Market Intelligence

Weekly Wool Market Commentary

Moses & Son is committed to providing our valued customers the most current information and data to empower your decision-making process. Discover our latest Australian wool market weekly update below, along with archived reports for your perusal and analysis.

2026-S03

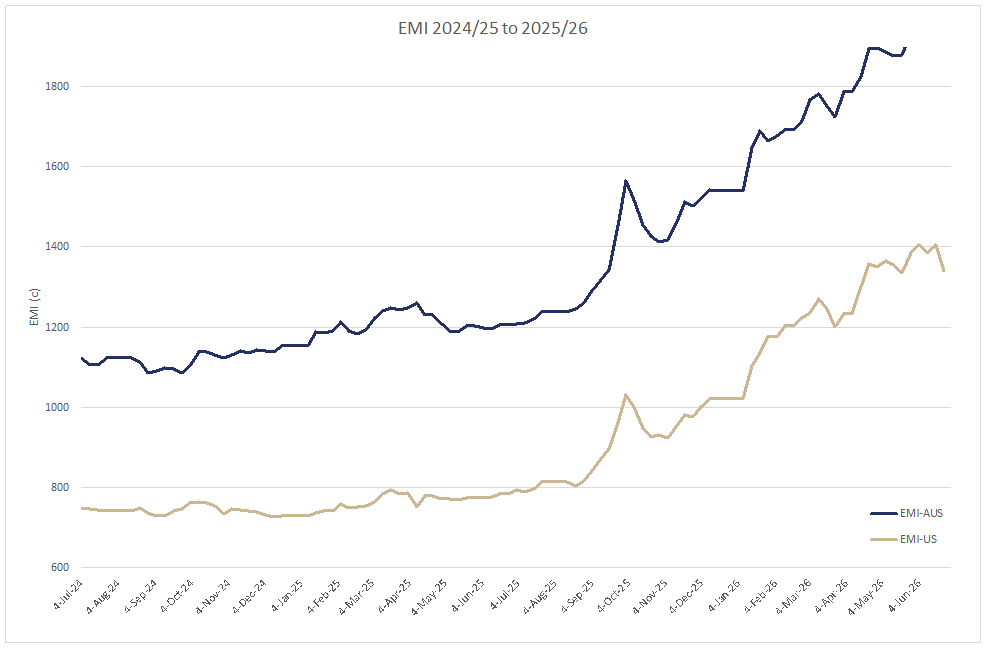

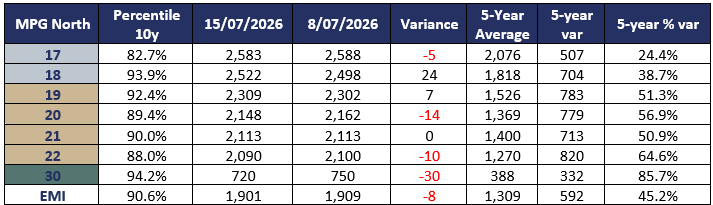

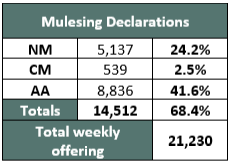

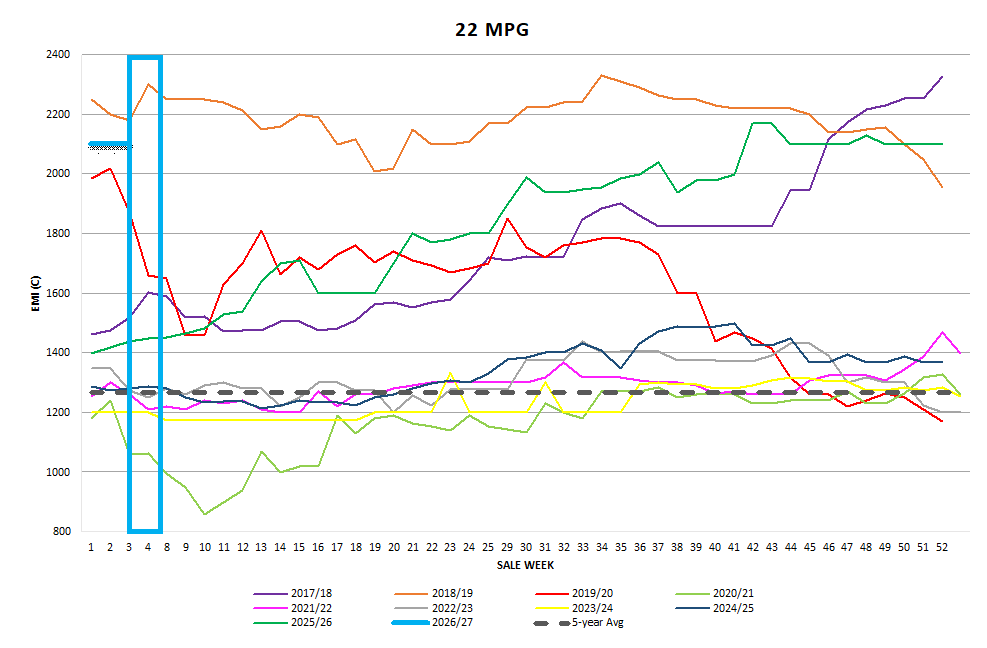

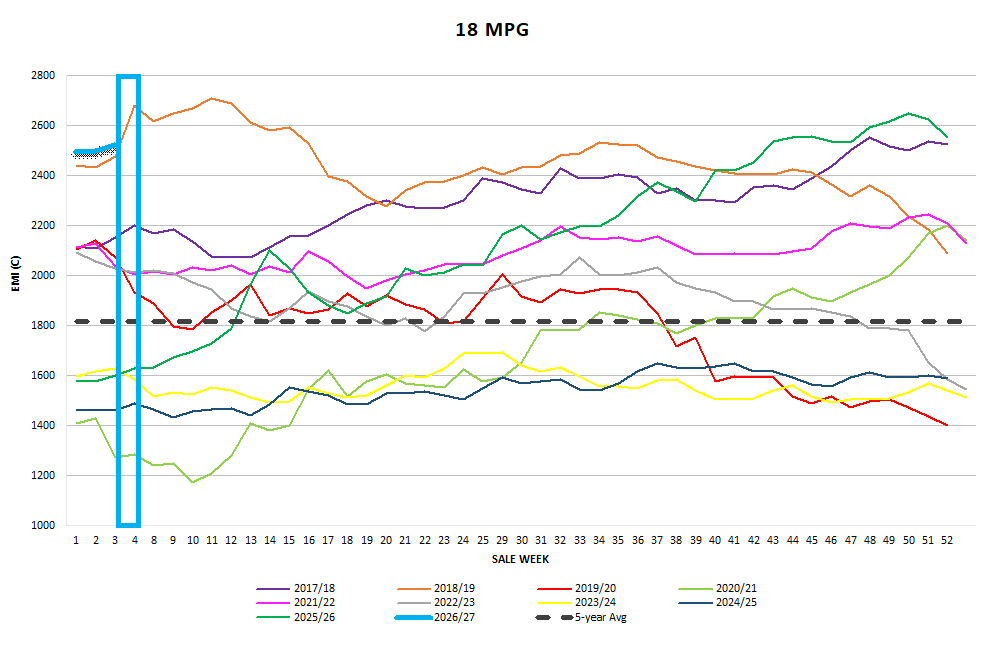

The AWEX EMI closed on 1901c down 8c at auction sales in Australia this week. 21,230 bales were offered for sale with Fremantle sitting the sale out this week. 91.5% of the offering was cleared to the trade as exporters remained selective in their purchases, as they prepare for the 3-week recess after next week. The EMI fell just 1c on Tuesday but as the sale progressed, Wednesday posted a 7c loss with the Merino MPG’s holding their ground whilst the Crossbred and Merino Carding indices took the heaviest hit.

The AUD strengthened this week placing additional price pressure on the market. For note the market opened when the AUD was 69.13c and reached a high just over 70c which was enough to create some apprehension in the competition. In relevance the fall is meaningless when you look at the EMI which was 1221c at the same time last year. That puts the EMI at 55.7% up year on year.

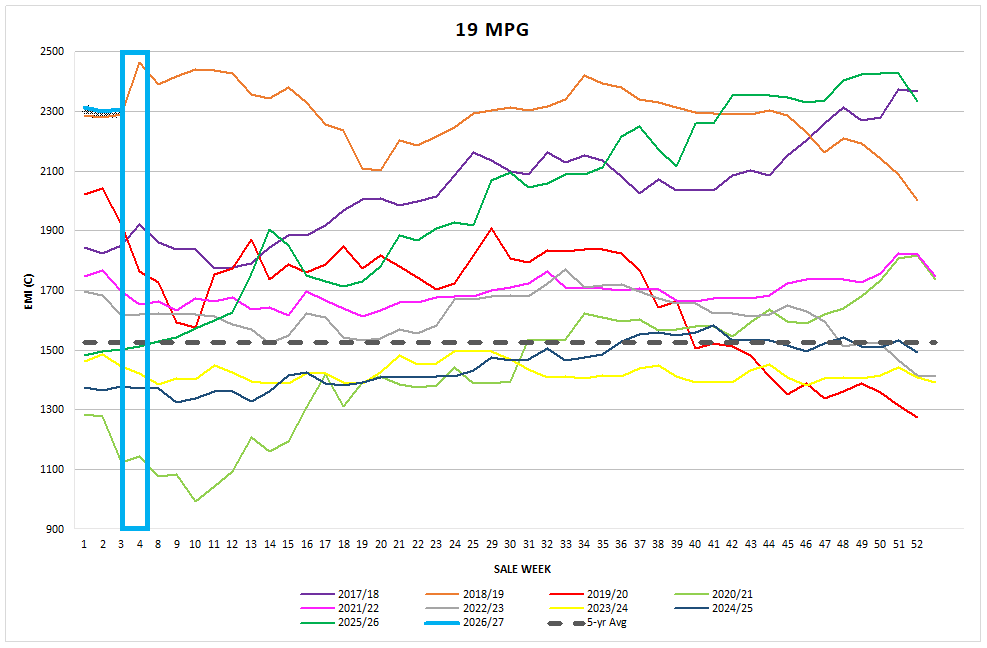

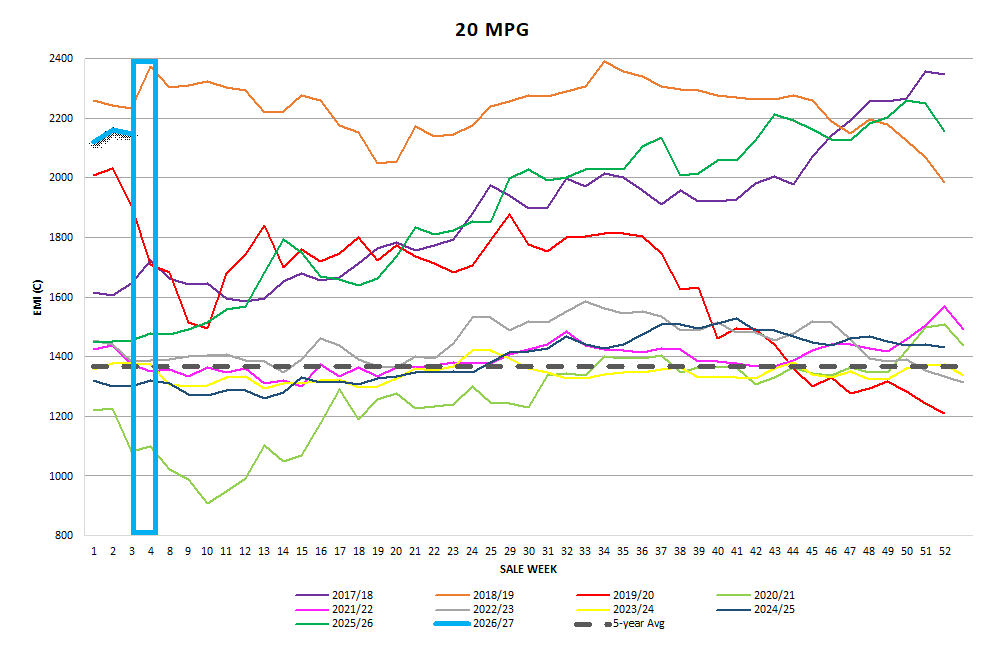

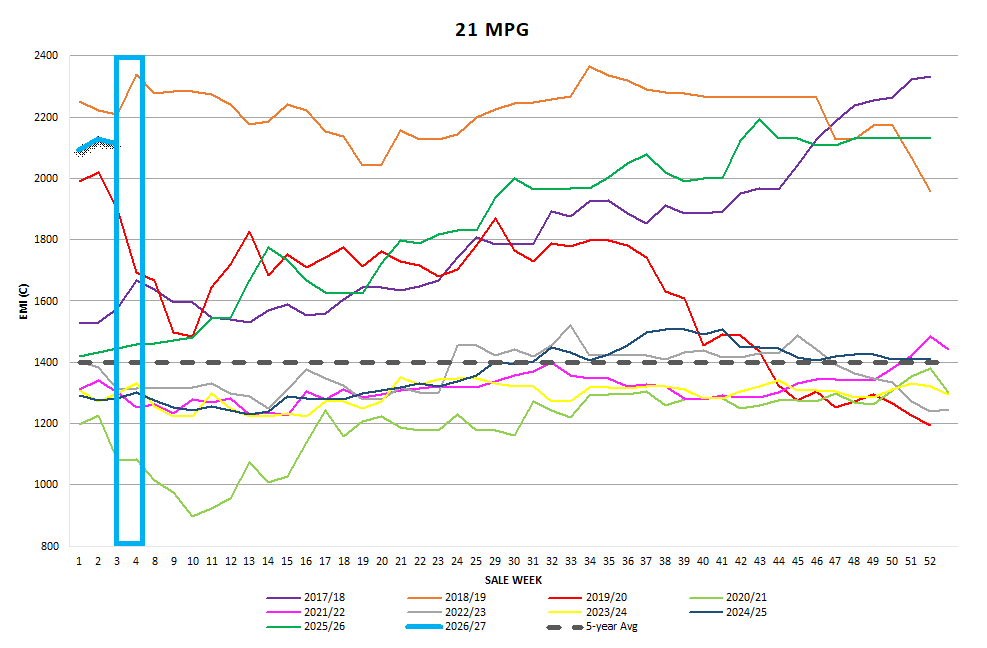

Merino Fleece

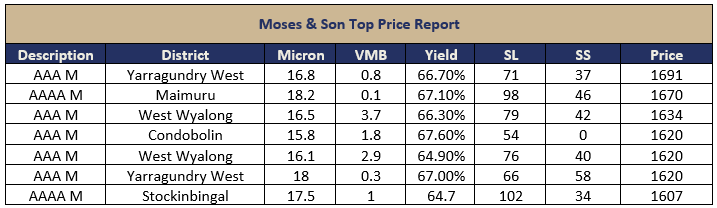

The Northern Indices closed 3c stronger for the day, with somewhat mixed results. An offering of 35NKT, 17.5μ and finer fleece fell between 8 to 17c whilst the broader microns > 38+NKT gained as much as 19 c. With Currency working against the market, the market closed today with minor movements in the merino fleece. Generally speaking, 18μ and finer measured small increases in Sydney in contrast to Melbourne’s negative performance. 18μ fleece wool and coarser lost ground in both selling centres. The Top 4 buyers were evenly apportioned between the trading exporters, Chinese Top Makers and Chinese Indents who collectively purchased 53.7% of the offering. Something I have not seen before was the evenness of the top 4 buyers with just 74 bales separated the 1st and 4th largest buyers.

Merino Skirtings

Tuesday experienced a well-supported skirting market that attracted spirited competition on lots with less than 3%VM, the 17 μ and finer skirts were keenly sought after and sold at a 20c premium . Most other types remained firm on last Thursdays closing level. Wednesday remained generally unchanged for the best prepared and specified “brokens”, whilst heavy VM and poor style fell up to 10c.

Merino Cardings

Tuesdays MC closed down 5c, and whilst support rallied for combing length crutchings & stain there was a distinct fall in the price for 19-micron locks, with 2-5%VM. This pullback alone caused the negative impact on the carding indicator. Wednesday’s market experienced locks & crutchings falling back around 30c across all types and descriptions. Whilst the average bulk took a hit, I did note that our Gordon Litchfield Wool Brokers clients had 4 lots of bulky Merino Crutchings sold for 1540c, 1450c, 1400c and 1320c greasy. Extraordinary prices for Crutchings.

Crossbred Fleece

Crossbred Oddments

Crossbreds

Crossbreds remained firm on Tuesday but as the AUD rose against the USD, the offerings came under some price pressure with falls of 5-23c measured across the 25-30µ MPG’s. Competition from the top 4 operators purchased 61.5% with Trading Exporters, Chinese and European Processor and Chinese Indents dominate.

Next Week

Next week’s offering will be the last sale before the 3-week mid-year recess. After sitting out of the sale roster this week, Fremantle will offer 4,013 bales next week pushing the total weekly offering to 32,397 bales. The early market intelligence seems to unfortunately indicate a downward correction for the Merino and Crossbred sector. Whilst the past few seasons we have seen exporters protecting the last week to increase the chance of selling stock and creating forward sales into the new season, my conversations with the traded indicate the opposite emotions for next week. ~Marty Moses

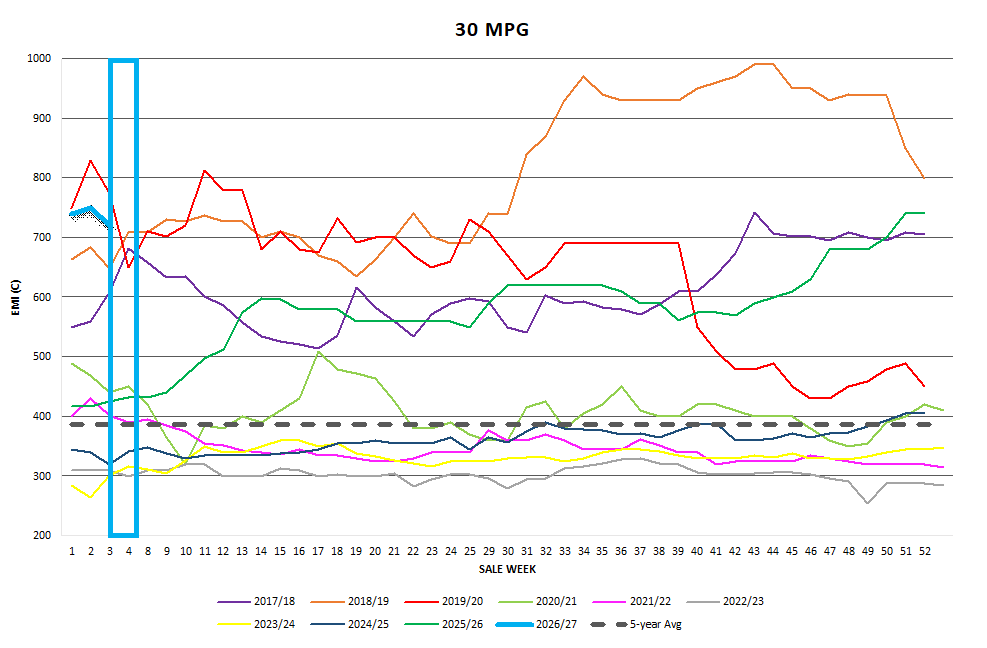

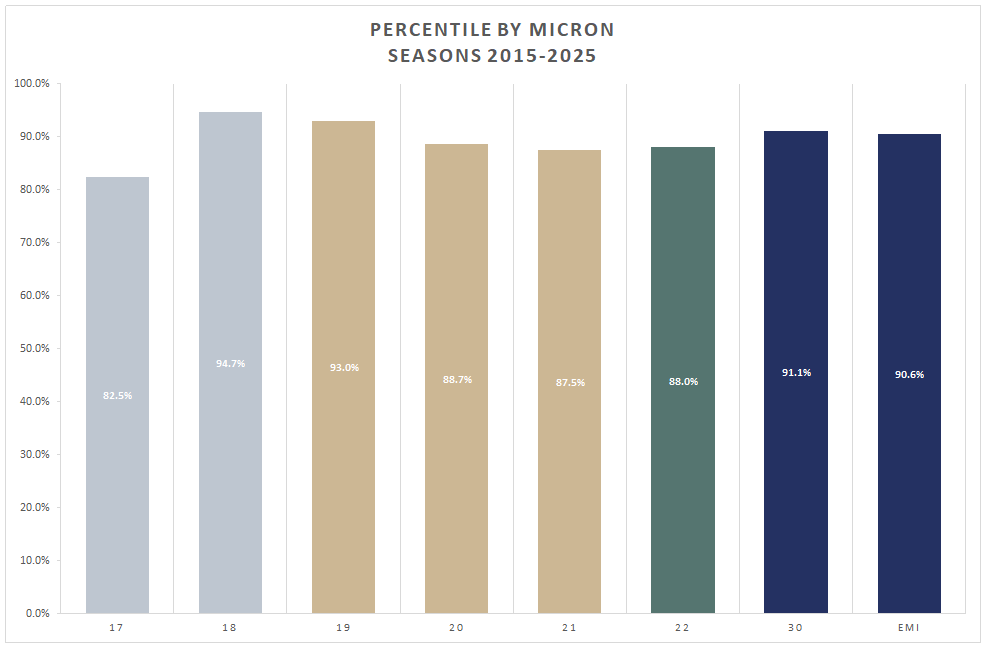

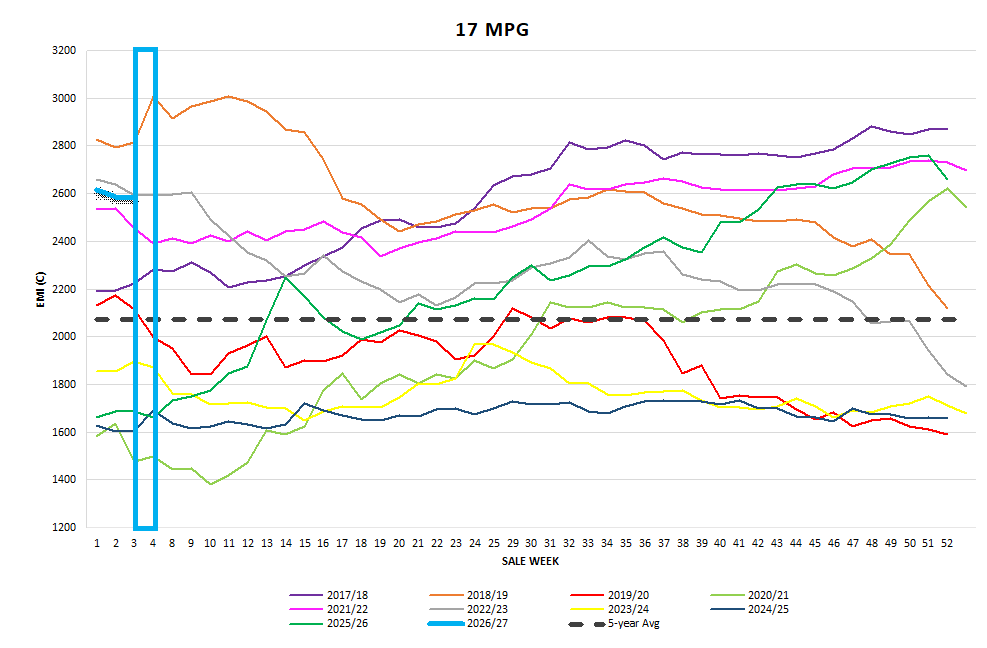

Graphs

Market Commentary

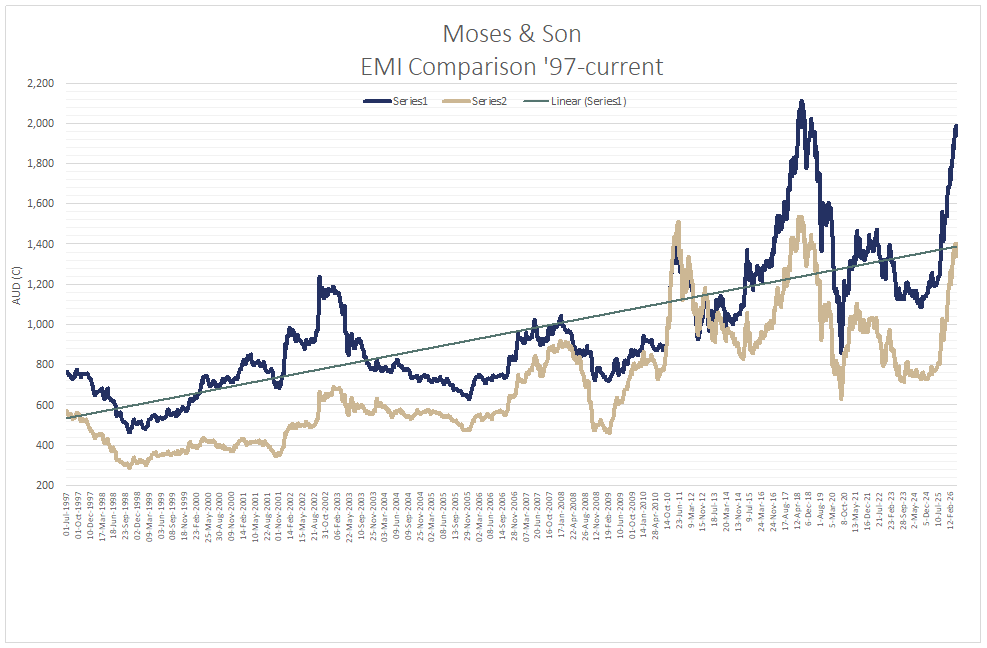

It seems the wool markets incredible recovery has hit its limit, temporarily. The traditional seasonal price pattern from June through spring, more than often delivers negative results for price. This trend that started as a supply driven recovery has more recently evolved into a demand-driven market. It has become more evident that the sharp price rally since mid-2025, have been consumed as the supply price was averaged up. However, the past month we have seen participants across the upper end of the supply chain, including those at the greasy wool level, are now closely watching to see whether downstream processors and consumers can fully absorb these higher price levels.

If you watch the daily news feeds you will be across the geopolitical developments as they continue to undermine global economies. It would be beneficial if the we could experience a market environment that’s not battling these external challenges.