Market Intelligence

Weekly Wool Market Commentary

Moses & Son is committed to providing our valued customers the most current information and data to empower your decision-making process. Discover our latest Australian wool market weekly update below, along with archived reports for your perusal and analysis.

2025-S50

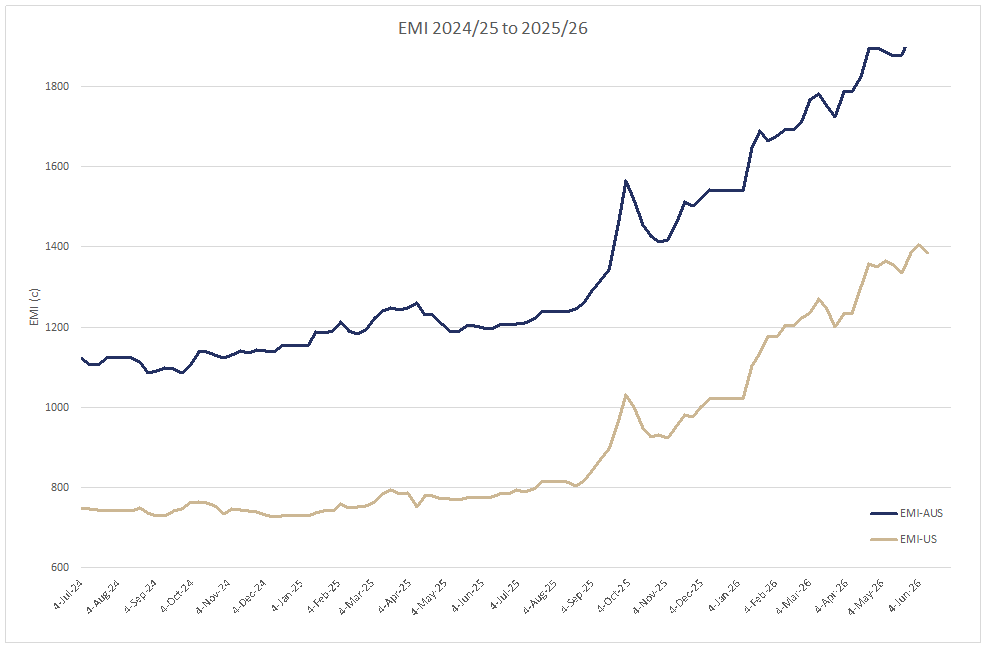

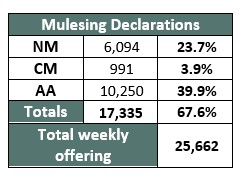

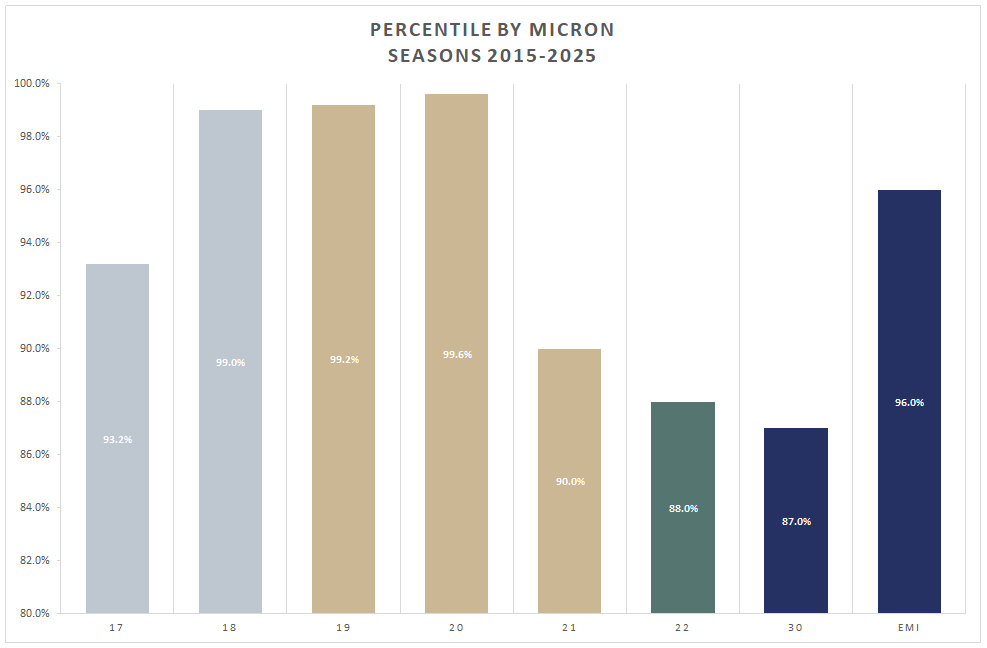

The AWEX EMI closed the week on 1979c, up 15c at Auction Sales held in Australia this week. With all centres offering 25,662 bales this week the lower number kept pressure on prices across most MPG’s and wool categories and produced a clearance rate of 96.7%.

Just to note that this week was the smallest 3-centre National offering since 2020. Competition came from a wide range of exporters with Chinese Indents and Top Makers keeping the Australian Trading Exporters on their toes especially in the Merino Fleece categories this week. Currency weakened early in the week and despite the EMI opening the week up 9 AUc on Wednesday in USD terms it washed of 22 USc, falling back off its 1407c level achieved last week to close on 1385USc. Thursday saw the EMI rise another 6c, whilst the EMI in USD held firm.

Merino Fleece

Trying to accurately describe what the Merino Fleece price trends were across the three centres in the smaller weekly offering is almost impossible. If I said “all the MPGs were fully firm” it would be a pretty accurate reflection of the sentiment. Of course, the exception of lots with low N/kt and high VM lots may have bucked that trend. The Merino MPG measured rises to 50c, with the best style, high yielding, and low VM keenly sought. Good Merino prem - shorn Fleece lots were also notably dearer this week. The top 4 buyers purchased 61.4% of the Merino Fleece offering.

Merino Skirtings

The market opened the week on a positive note, gaining up to 30 cents on Wednesday, with this momentum carrying through into Thursday's sale. Lots containing 5% VM or more maintained firm prices through to the close. Competition was dominated by the Australian Based trading Exporters and pushed all the way by China’s largest Top Maker. The Top 4 buyers took 60.3% of the skirting offering.

Merino Cardings

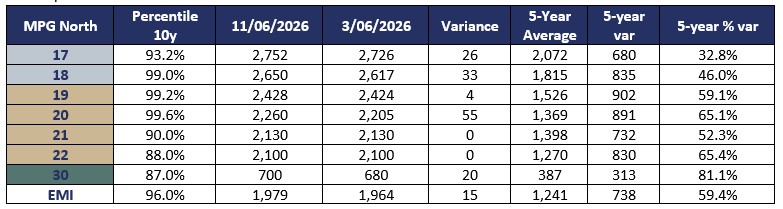

Measured a 24c increase in the Northern region to close on 1229c the highest level in over 7 years. Whilst most lots increased in price there was bullish competition for combing length crutchings and stain. New innovations in processing have seen mills combing shorter wools than we have seen ever before to meet the demands of the knitwear sector.

Crossbred Fleece

Crossbred Oddments

Crossbreds

A small Northern region was quoted generally dearer on nominal quotes with the Southern offering measuring similar price rises in the 28 MPG and finer lots whilst the 30 & 32 MPG’s held firm.

Next Week

Next week’s offering drops back to 21,720c with Fremantle’s alternate week offering the key difference. This is the smallest weekly offering in exactly 12 months and the early market intel is for little or no change. ~ Marty Moses

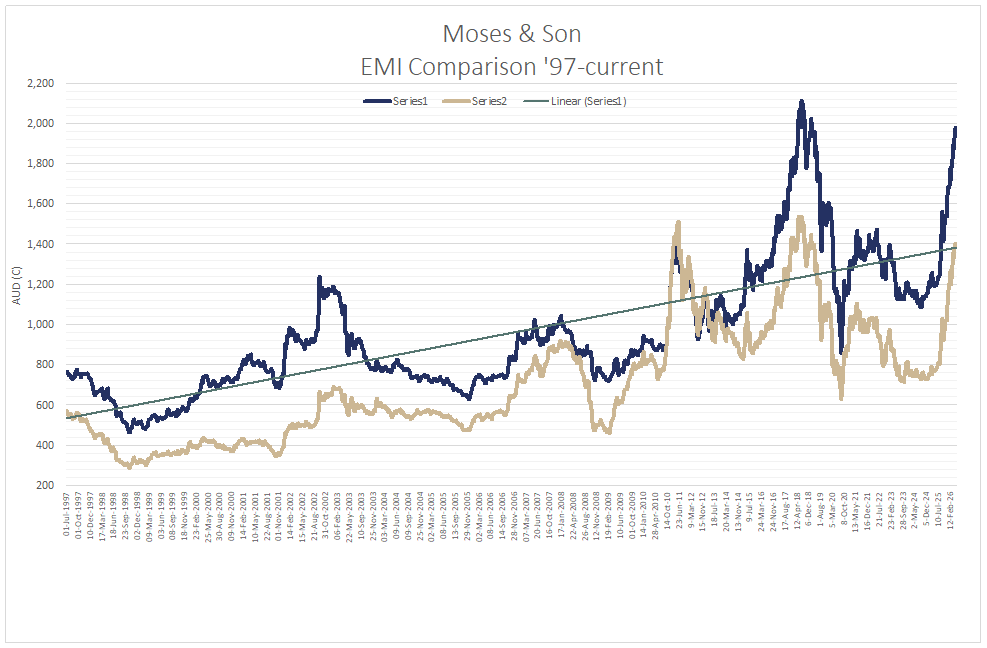

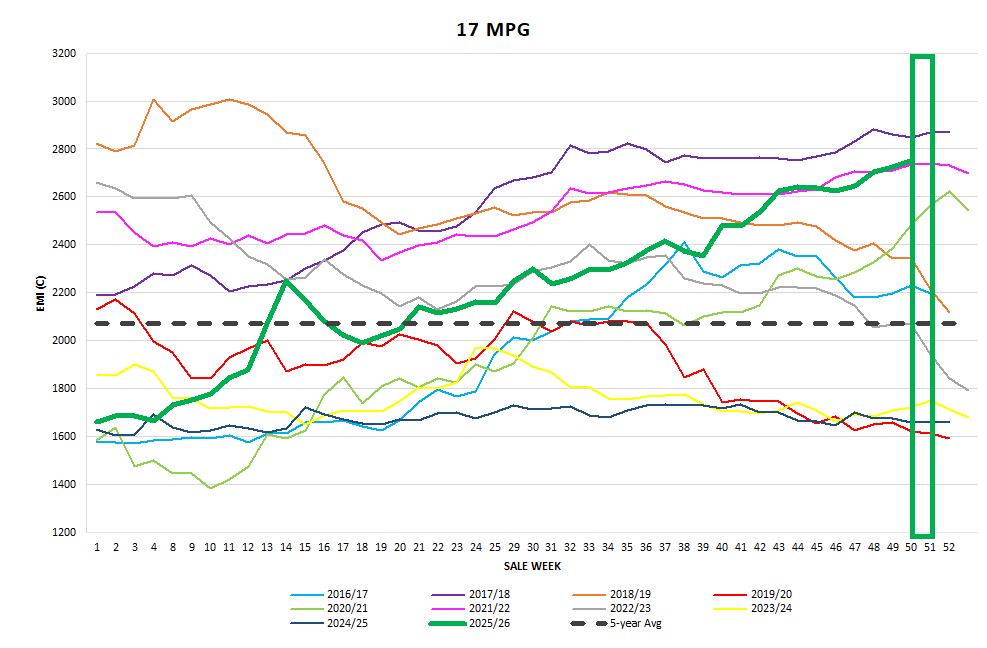

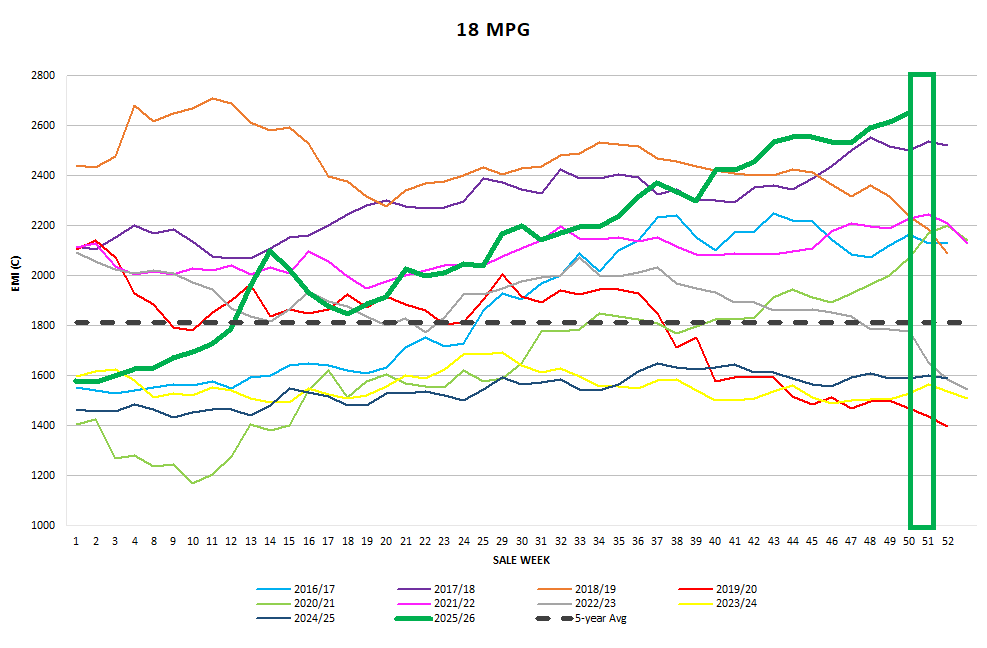

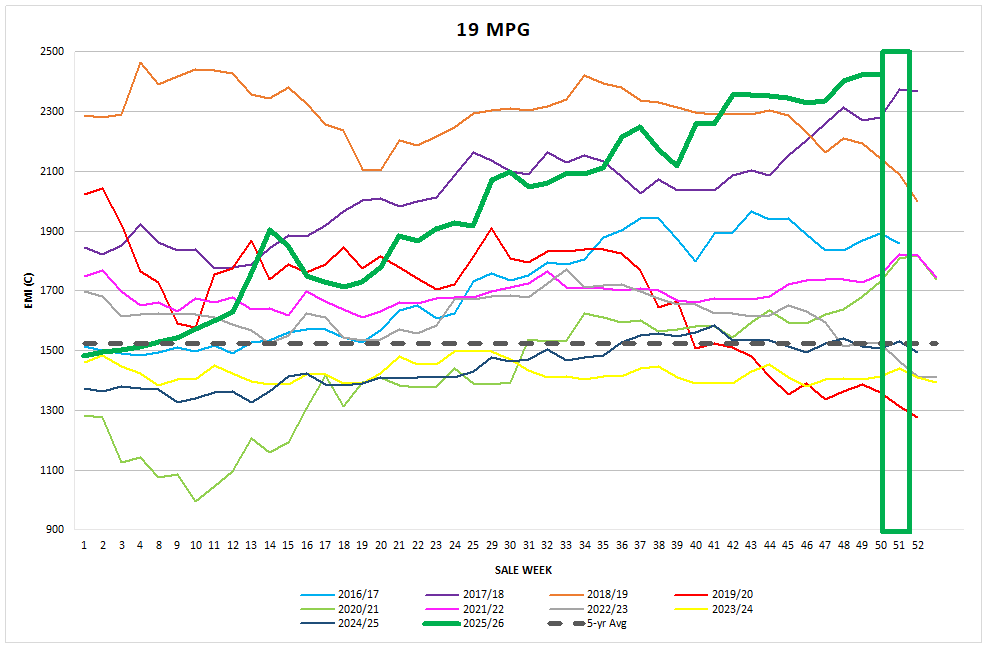

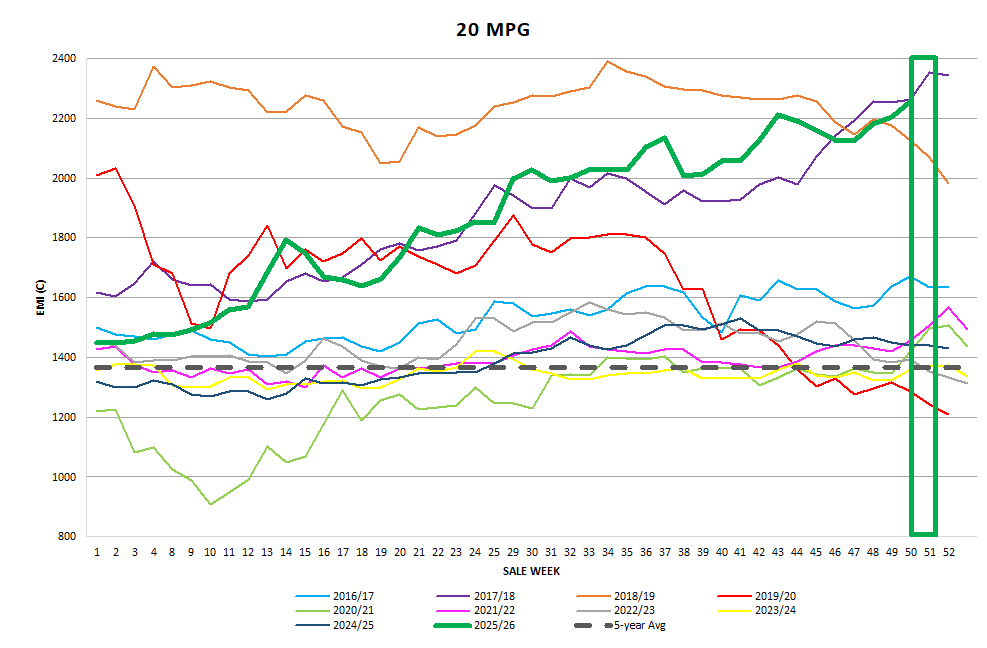

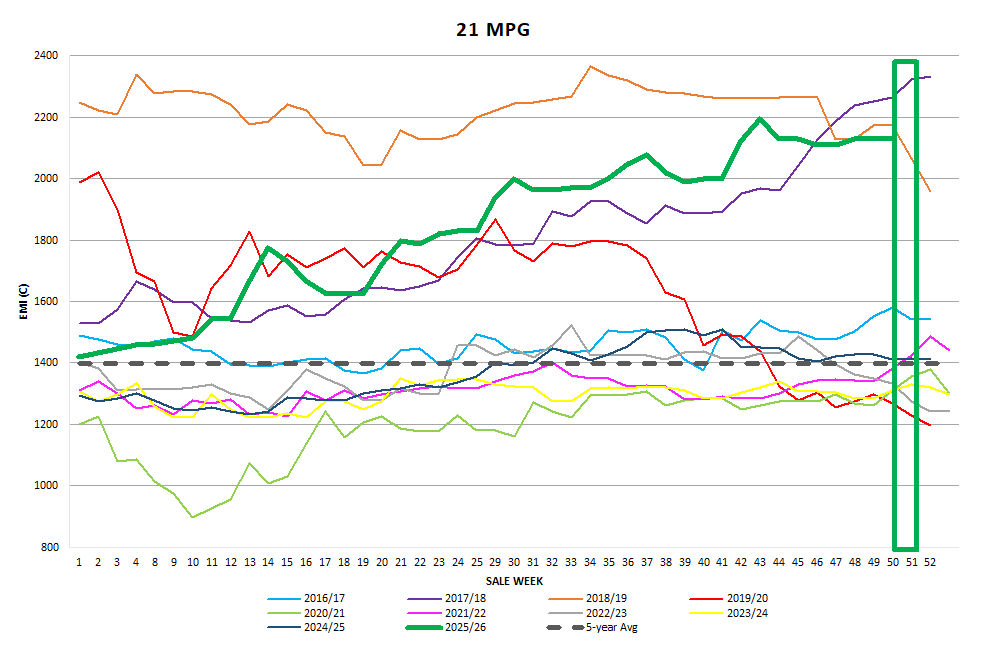

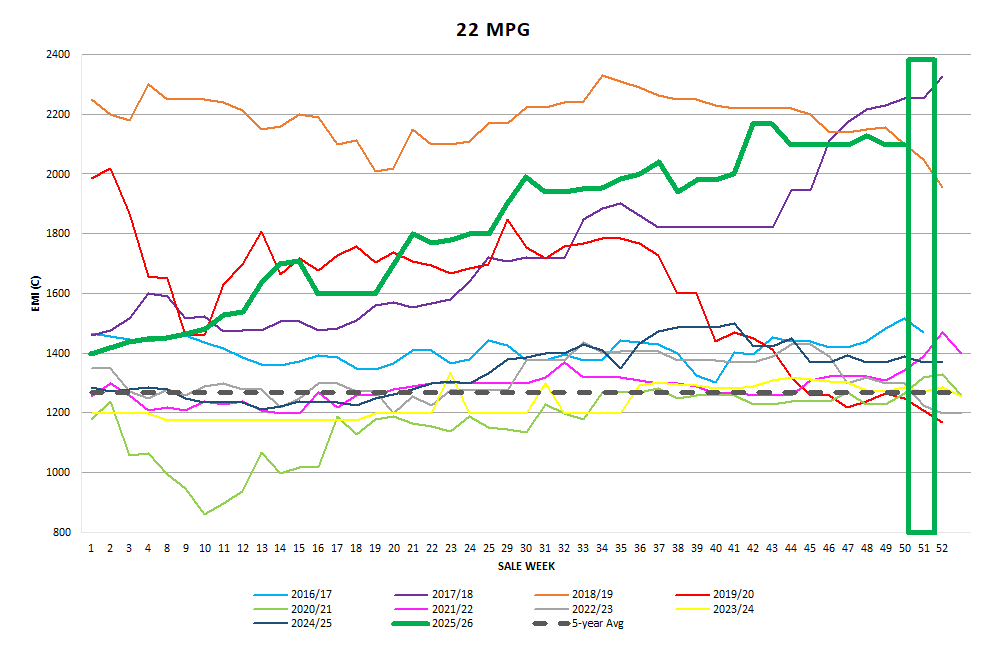

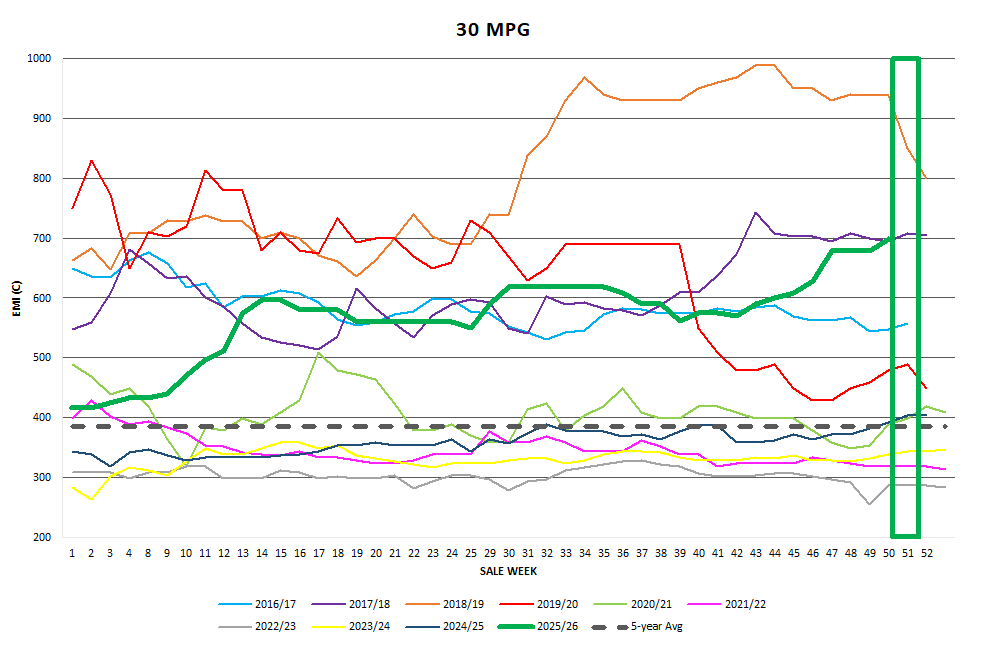

Graphs

Market Commentary

Despite the EMI adding 15c this week the red flag was the 22c fall in the EMI in USD terms. In conversations with our exporter and processor friends there is a general consensus that merino fleece prices are hitting high resistance levels. However, the Indent buyers are scrambling to secure stock to keep the mills ticking over, and with small weekly offerings and a three-week break looming it’s hard to see the Merino Fleece market moving far from here. Skirtings Crossbreds and Cardings look set to keep performing well. There are reports of some perceived price resistance from the downstream processors which is becoming more frequently in conversations. So are we at the top or are we finding a temporary level before the volatility kicks in?