Market Intelligence

Weekly Wool Market Commentary

Moses & Son is committed to providing our valued customers the most current information and data to empower your decision-making process. Discover our latest Australian wool market weekly update below, along with archived reports for your perusal and analysis.

2025-S44

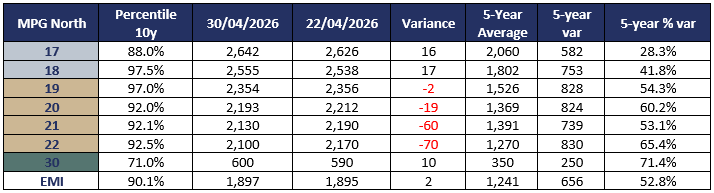

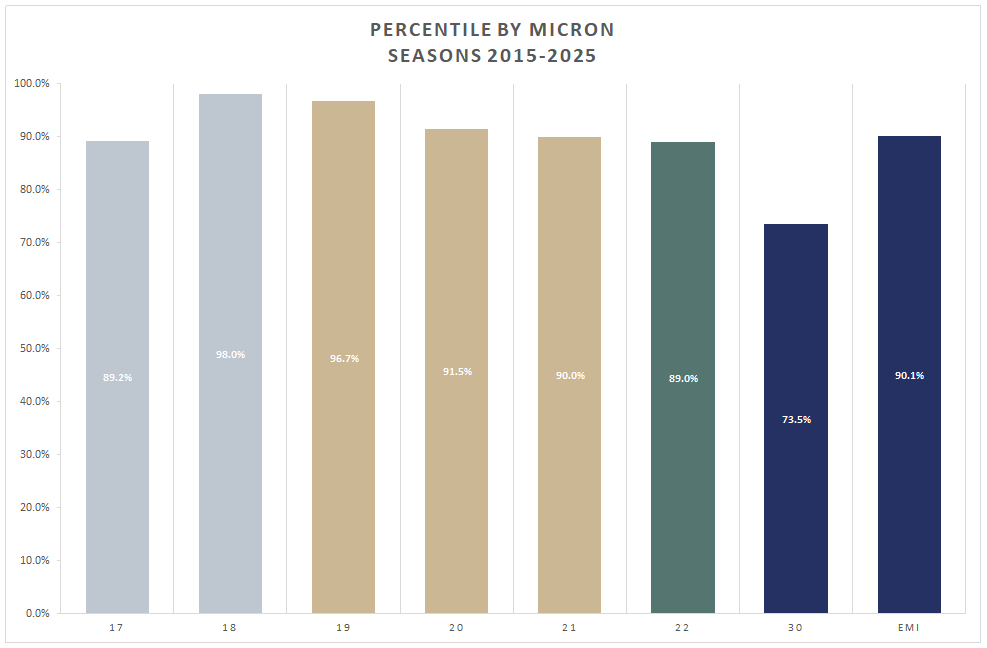

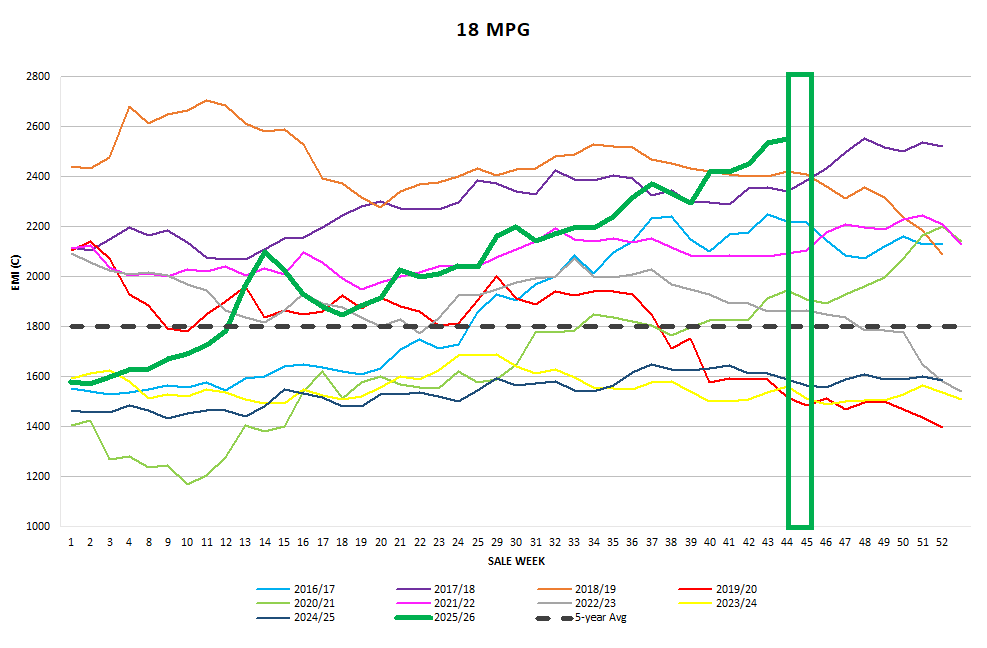

The AWEX EMI closed on 1897c up 2c at auction sales in Australia this week. 37,716 bales were offered nationally after the early estimate of 39,956 bales were published late last week. After a 70c rise in last weeks EMI it was somewhat surprising a number.

Talk of a weaker market and the larger weekly offering may have spooked some but others were withdrawn from sale due to AWTA Test results not meeting the cataloguing deadline. The other sale week abnormality was the split selling centre caused by the misalignment between states of the Anzac Day public holiday. For reasons I cannot fathom the sale roster had Melbourne offering on Tuesday and Wednesday, Sydney offered on Wednesday and Thursday and Fremantle offered on Wednesday only. This meant we had both Tuesday and Thursday sales held in isolation. I don’t believe we could call this orderly marketing as the real benefit of having as many selling centres operational on the sale days creates a positive market environment. That aside 93.1% of the offering was cleared to the trade dominated by the Large Australian owned Trading Exporters, Chinese Indent operators and Chinese topmakers.

Merino Fleece

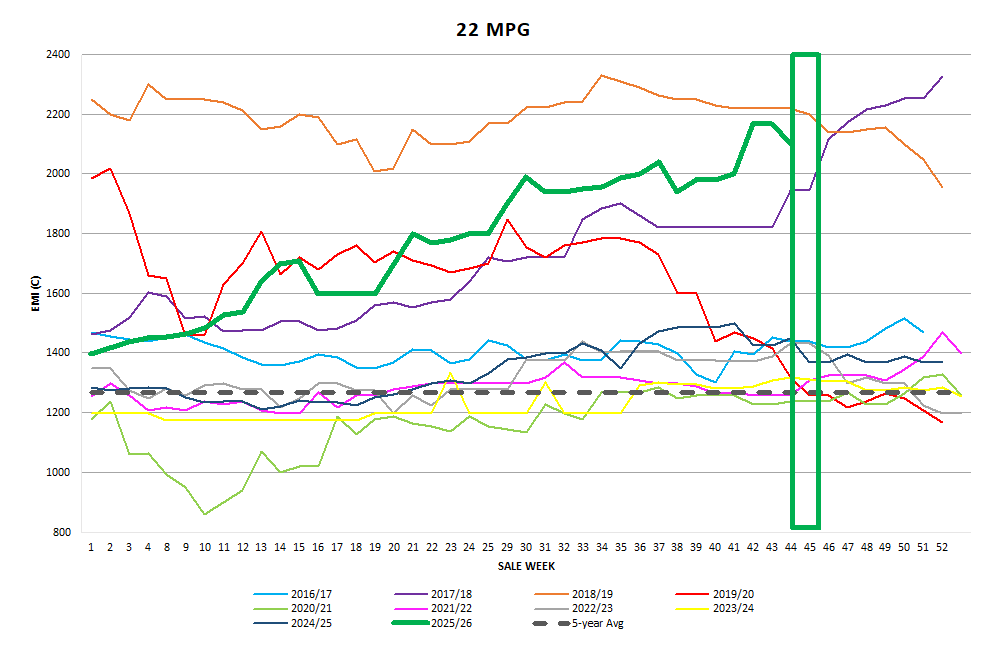

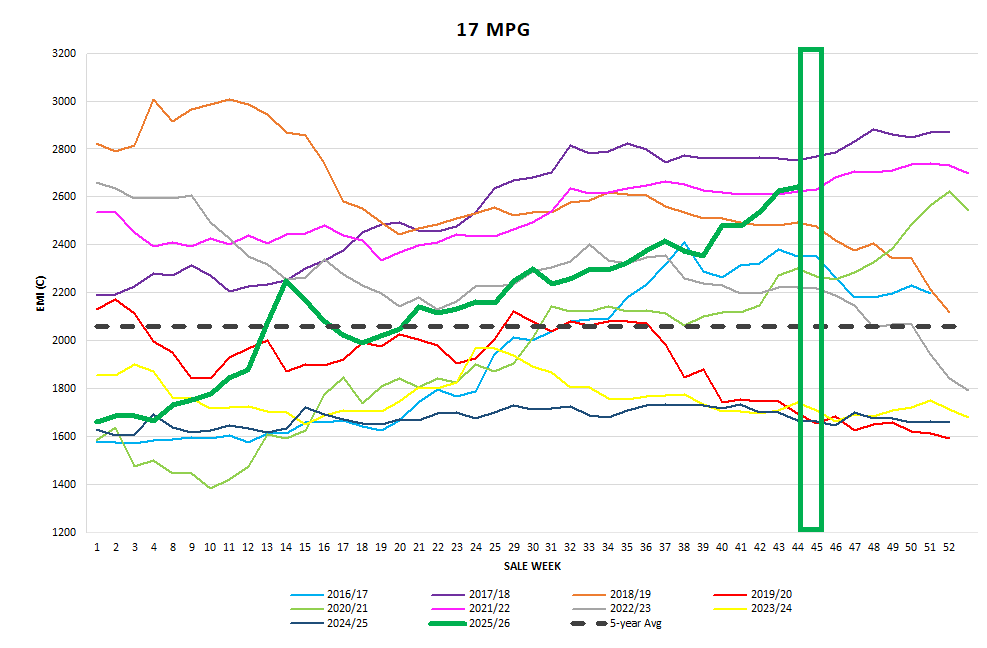

Melbourne opened the with slightly dearer tone on the sub 19 MPG’s and the coarser MPG’s struggled to hold its ground on the opening day. Sydney joined Melbourne and Fremantle on Wednesday with Sydney holding form on the 19 MPG and finer and slightly cheaper on the 19.5 and coarser. Melbourne gave back Tuesdays fine MPG gains the broader lots added to their losses. Interestingly, Fremantle posted price increases on the 18.5 MPG and finer lots but losses of up to 36c were posted on the medium and strong MPG’s. Sydney was Left to sell in isolation on Thursday. Remarkably solid gains were measured on 19 MPG and finer with further losses posted on the 19.5 and coarser MPG’s. Best style and specified lots were keenly sought after each day however the slightly larger offering was met with some buyer selection scrutiny over each selling day. This week the best style and high yielding tableland wool clips grossed their owners above $3000/bale. The general average of an 18.5 micron and finer is $2400-$2750/bale. The market has come such a long way in a short time.

Merino Skirtings

Merino Skirtings posted noticeable gains in each selling centre each day. Best style & bulky skirtings with low VM continued to attract spirited bidding. Good length prems were generally well supported with the shorter end of the length spectrum, slightly cheaper. Fine and superfine short prems generally sold well whilst there is some resistance in the coarser short prem.

Merino Cardings

Merino Cardings the eastern selling centres saw a continued upward weekly trend adding 7c to Sydney and 3c to the Melbourne MC. Fremantle gave back 15c this week. The best bulk merino crutchings continued to attract vigorous bidding and producing unbelievable prices.

Crossbred Fleece

Crossbred Oddments

Crossbreds

Crossbreds were generally dearer at the end of the week. Results are influenced heavily by the style, VM and specifications of the offering on any one day in any centre.

Next Week

Next week the national offering drops back to 34,290 bales, With Sydney and Melbourne offering on Tuesday and Wednesday and Fremantle offering on Tuesday only. The market intel is a bit like last week’s projections. As at today the early intel ranges from up 50c or down 50c. It is likely we will see the current increase in demand on the better style and specifications being experienced in Chinese domestic retails sales continue and keep this market at around, or above these levels. The short/medium term for wool looks more promising. ~Marty Moses

Graphs

Market Commentary

Early on in the week I was hopeful the Easten Market Indicator would break through the 1900c barrier and whilst it did not hit that benchmark, wool producers must be doing a happy dance with the returns from the wool clips at the minute. The Australian Wool Production Forecasting Committee’s (AWPFC) first forecast of shorn wool production for the 2026/27 season is 243.9 million kilograms (Mkg) greasy. This is 4.5% lower than the 2025/26 final forecast.