Market Intelligence

Weekly Wool Market Commentary

Moses & Son is committed to providing our valued customers the most current information and data to empower your decision-making process. Discover our latest Australian wool market weekly update below, along with archived reports for your perusal and analysis.

2025-S40

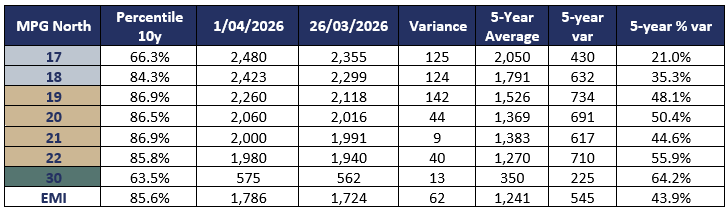

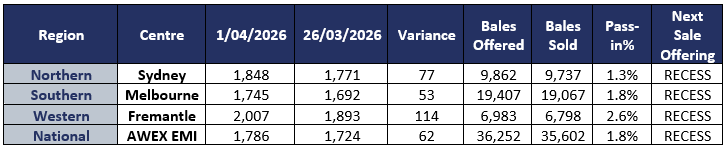

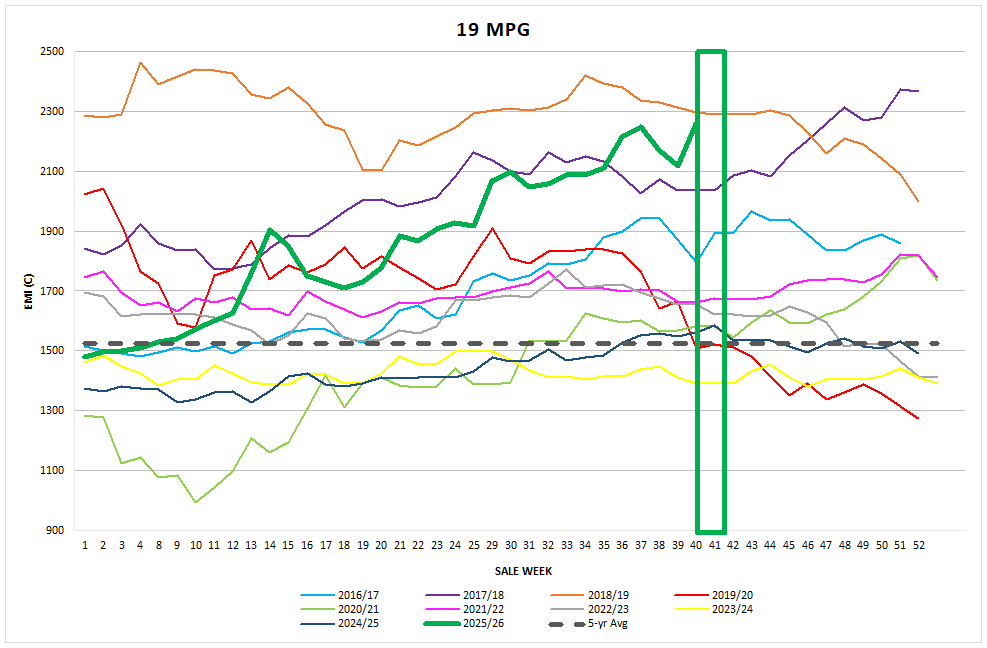

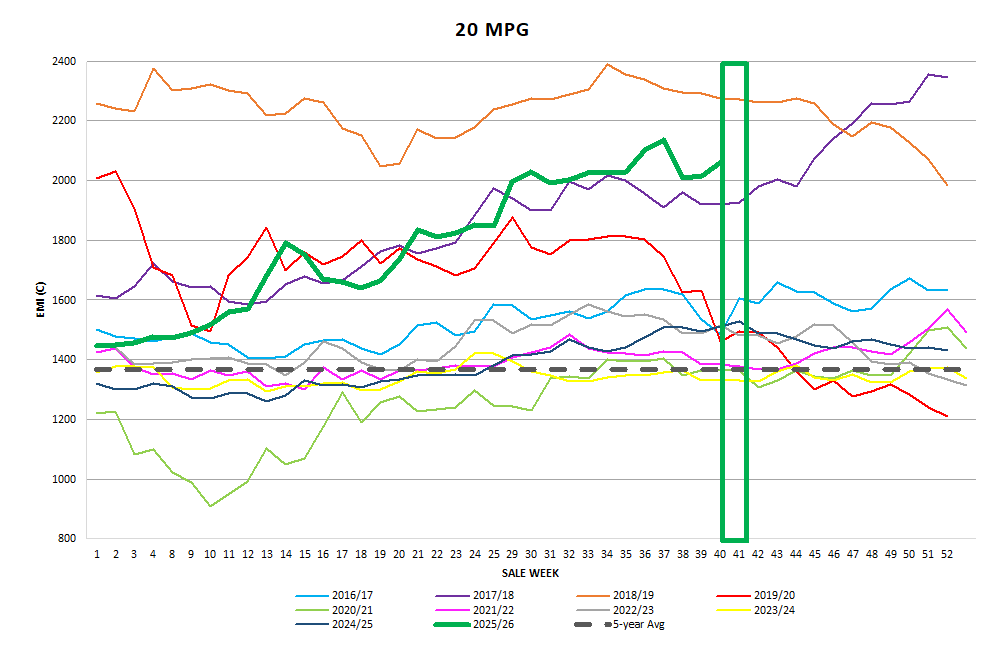

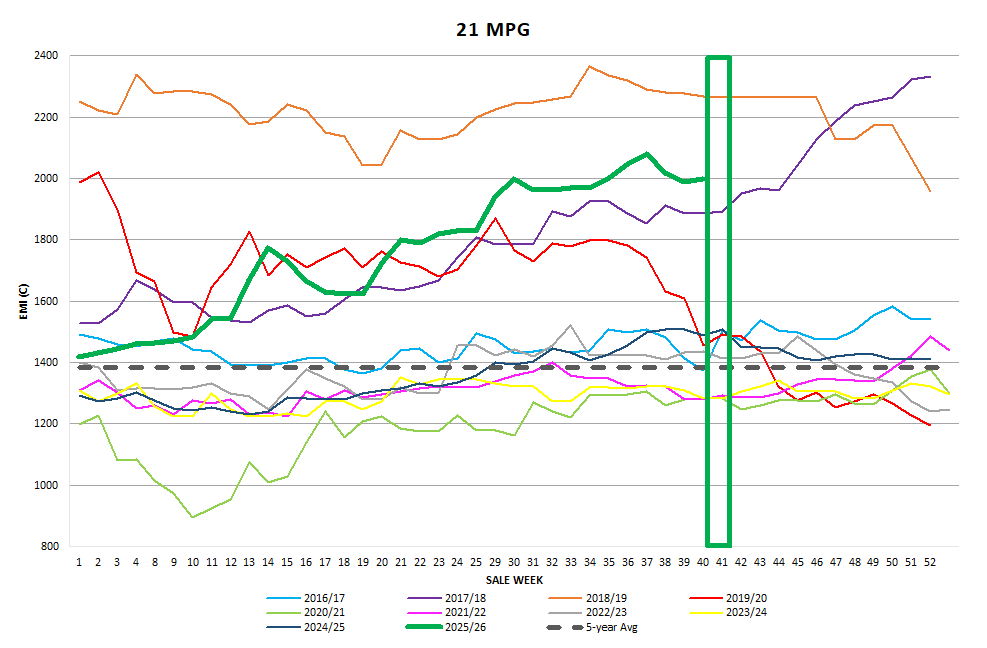

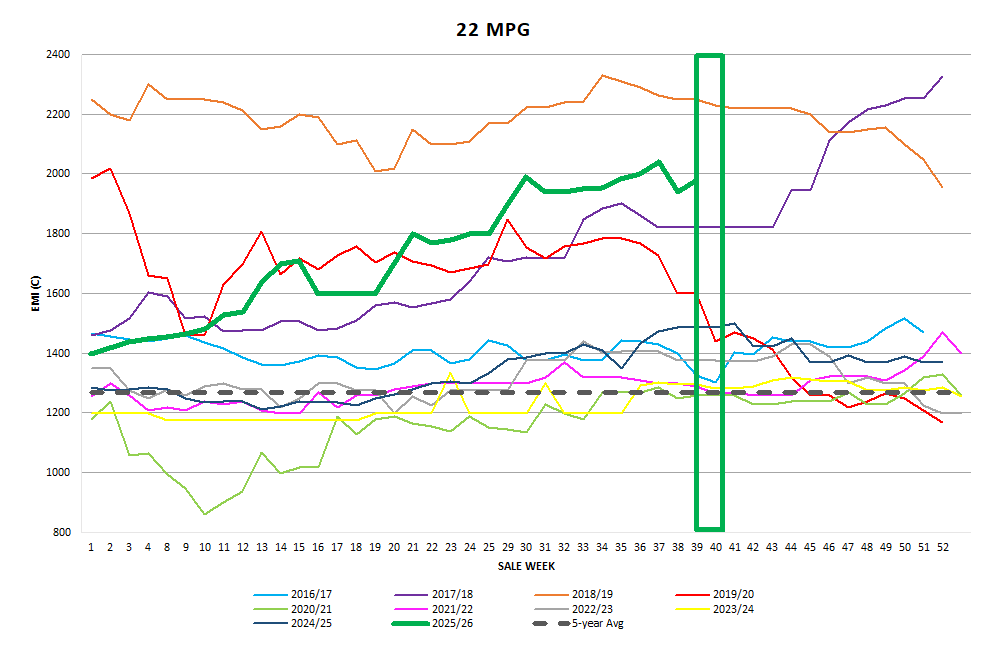

The AWEX EMI closed on 1786c up 62c at auction sales in Australia this week. This week the 36,252 bale offering was aided by a weaker FOREX which fell back to around the 69 USc mark. The EMI in USD terms closed on 1234c up 31c. After the long stretch of weekly price increases, followed by the past two weekly EMI losses, it was encouraging to see the market rebound over both selling days.

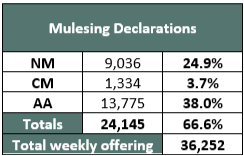

The clearance rate was an incredible 98.2% which is an (unofficial) equal historic high clearance rate. Competition was once again dominated by the large Chinese Indent operators, the Australian based trading Exporters and China’s Top maker. It was evident that next week’s traditional easter sale recess created some competition to secure volume ahead of the break, and sellers may have been motived to capture the current attractive price levels. Whilst the Forward price Contracts traded the discount to cash remains a barrier to any volume of trades. I guess the greater the number of offers may attract more bids.

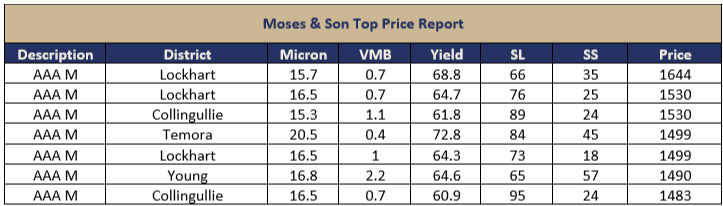

Merino Fleece

The gains were led by the 19.0µ and finer end, pushing up to 130c, with the medium micron categories adding 4556c. Buyer activity was heavily focussed on the well specified and well classed lots with a clear preference for the fleece lots with low vegetable matter. Whilst many of these lots were from previous seasons, this did not hinder the buyer’s enthusiasm. Prem shorn fleece wool also joined the positive price party with at times huge premiums paid for the right specifications.

Merino Skirtings

Merino Skirtings followed the fleece prices upward with the low VM skirts displaying favourable specifications and good preparation attracting notable premiums.

Merino Cardings

Merino Cardings added solid gains with the Northern MC adding 33c, While the South rose 10c. Although Fremantle raced ahead of the eastern centres with a 69c rise in their MC it was only recouping what it had lost over the previous fortnight.

Crossbred Fleece

Crossbred Oddments

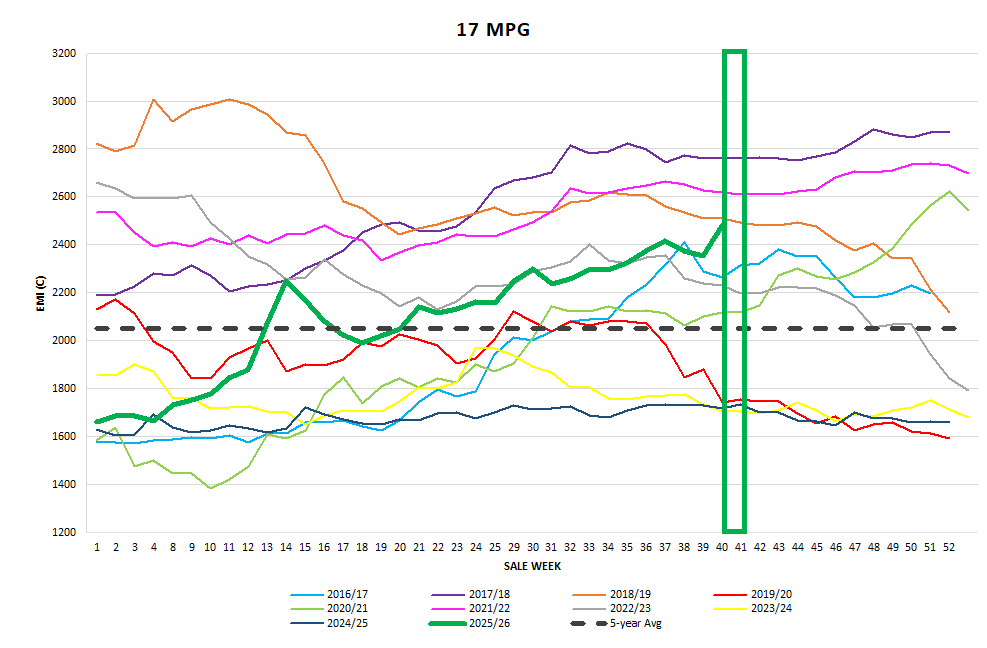

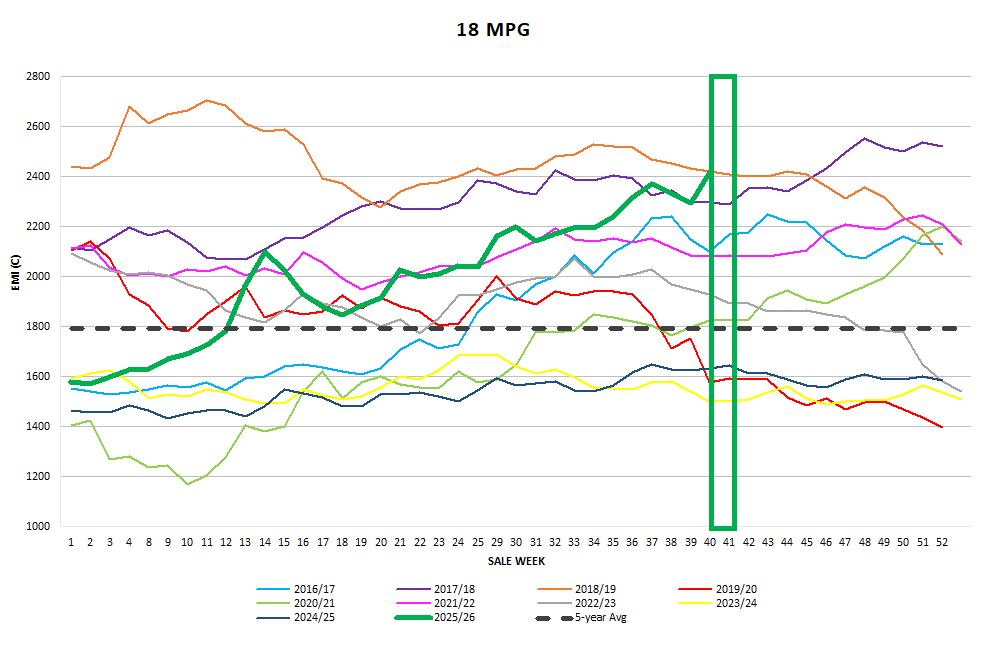

Crossbreds

Crossbreds welcomed the price recovery and despite the rises in the MPG’s being a little lower than their merino counterparts the prices between well specified and classed lots and the average, were worlds apart. Over 70% of the offering was purchased by the top 4 buyers, led by Australia’s largest trading exporter who secured 31% of the offering.

Next Week

Sales will resume on the week beginning the 13th April. I speak for many sellers and buyers when I say that whilst selling wool at the current level is a welcome change next week’s recess will be welcomed. ~Marty Moses

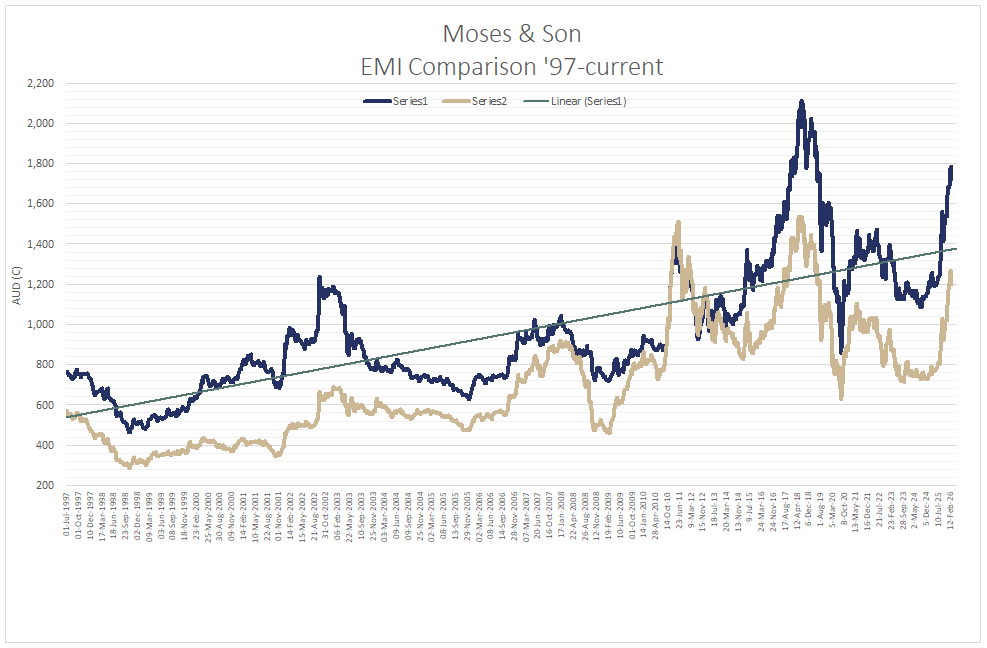

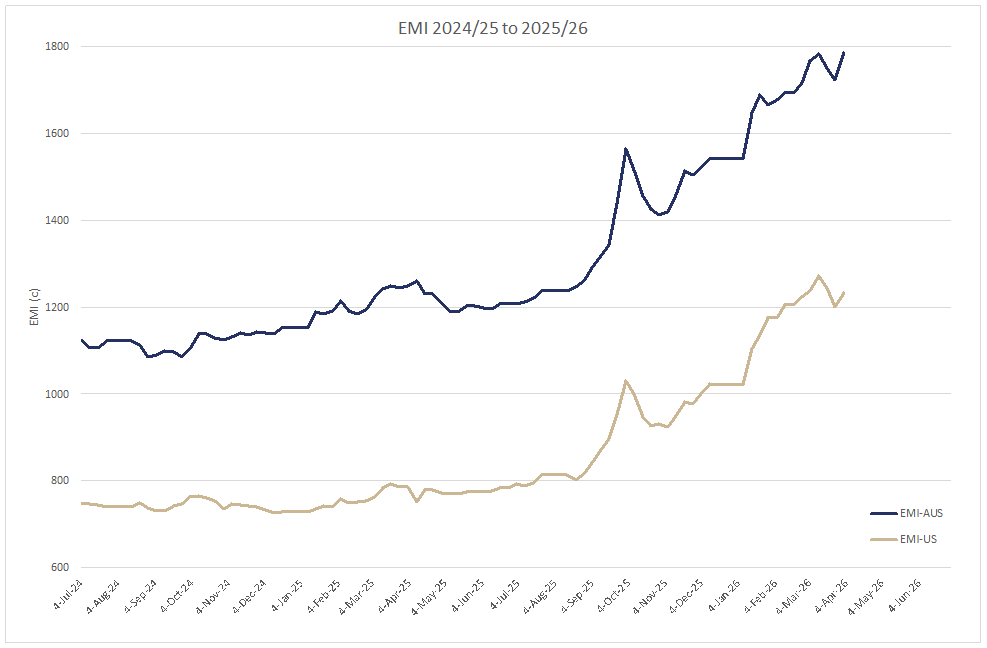

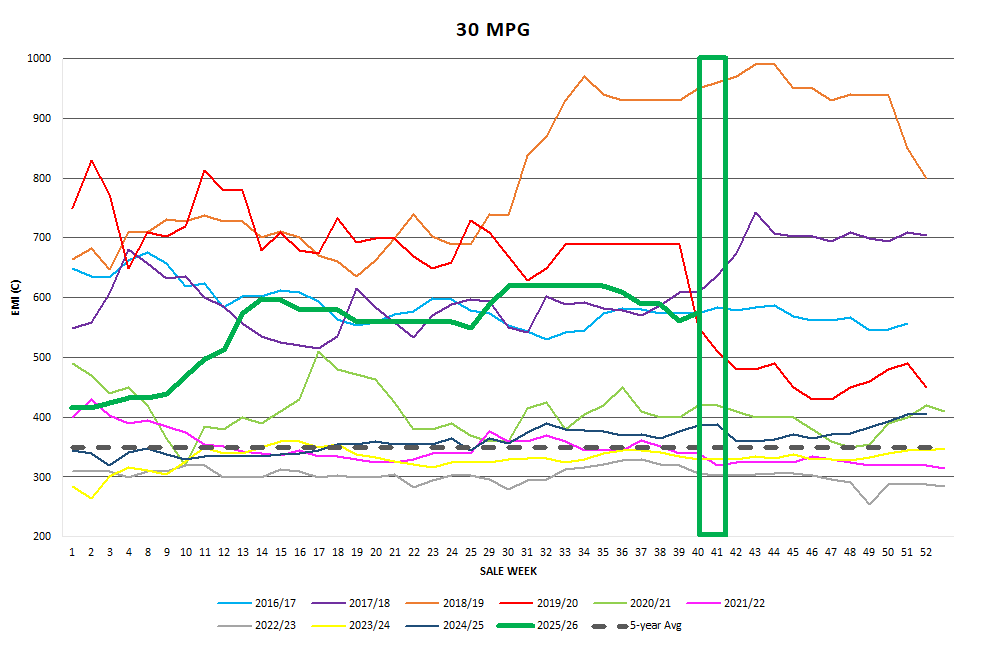

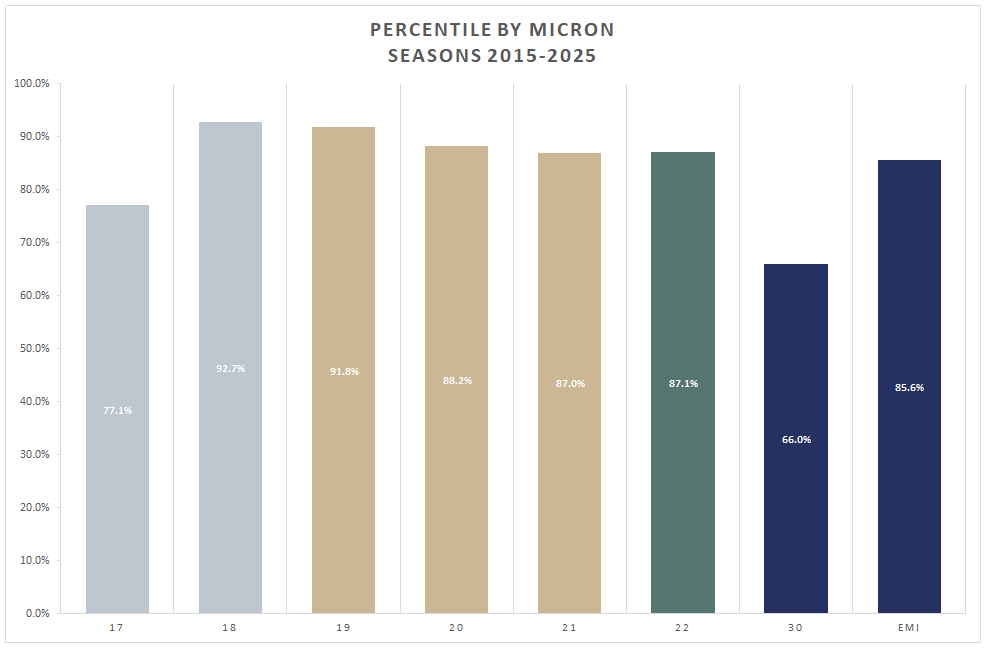

Graphs

Market Commentary

Whilst I would like to have a rant about the current fuel crisis, I’m sure you are all well versed in the frustrations the current situation has produced around the world.

An equally important story went unnoticed by our mainstream news agencies this week. This oversight was brought to my attention from the team at “Keep the Sheep.”

“When Labor banned live sheep exports, they told us new markets would make up for it. Back in 2023, their Agriculture Minister Murray Watt stood up and said the government had ‘opened up big new markets for sheepmeat’ and was hoping to ‘land a good deal with the EU.’ That was the promise. The EU deal was supposed to be part of the answer.

Well, the deal is done. And it stinks. Our industry asked for a minimum of 67,000 tonnes of sheep meat access. We got 25,000. Starting at just 8,300. You know what New Zealand got? Over 163,000 tonnes. For the same product, from the same product, from the same part of the world. That’s not a level playing field. It’s not even close. The deal is basically unchanged from what Australia walked away from in 2023. Back then, Watt himself called the EU’s offer Laughable. Now apparently its good enough. Once again the government has sold out our sheep farmers” ~Ben Sutherland

Both Moses & Son and Gordon Litchfield Wool were able to clear 100% of their offerings this week and cement a pleasing first month of trading since the acquisition took place on the 1st March.

AWTA monthly comparisons of total bales tested for March 2026 compared with the same period season are down 10.3%. The progressive comparison of total bales tested for July 2025 to March 2026 compared with the same period last season are down 9.5%. AWTA Ltd has tested 208.4 mkg this season compared with 230.4 mkg for the equivalent period last season.