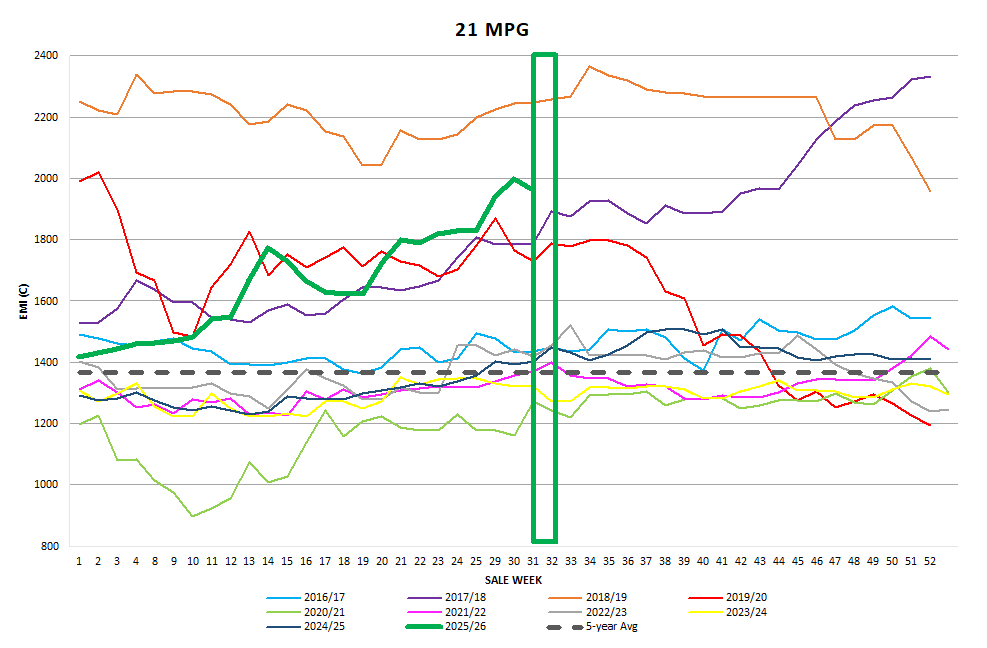

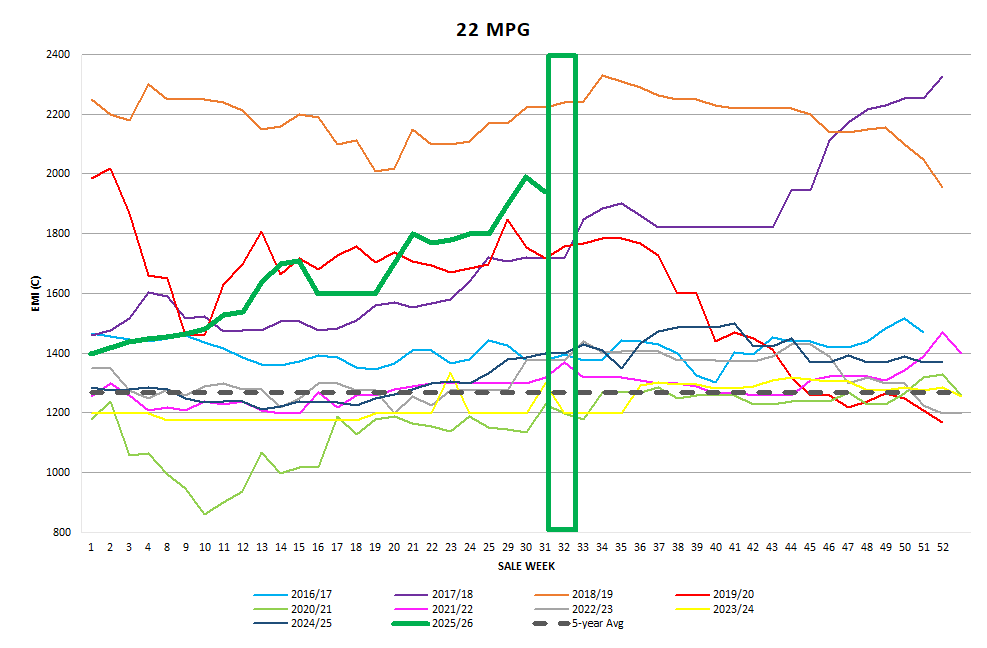

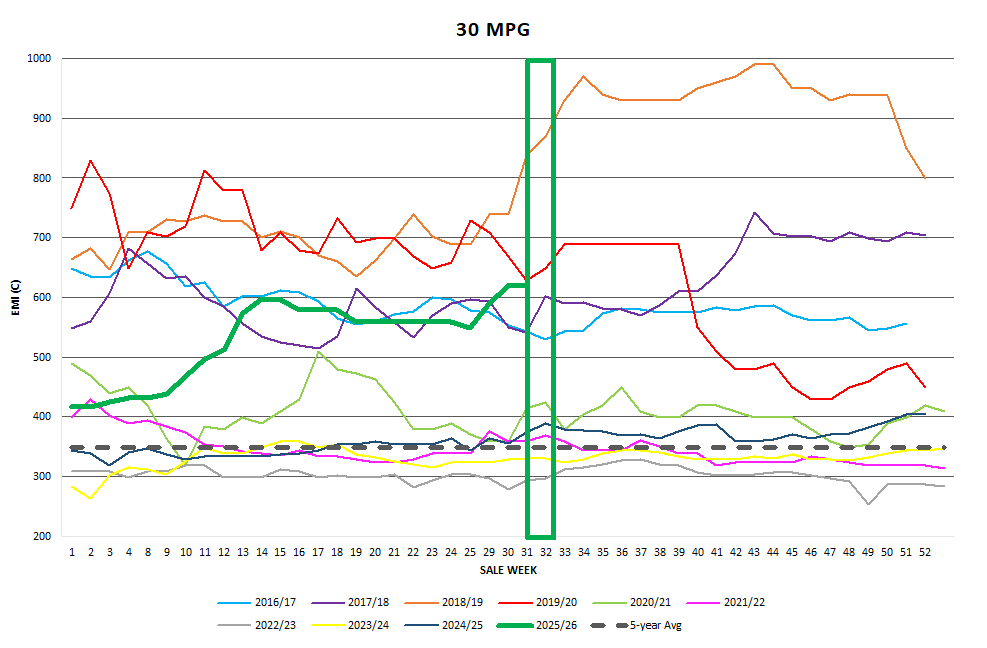

Graphs

Market Commentary

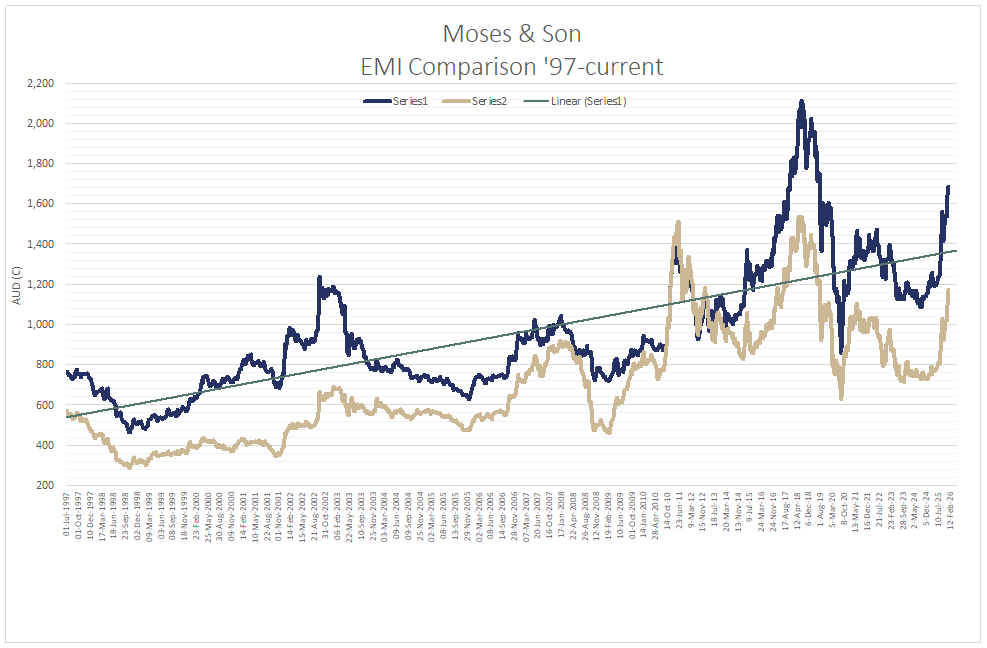

The January wool performance was almost a “straight flush” for the EMI posting 2 of the 3-week series with positive results. The January EMI rises totaled 124c in AUD and 156c in USc. Over the past 4 months there have been many discussions with our clients about the direction of the wool market as the mounting pressure of cropping input costs and average grain prices are being weighed up with the various livestock enterprises. Many discussions have resulted in the recognition of converting below average grain prices coupled with escalating cropping input costs and comparing with the above average Lamb, Mutton and Wool prices. Mixed farming maybe on the verge of a recovery. Hopefully we get a season change that supports this thought bubble.